IRAN: Senator Graham Backs Diplomacy With Iran

Mar-25 16:43

Senator Lindsay Graham (R-SC) has issued a statement on X: https://x.com/LindseyGrahamSC/status/2036...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 26W BILL AUCTION: HIGH 3.525%(ALLOT 82.17%)

Feb-23 16:32

- US TSY 26W BILL AUCTION: HIGH 3.525%(ALLOT 82.17%)

- US TSY 26W BILL AUCTION: DEALERS TAKE 28.19% OF COMPETITIVES

- US TSY 26W BILL AUCTION: DIRECTS TAKE 10.13% OF COMPETITIVES

- US TSY 26W BILL AUCTION: INDIRECTS TAKE 61.68% OF COMPETITIVES

- US TSY 26W BILL AUCTION: BID/CVR 3.03

FED: US TSY 13W BILL AUCTION: HIGH 3.590%(ALLOT 60.91%)

Feb-23 16:32

- US TSY 13W BILL AUCTION: HIGH 3.590%(ALLOT 60.91%)

- US TSY 13W BILL AUCTION: DEALERS TAKE 25.29% OF COMPETITIVES

- US TSY 13W BILL AUCTION: DIRECTS TAKE 6.62% OF COMPETITIVES

- US TSY 13W BILL AUCTION: INDIRECTS TAKE 68.09% OF COMPETITIVES

- US TSY 13W BILL AUCTION: BID/CVR 3.30

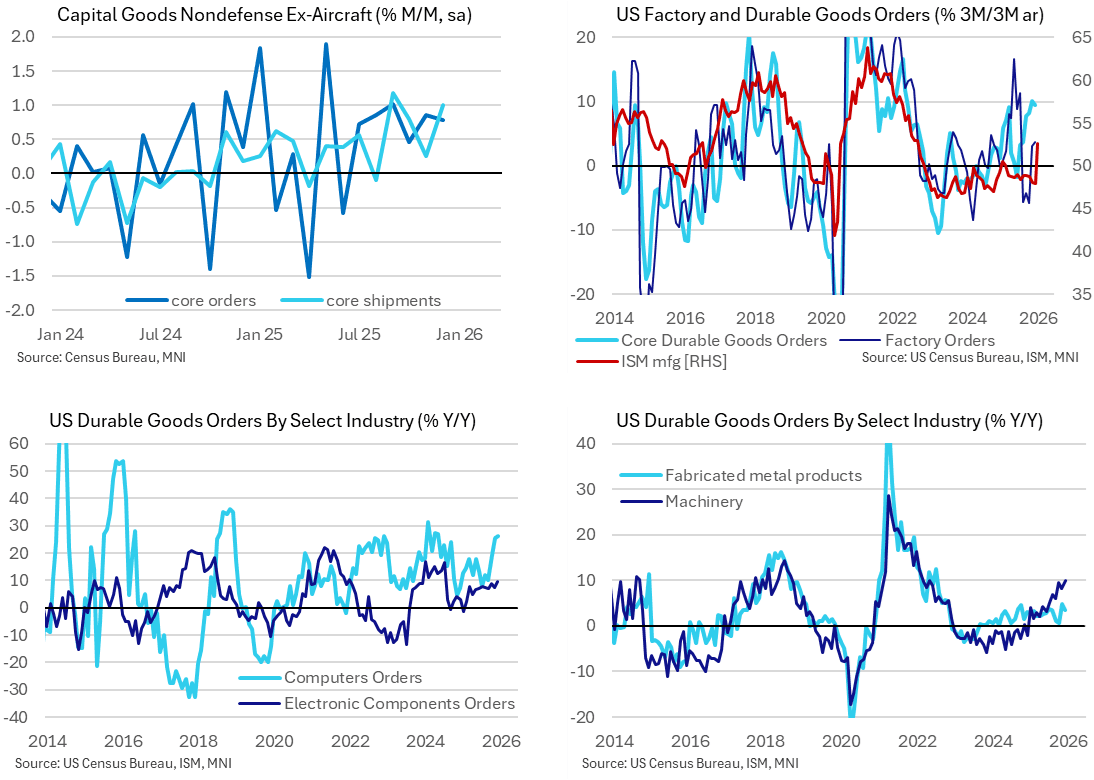

US DATA: Core Orders Revised Higher Less Than A Week After Preliminary Report

Feb-23 16:28

Factory orders were a touch softer than expected in December as they eased after a strong November, leaving a relatively tepid Q4 in implied real terms. Core durable goods painted a stronger picture however, especially after being revised higher from last week’s preliminary release of just four working days ago, in a release that helps support an upgrade in 4Q25 / 1Q26 business fixed investment estimates.

- Factory orders ($618bn) were close to expected in December as they slipped -0.7% M/M (sa, cons -0.6) after a strong 2.7% M/M increase in November.

- Finalized December figures for the smaller durable goods orders subset ($320bn) were unrevised at -1.4% M/M from preliminary estimates released just four working days ago.

- Core durable goods orders ($79bn) did however see a more impressive upward revision to 0.79% M/M (prelim 0.6 vs an original consensus of 0.3) considering the short turnaround time, after 0.86% M/M (initially 0.79) in Nov.

- Core durable goods shipments also saw upward revisions to 1.0% M/M (prelim 0.9) in Dec and 0.3% (initially 0.2) in Nov.

- Chiming with booming tech-focused capital goods imports, orders of computers continue to grow strongly (3.0% M/M, 26% Y/Y) as well as those for electronic components (1.6% M/M, 10% Y/Y). They are however still a relatively small share of broader orders at $1.7bn and $5.4bn.

- Factory orders saw a relatively tepid 3.7% annualized increase in Q4 considering it’s a nominal measure, for a similar trend pace to the 4.3% Y/Y. It follows some volatile quarters including -4.2% in Q3, 8.8% in Q2 and 8.1% in Q1.

- Core momentum looks strong though, with orders up 6.2% Y/Y in Dec and 9.4% annualized in Q4, whilst shipments have been catching up with 5.8% Y/Y in Dec and 8.5% annualized in Q4.