DIESEL: Russian Diesel Exports Fell 4% in Oct. Amid Refinery Outages

Nov-06 13:24

Russian diesel and gasoil exports fell by 4% on the month to 2.37m tons in October, according to LSEG amid seasonal and unplanned refinery outages.

- Turkey remained the main importer with total diesel and gasoil exports rising 1% from September to 1.0m tons but shipments to Brazil fell 73% to 74k tons.

- Brazil has boosted diesel imports from the US, India, and the UAE to replace the drop in Russia supplies.

- Morocco, Tunisia, Senegal and Libya were also among the biggest importers of Russia diesel and gasoil in October.

- Recent US sanctions are having an impact with increased ship-to-ship transfers near Limassol port, the Laconian Gulf and Port Said anchorage, Reuters sources said.

- Russian ultra-low-sulphur diesel exports from the Baltic Sea port of Primorsk fell 5.7% on the month 0.06m tons.

- Russia's crude processing rates rose to 5.15m b/d over Oct. 23-29, as some refineries ramped up operations after seasonal maintenance and drone-related disruptions, Bloomberg said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

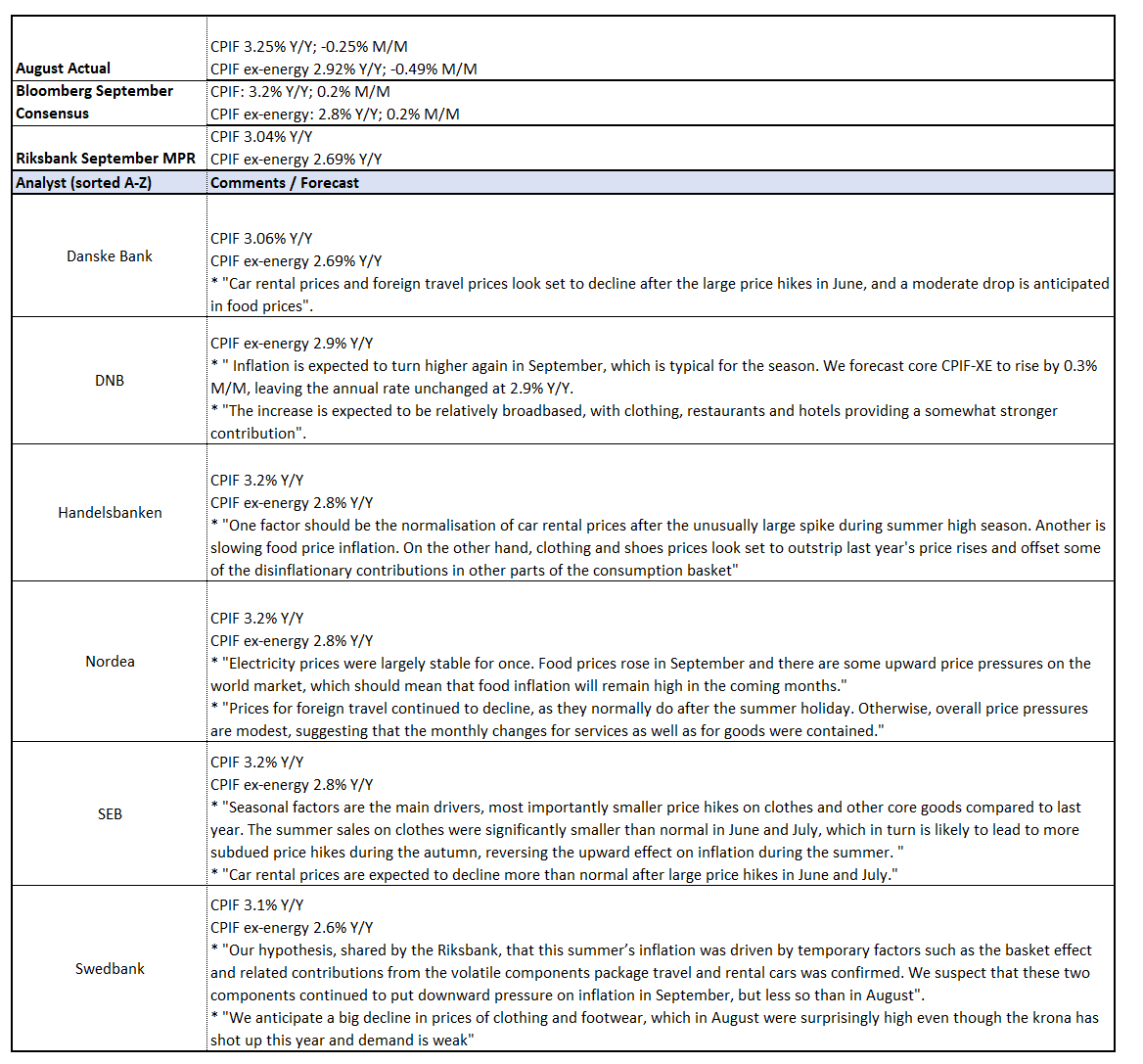

SWEDEN: September Flash Inflation Due At 0700BST/0800CET; No Fireworks Expected

Oct-07 13:14

Swedish flash September inflation is due tomorrow at 0700BST/0800CET, but is not expected to be a major market mover. The Riksbank has signalled that it is likely to remain on hold going forward, after delivering a 25bp cut to 1.75% in September. The Board will require a much larger stock of data than one inflation report to consider deviating from this stance.

- Analysts expect CPIF ex-energy inflation to ease to 2.8% Y/Y (vs 2.9% in August). The Riksbank’s September MPR projects a larger deceleration to 2.7% Y/Y.

