EU: RTRS-Commission Plans To Cut Foreign Steel Quota In Half, Tariffs Of 50%

(MNI) London - Reuters reports that according to its sources, the European Commission has plans to "cut foreign steel quotas by nearly half" as part of a new safeguards package. This package would also see a hike in import tariffs on foreign steel "to similar levels as the US and Canada", with the report claiming this could be as high as 50%.

- Germany's Handelsblatt reported on 26 Sep that the Commission was considering tariffs of 25-50% on foreign steel and steel products in order to protect its markets from dumping of cheap steel in the wake of the US' 'reciprocal' tariffs, with the Reuters report seemingly confirming the upper end of this envelope will come into play.

- European Industry Commissioner Stephane Sejourne told Handelsblatt, "Europe has no choice but to find a new balance, [this requires] fewer internal trade barriers, with a truly functioning internal market [but also] protective measures to restore balance with partners who no longer respect any rules."

- This comes in the wake of a major increase in Chinese steel exports, (up 4-9% according to analyst estimates). Relations between Brussels and Beijing are already in a precarious position following a summit that achieved little in July, amid tensions over the war in Ukraine and European concerns of dumping.

- Protection of the EU steel sector is viewed as crucial in Brussels for decarbonisation and efforts to ensure European defence capabilities, while in member state capitals, concerns extend to supporting domestic industry and avoiding political blowback from powerful trade unions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

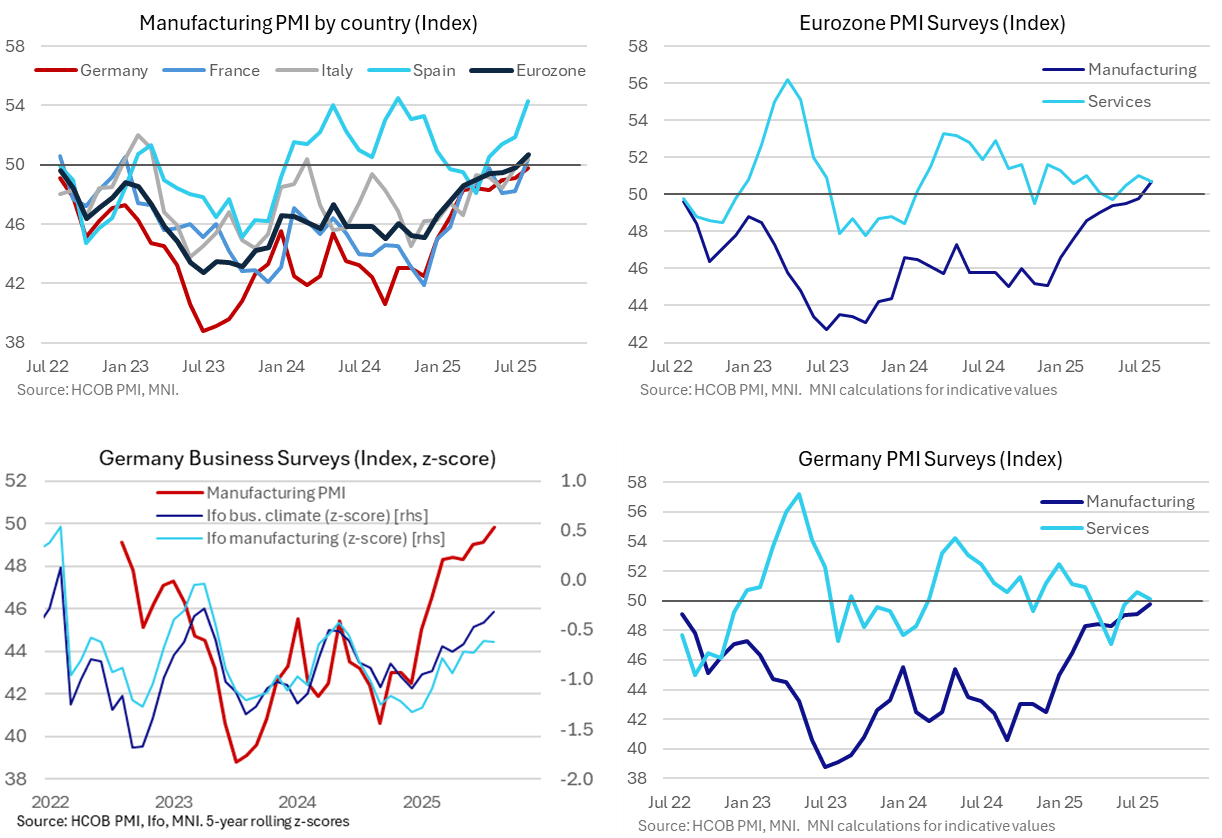

EUROZONE DATA: German Mfg PMI Lags Further Despite August Improvement

The Eurozone final August manufacturing PMI release was revised higher to further confirm a 38-month high. Despite a string of improvements it is still only just above the 50 breakeven line, although has closed a sizeable gap to services (ahead of Wednesday's revisions for the latter). Latest manufacturing improvements were seen across the board although Germany continues to lag France and Italy modestly, whilst Spain is an even clearer outperformer.

- The Eurozone manufacturing PMI was revised up to 50.7 in the final August release (prelim 50.5) to extend the increase to what was its first above-50 (i.e. expansionary) reading in the three-year lookback for publicly available data and a 38-month high per the press release.

- Within that, factory output was revised up from 52.3 to 52.5, a solid improvement from the 50.6 in July for still a 41-month high.

- The press release also confirmed that “eurozone manufacturers saw operating expenses increase for the first time in five months, although the uptick was only marginal.” However, prices “charged were discounted fractionally.”

- Germany was revised down a tenth to 49.8 (prelim 49.9) to trim an increase from 49.1 in July, with the EZ upward revision itself helped by a larger than first thought bounce in France to 50.4 (prelim 49.9) from 48.2.

- Our rough calculations also point to stronger than first implied manufacturing readings elsewhere, with our Eurozone ex Germany & France estimate revised up to 51.6 (prelim 51.2) after 51.0 in July.

- As we noted earlier, today’s first details for Spain were particularly robust at 54.3 (cons 52.1) after 51.9 for just shy of cycle highs of 54.5 in Oct 2024. Italy meanwhile increased to 50.4 after 49.8.

USD: Broader selling going through

- Another round of Dollar selling here, EUR is heading towards the initial resistance of 1.1743 High Aug 22.

- The AUD, GBP, CAD, SEK, PLN, MXN, INR, CZK, NOK, NZD are all lifted.

- AUDUSD now targets the next immediate resistance at 0.6569, 14th Aug high.

STIR: Danske Recommend Paying June '26 Vs. Dec '25 & Dec '26 ECB On Fly

Danske Bank recommend tactically paying the June ‘26 ECB meeting vs. receiving the Dec ‘25 and Dec ‘26 meetings on an ECB-dated OIS fly structure.

- They note that their “baseline is for the pricing of additional rate cuts from the ECB to move closer to zero as the economy has proven surprisingly resilient and downside risks to the outlook have faded. However, the prospects of inflation moving below 2% and wage indicators remaining soft also dampen the likelihood of the ECB kicking off rate hikes in late ‘26”.