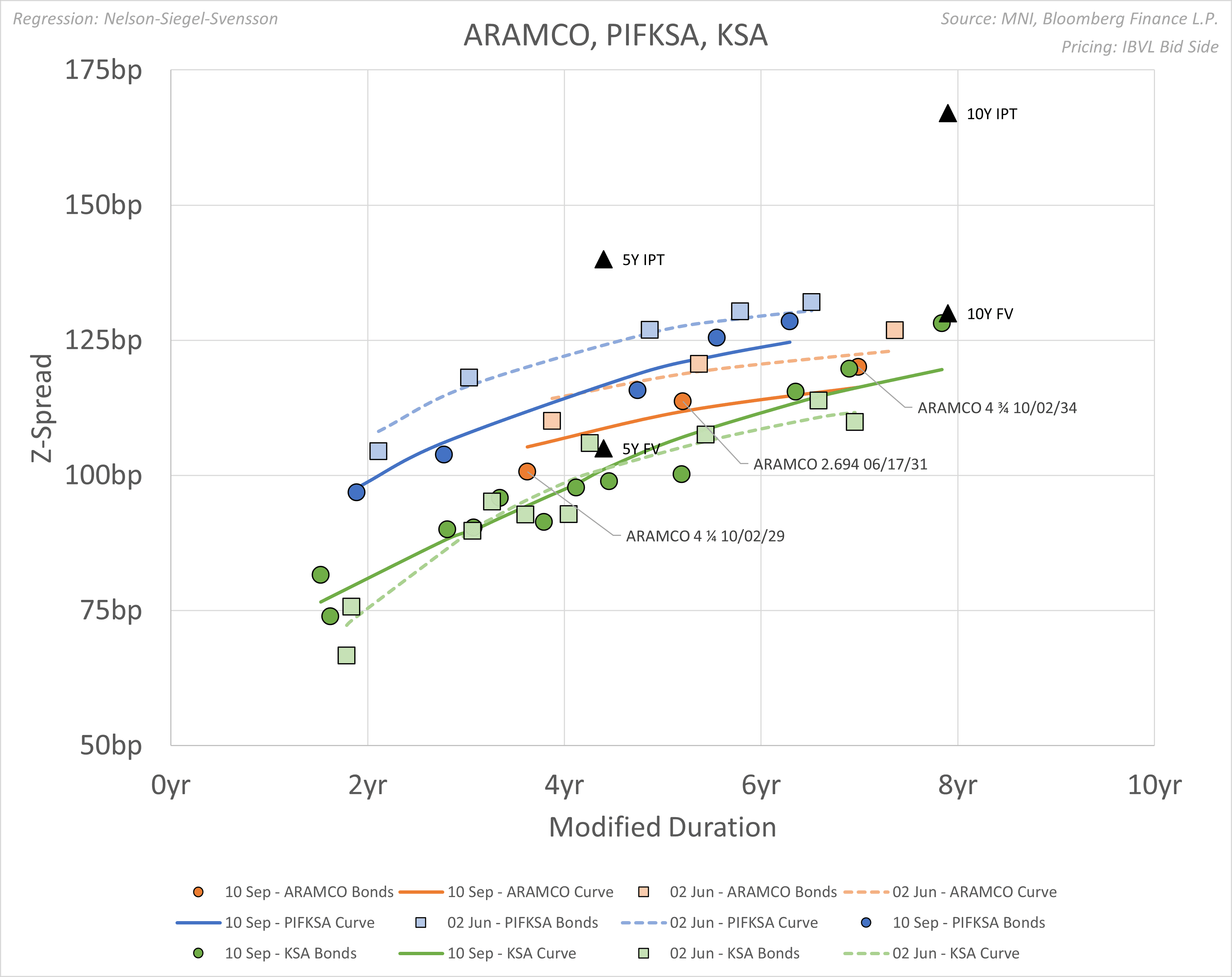

EM CEEMEA CREDIT: Saudi Aramco: FV for $ BM 5Y & 10Y Sukuk

(ARAMCO; Aa3/NR/A+)

IPT 5Y @ T+105bp area FV @ T+70bp

IPT 10Y @ T+115bp area FV @ T+78bp

- 5Y deal: we see z+105bp or T+70bp, that is some 10bp pick up vs the seasoned 29s.

