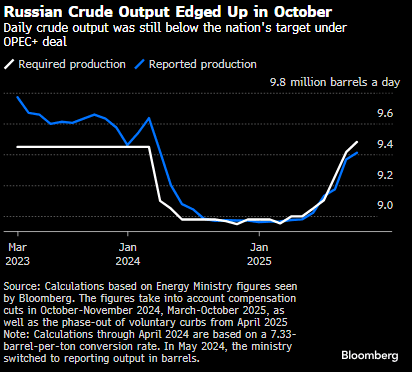

OIL: Russian Crude Output Rose in Oct: Bloomberg

Nov-07 13:54

Russia’s crude oil production edged up in October, but remained below its OPEC+ quotas as international pressure mounted on the country’s energy sector, Bloomberg said.

- Russia pumped an average of 9/411m b/d last month, sources told Bloomberg.

- That is 43k b/d higher than in September and 70k b/d below a quota that includes compensation cuts for previous overproduction.

- Meanwhile. Ukrainian attacks have intensified, putting pressure on Russia’s crude-processing sector even as refinery owners rush to repair infrastructure.

- If Moscow eventually finds itself unable to find buyers for oil from its sanctioned producers, and struggles to restore refining, it’ll be forced to halt output at some fields, risking damage to wells, Bloomberg.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: BLOCK/Pit: Large Feb'26 SOFR Call Spread Buy

Oct-08 13:47

- +50,000 SFRG6 97.25/97.50 call spds, 1.0 ref 96.52 at 0939-0942ET

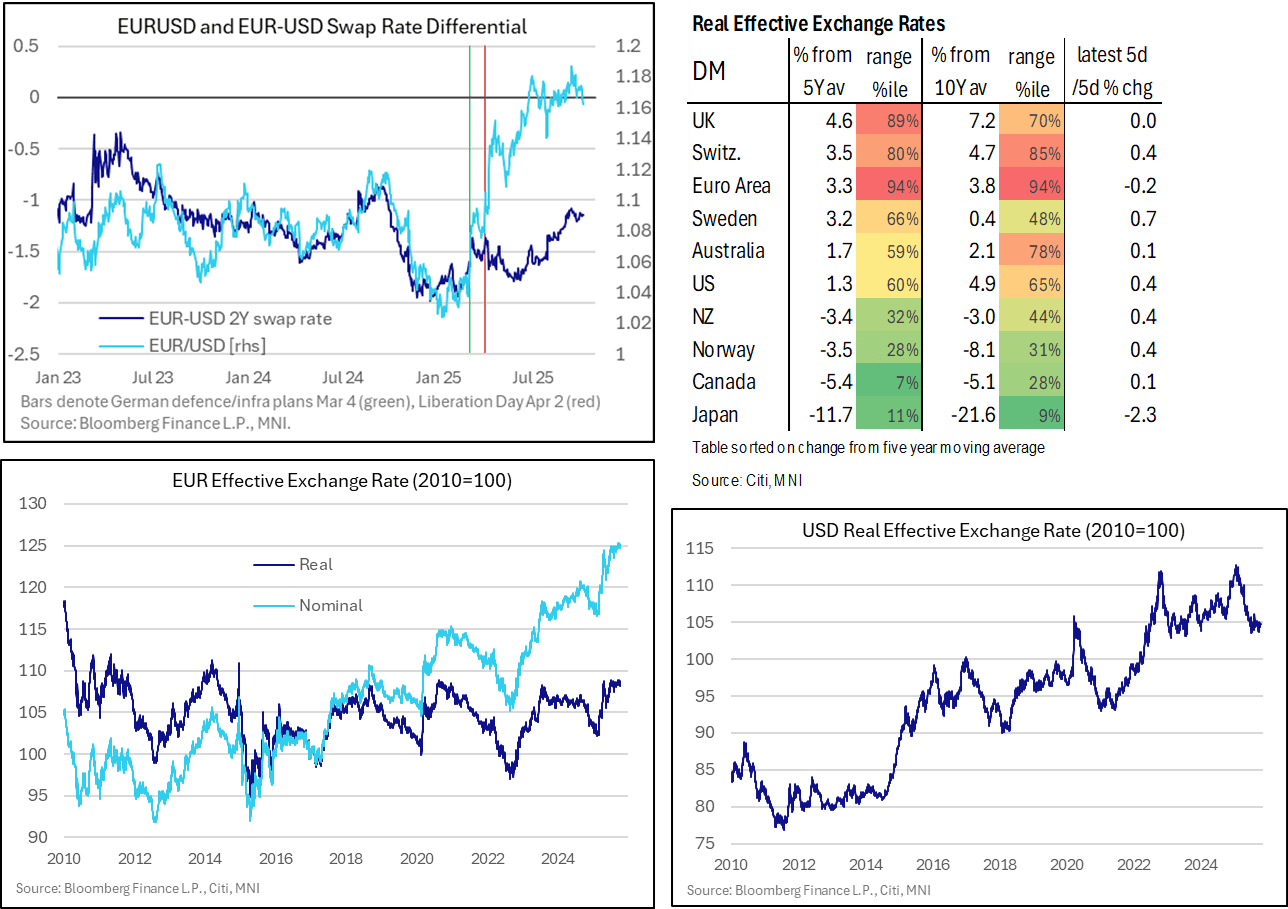

EUR: Euro Effective Exchange Rate Still Historically Stretched

Oct-08 13:47

- EURUSD has held onto a dip below 1.1650 today, earlier touching a low of 1.1606 in what was its lowest since early September.

- In doing so, it has pulled back from mid-September’s short-lived fresh cycle high of 1.1919 having pushed through the previous high of 1.1829 on Jul 1. The latter came with ECB VP De Guindos explicitly saying a 1.20 level is “acceptable” but something above that “would be more complicated”. It was part of remarks that were more typical for central bank speech, with the speed of the euro’s climb more worrying than the level.

- Since then, at an MNI event on Sep 18, De Guindos pushed back on focusing on EURUSD and talked to the nominal effective exchange rate as part of a comprehensive approach.

- “The media gives a lot of attention to the exchange rate of the euro vis-a-vis the dollar, but I think that we have to give much more attention to what we call the nominal effective exchange rate. And here with China, I think that sometimes we overlook a little bit what's happening there, and this is another element of uncertainty that we will have to carry”. The NEER is “something that we have to look at carefully, because it’s going to be relevant for growth and for inflation”.

- To this end, the euro NEER according to Citi has eased 0.7% from highs seen on Sep 18 but clearly remains close to those multi-year highs – see charts.

- We prefer looking in real terms when it comes to a cross-country comparison, and here the euro sits at the 94th percentile over both five- and ten-year windows. This is the most stretched across developed markets although both sterling and the Swiss franc see higher relative deviations from historical averages.

- These ranges in isolation suggest asymmetrical risk ahead with skew towards a weaker euro.

- That’s coupled with some ECB Governing Council members not appearing overly concerned by disinflationary implications from the currently elevated exchange rate. One example was a typically centrist Bank of Spain’s Escriva earlier today saying he wouldn’t overemphasize a strong euro as a risk factor for the inflation outlook, whilst Bundesbank's Nagel wasn't concerned about the euro's valuation on Sep 22.

EURIBOR OPTIONS: More Large Upside Options

Oct-08 13:37

ERH6 98.25/98.37cs, bought for 1 in 20k.