US STOCKS: S&P - New Highs Again, OpEx Tonight Could See Demand Slow

The S&P(ESM6) range overnight was 7475.25 - 7540.00, SPX closed +0.77%, Asia is currently trading ar...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

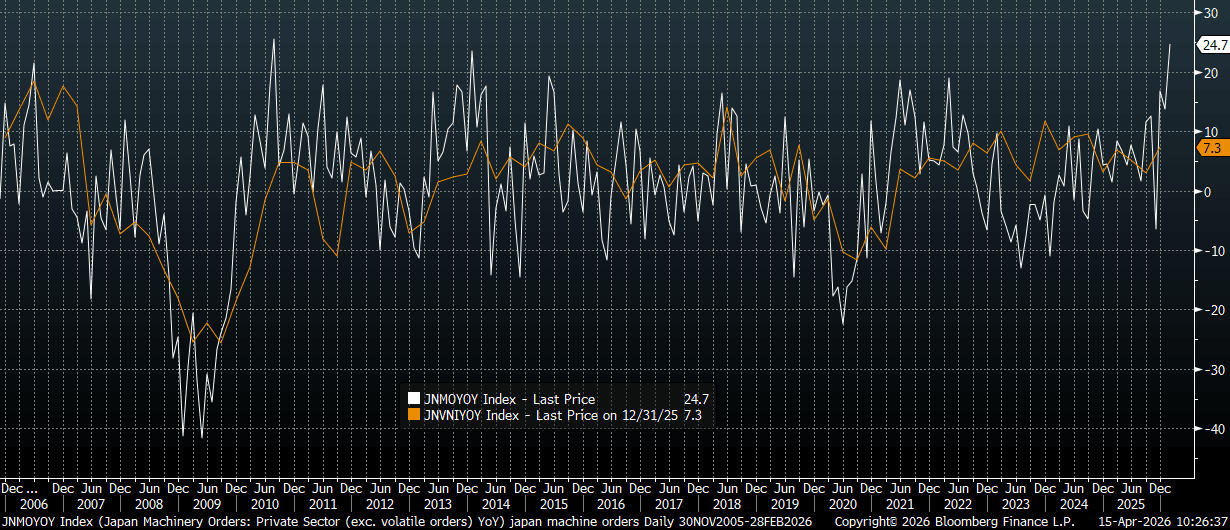

JAPAN DATA: Machine Orders/Capex Were Robust Prior To Iran Conflict

Japan Feb core machine orders were well above market forecasts. We rose 13.6%m/m, versus -1.1%m/m forecast and -5.5% prior. The m/m outcomes have been volatile, but mostly with a firmer bias in recent months. The y/y print surged to 24.7%y/y, versus 8.1% forecast and 13.7% prior. Below the core machine order print, in y/y terms (the white line) is plotted against Japan Capex, y/y (ex software). All else equal, the strength in machine orders, is pointing to a positive Q1 Capex backdrop. The Iran conflict, which kicked off in March, is an obvious cloud over the outlook, but clearly heading into it machine orders/capex were quite firm. Note next week, on Apr 23, we get preliminary PMIs for April, which may provide an update on the conflict's impact.

- Reuters noted earlier: "Japanese manufacturers' confidence posted its biggest month-on-month drop in more than three years in April, dampened by surging oil prices and supply-chain disruptions caused by the Middle East conflict, the Reuters Tankan poll showed."

- The uncertainty created by the conflict (even with the risks associated with higher inflation) is a factor cited as lowering BoJ hike odds for April. From above 70% at the start of April, we are now back to around 36% in terms of a full hike being priced, per OIS markets.

Fig 1: Japan Core Machine Orders (White Line) & Capex Ex Software (Orange Line) Y/Y

Source: Bloomberg Finance L.P./MNI

JGBS: Futures Lag Global Moves As BoJ Considering Higher Inflation Forecasts

JGB futures are softer to start Wednesday trade, lagging broader global/region trends. We were last 130, +.01 versus settlement levels. We are just short of recent highs, but still comfortably under the 20-day EMA (130.46) and 50-day EMA (131.26) resistance points. From late yesterday, via BBG, is likely aiding the lag in JGB futures: "Bank of Japan officials are likely to consider raising their inflation forecast sharply at their policy meeting this month, mainly to reflect elevated oil prices, according to people familiar with the matter."

- Broader bond futures sentiment remains positive, with UST 10yr at 111-20, close to recent highs. Optimism around an further US-Iran talks and Trump stating earlier (via FoxNews) that he sees the war close to an end, is weighing on oil prices and keeping broader risk sentiment supported.

- In the cash JGB space, we have softness in the back end with 20-40yr tenors down around 2bps in yield. We have steadier trends elsewhere, with the 10yr near 2.425%.

- On the data front, we had the Feb core machine orders print a short while ago, up 13.6%m/m, well above market markets of a -1.1% m/m decline. In y/y terms we were +24.7%, against a 8.1% forecast.

- Also note for today, via BBG: "The BOJ will buy notes due in one to 10 years and bonds maturing in more than 25 years".

LNG: Gas Follows Oil Lower On Hopes Of Iran War Resolution

The direction of gas prices continued to be determined by news from the Middle East. They followed oil lower following headlines that US-Iran talks could resume towards the end of the week which could extend the ceasefire which appears to be holding. President Trump also said in a recent FOX interview that “the war is very close to being over”.

- European gas fell 8.2% to EUR42.62 on Tuesday after reaching a high of EUR 45.845 and is now down 16% in April and 42% since the 19 March peak at EUR 73.79.

- European storage reached a seasonal low on 31 March at 27.66% and is currently slightly higher at 29.55%. The impact of the Iran conflict on the region’s ability to rebuild inventories is being watched closely. Higher temperatures and wind-generated power are helping for now.

- Lower Asian LNG imports should reduce competition for supply helping Europe refill. Bloomberg reported that imports fell to their lowest in close to 6 years in the 30-days to 12 April due to tankers unable to pass through the Strait of Hormuz. China’s average fell 30% y/y and India’s 20% y/y. Bloomberg also notes that Japan is reducing gas-fired power output and Korea has lifted its coal cap.

- US Henry Hub fell 1.3% to $2.594 to be over 10% lower this month but is currently down to $2.586. It reached $2.66 before declining to $2.561. Even without geopolitical swings, US gas would face pressure given ample supply and inventories above the 5-year average during the shoulder season.

- While BNEF data showed estimated flows to LNG export facilities rising 3.4% w/w on Tuesday, US LNG exports fell to their lowest in almost 2 months in the week to 12 April despite Qatar’s exports coming to a halt.