- 10Y deal: we see z+130bp or T+78bp, that is some 10bp pick up vs the seasoned 34s.

- We sketch our FV considerations focusing on Aramco’s granular secondary curve in Sukuk format. For context, we also look at PIF and KSA curves in Sukuk format.

To gain perspective, we look at spread moves since Aramco’s last (conventional format) issuance back on Jun 2. We note Sukuk format curves have tightened some 8bp for Aramco and 5bp for PIF, whilst KSA has steepened pivoting around 4Y tenor (see chart below).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

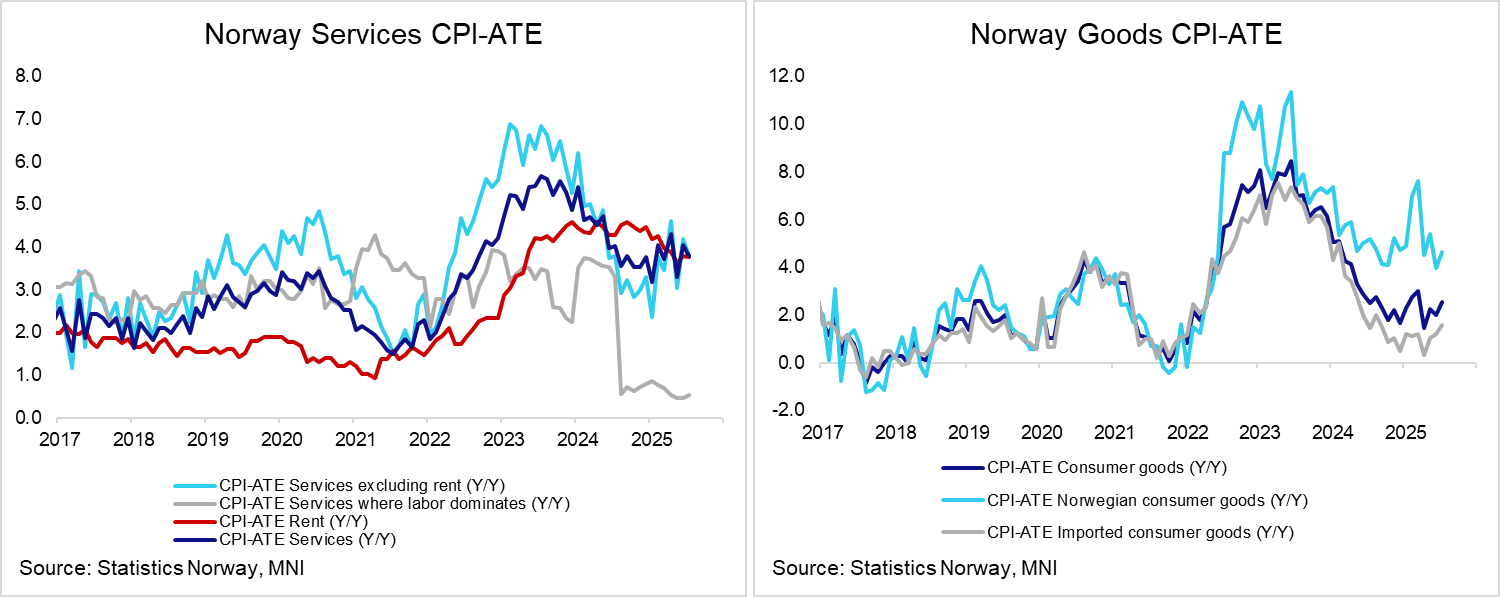

NORWAY: July CPI - Uptick In Food Alongside Persistent Underlying Services

- Food prices rose 4.53% M/M and 5.57% Y/Y (vs 4.35% prior) – above some of the estimates we had seen, and likely the main driver behind the higher-than-expected CPI-ATE reading (at least versus analyst projections).

