ARGENTINA: Second Review Of IMF Program Expected To Be Concluded By End of Month

Aug-05 12:01

- The inflation rate for July and August will be at the highest levels since President Alberto Fernandez took office in late 2019, according to an Economy Ministry official, as prices spiked significantly further amid political turmoil. (BBG)

- Officials also expect to conclude the second review of the government’s $44 billion program with the International Monetary Fund before the end of the month.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

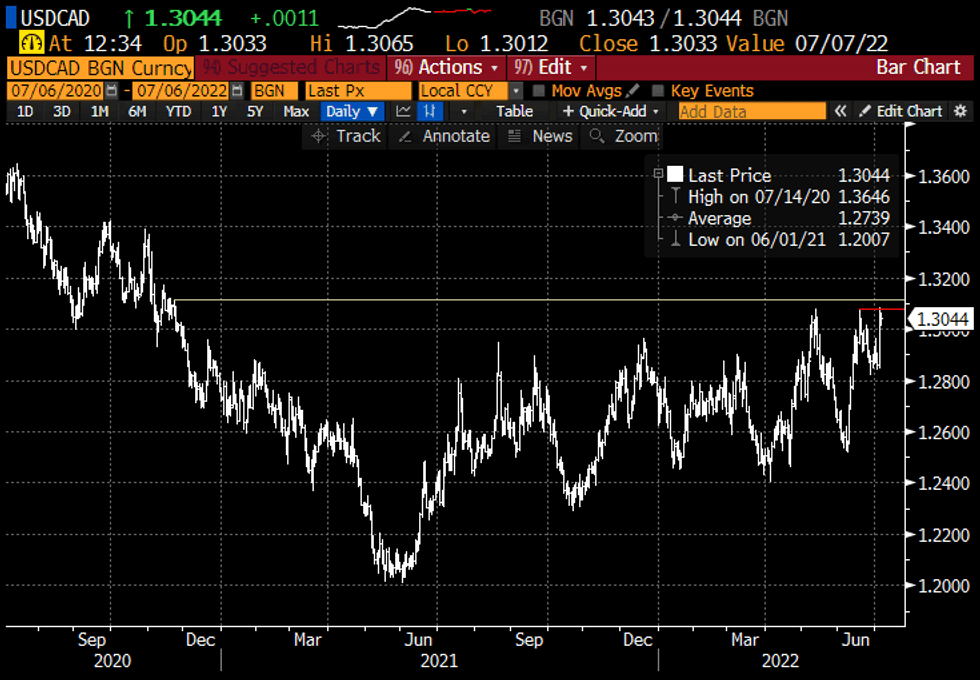

CANADA: USDCAD Plateaus After Testing Resistance

Jul-06 11:36

- USDCAD has only nudged higher today, +0.1% at 1.3044 after surging 1.3% higher yesterday on USD strength.

- It fleetingly cleared a bull trigger at 1.3079 (May 17 high) yesterday, a clear break of which would strength bullish conditions and open 1.3113 (Nov 23, 2020 high).

- USD strength has outweighed supportive Can-US yield differentials, potentially trimming the build in net longs seen in latest CFTC data as of Jun 28.

- The solid US docket sees plenty of potential drivers ahead, headlined by ISM services and the FOMC minutes but also with Fedspeak, JOLTS and the final PMI, with growth implications/interpretations very much in focus.

Source: Bloomberg

Source: Bloomberg

US EURODLR FUTURES: Post-LIBOR Settle Update: New 3Y High

Jul-06 11:35

Lead quarterly EDU2 trading weaker at 96.805 (-0.010) after latest 3M LIBOR set' +0.04228 to new 3Y high of 2.39057% (+0.09771/wk).

- Balance of Whites through Reds (EDZ2-EDM4) -0.030-0.005, as forward rate hike expectations holding steady around 75bp in July followed by two consecutive 50bp hikes; Greens through Golds (EDU4-EDM7) steady to +0.010.

- Recession expectations priced in front end: Dec'22/Mar'23 inverted at -0.125. Most inverted calendar spd: EDH3/EDH4 extends to -0.745.

- Light overnight option volume, buyers of short Dec 100.5 calls at 1.0 -- looking for futures to price in rate cuts back to 0.0 by end of 2023.

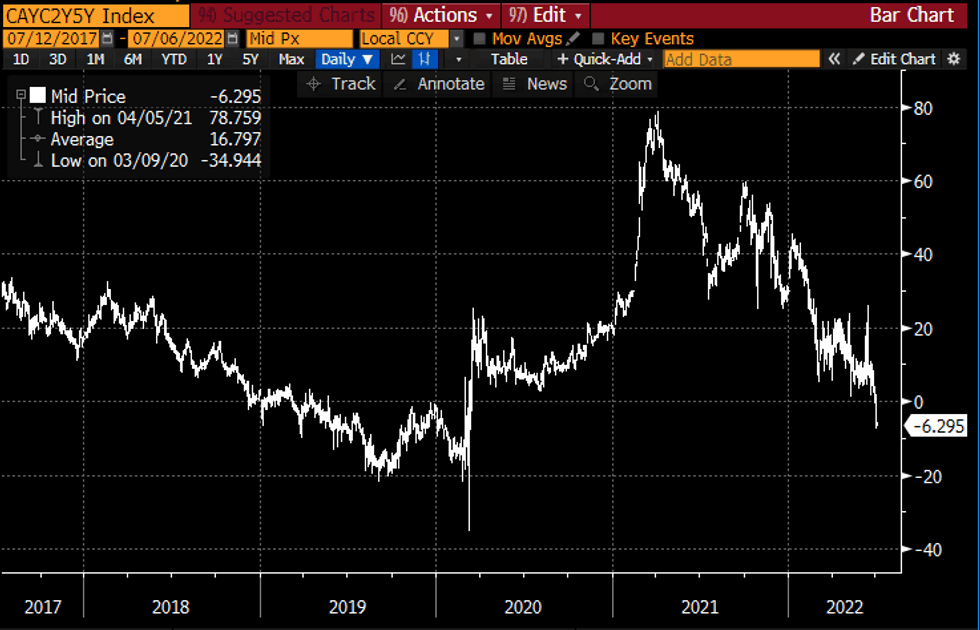

CANADA: GoCs Stabilise After Yesterday's Rally

Jul-06 11:30

- GoCs sell-off slightly after with the open, with yields rising ~1bp across the curve after rallying 9bps in 5Y and 10Y tenors yesterday. It leaves the 2s5s inversion of -5.5ps close to yesterday’s low, having become inverted for the first time since Mar’20 on Monday.

- Can-US yield differentials have dipped from yesterday’s highs but remain at the high end of recent ranges with +18bp for the 2Y and +27bp for the 10Y.

- The tentative start to the day is echoed in early BAX trading, with yields crawling across the curve after sliding yesterday to drive further inversion through 2023 with 45bps of cuts priced through Dec'22-Dec'23.

GoC 2s5s spread (shown as mid price and not ask price in text)Source: Bloomberg

GoC 2s5s spread (shown as mid price and not ask price in text)Source: Bloomberg