- A continued pullback in volatile components such as car rentals and package holidays are expected to contribute to disinflation in September. These components drove the inflation uptick over the summer, but the Riksbank assesses these dynamics to have been temporary.

- There is some uncertainty amongst analysts around the contribution from the clothing and footwear component in September (see image for more).

- CPIF ex-energy is expected to fall significantly below target next year due to the Government’s temporary food VAT tax cut. The Riksbank will look through associated swings in annual inflation rates. Indicators of price pressures (e.g. Economic Tendency Indicator expected prices) point to subdued underlying inflationary pressures ahead.

- As always, the flash release does not contain any details. The final report is due on October 15.

EU-BOND SYNDICATION: 2.75% Dec-32 / New 15-year 3.625% Dec-40 EU-bond: Priced

Oct-07 13:03

2.75% Dec-32 EU-bond

- Reoffer 99.114 to yield 2.889%

- Spread set at MS + 34bps (guidance was MS + 36bps area)

- Size: E5bln - in line with initial guidance (MNI expected E4-5bln)

- Final books in excess of E96bln (inc E7bln JLM interest)

- HR 105% vs 1.70% Aug-32 Bund 42.2bps. Spot ref: 95.220 / 2.467%

New 15-year 3.625% Dec-40

- Reoffer 99.518 to yield 3.666%

- Spread set at MS + 75bps (guidance wasMS + 77bps area

- Size: E6bln - up from initial E5bln guidance (MNI expects E5-6bln)

- Final books in excess of E79bln (inc E6.75bln JLM interest)

- HR 98% vs 2.60% May-41 Bund 55.2bps. Spot ref: 93.720 / 3.114%

- ISIN: EU000A4EJF17

- Coupon: 3.625%. Long first

- Maturity: 12 December 2040

For both:

- JLMs: BNP Paribas (B&D/DM), Citi, Deutsche Bank, DZ BANK and Santander

- Settlement: 14 October 2025 (T+5)

- Timing: TOE 13.46 BST / 14:46 CET. FTT Immediately

From market source / MNI colour

MNI: US REDBOOK: OCT STORE SALES +6.1% V YR AGO MO

Oct-07 12:55

- MNI: US REDBOOK: OCT STORE SALES +6.1% V YR AGO MO

- US REDBOOK: STORE SALES +5.8% WK ENDED OCT 04 V YR AGO WK