- Rents remain a source of persistent inflationary pressure, rising 0.32% M/M for the second consecutive month with an annual rate of 3.77% Y/Y (vs 3.78% prior).

- Services excluding rents eased to 3.80% Y/Y (vs 4.19% prior).

- A pullback in airfares (-0.18% Y/Y vs 7.36% prior) and package holiday (1.24% Y/Y (vs 6.94% prior), which drove a large part of the upward inflation surprise in June, were offset by rises in accommodation (6.83% Y/Y (vs 3.66% prior) .

- Otherwise, there were some signs of persistence in the likes of insurance (14.31% Y/Y vs 13.24% prior), personal care (3.66% Y/Y vs 2.92% prior), restaurant services (3.35% Y/Y vs 3.37% prior) and recreation and culture (3.93% Y/Y vs 3.87% prior). Services inflation where labour dominates and excluding regulated prices ricked up to 4.26% Y/Y (vs 4.20% prior).

- Domestic goods inflation excluding agricultural products rose to 4.56% Y/Y (vs 4.18% prior). Alongside food, there were accelerations in a broad range of goods components (clothing, footwear, furniture, household textiles). Imported inflation ex agriculture was steady at 0.80% Y/Y. Including agricultural products, imported inflation is back on a gradually rising trend.

- Electricity prices fell 2.19% M/M, but this still saw the annual rate rise to 11.31% Y/Y (vs 8.34% prior), seemingly driving the headline inflation increase to 3.27% Y/Y (vs 2.99% prior).

RBA: MNI RBA Preview-Aug 2025: Cautious Augut Rate Cut

- Download Full Report Here

- The RBA’s Monetary Policy Board is unlikely to surprise economists and the market again in August when its decision is announced on Tuesday August 12. Bloomberg consensus is unanimous forecasting a 25bp rate cut to 3.60% given the further moderation in underlying inflation in Q2 towards the band mid-point, which should increase confidence that it is now sustainably within target, and signs that the labour market has reached a turning point.

- Thus, the “timing” this month is likely to be more suitable than last month possibly resulting in a 9-0 vote after July’s 6-3 split in favour of holding.

- With the economy broadly developing as the Board expected in May, there are unlikely to be material changes to the updated forecasts accompanying the August statement.

- The tone of the decision and Governor Bullock's press conference is likely to reiterate the bank's gradual and cautious approach to easing. We expect any further cuts to coincide with forecasting meetings.

SCHATZ TECHS: (U5) Support Remains Intact For Now

- RES 4: 107.430 High Jun 13

- RES 3: 107.360 High Jul 22 and a key resistance

- RES 2: 107.222 50-day EMA

- RES 1: 107.157 20-day EMA

- PRICE: 107.055 @ 07:15 BST Aug 11

- SUP 1: 107.010 Low Jul 25 and a bear trigger

- SUP 2: 107.993 1.500 proj of the Jul 7 - 11 - 22 price swing

- SUP 3: 106.964 1.618 proj of the Jul 7 - 11 - 22 price swing

- SUP 4: 106.928 1.764 proj of the Jul 7 - 11 - 22 price swing

The sell-off in Schatz futures between Jul 23 - 25, resulted in a break of key short-term support at 107.120, the Jul 11 low and a bear trigger. However, the contract has recovered from the Jul 25 low and recent price patterns highlight a potential base. A resumption of gains would expose resistance at the 20-day EMA, at 107.157. The 50-day EMA is at 107.222. On the downside, key support and the bear trigger has been defined at 107.010, the Jul 25 low.