CEE: Romanian Liberals Refuse To Support President's PM Candidate

Romania's third-largest National Liberal Party (PNL) said it would not support MEP Eugen Tomac's bid...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Gilt/Bund Spread Above 200bp, Targeting October High

The 10-Year gilt/Bund spread is ~5bp wider on the day at ~201bp, with the move driven by an increase in UK political risk premia, as questions surrounding the future of UK PM Starmer intensify.

- The spread hasn’t closed above 200bp since October.

- Next upside target of note located at the October closing high (204.23bp).

Fig. 1: 10-Year Gilt/Bund Spread (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

FOREX: FX OPTION EXPIRY - Large in the Yen next Monday

Large expiry in USDJPY next Monday. 2.61bn are Calls, 1.85bn are Puts.

Of note:

EURUSD 3.02bn at 1.1745/1.1750 (could act as magnet).

USDJPY 1.58bn at 157.00 (wed).

USDCNY 1.24bn at 6.7930 (thu).

USDJPY 4.46bn at 159.00 (mon).

- EURUSD: 1.1700 (1.37bn), 1.1705 (231mln), 1.1715 (266mln), 1.1745 (1.13bn), 1.1750 (1.89bn), 1.1785 (1.5bn), 1.1800 (1.3bn).

- NZDUSD: 0.5950 (240mln).

- AUDNZD: 1.2168 (247mln).

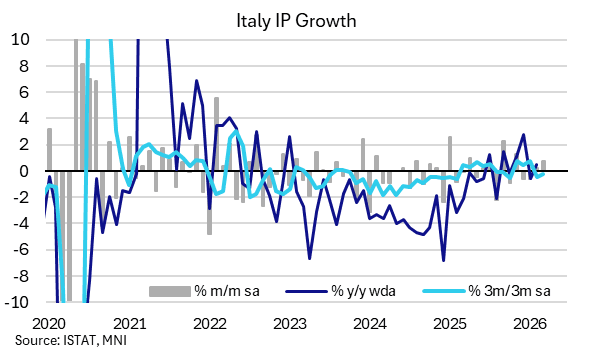

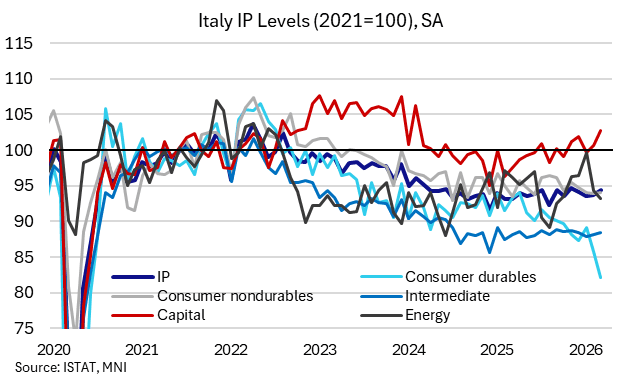

ITALY DATA: IP Rises on Capital Goods, Ending A Tepid Quarter On Better Footing

Italian industrial production saw a second monthly increase in March and encouragingly was led by capital and intermediate goods whilst energy production saw a second consecutive fall. Prior weakness still saw soft production in Q1 as a whole albeit with improved momentum heading into Q2.

- Industrial production saw a solid 0.7% M/M increase in March (0.2% cons) after 0.2% in February (revised up 0.1ppt).

- On monthly drivers, capital goods production increased a strong 2.1% M/M (1.1% Feb), rising further after the large -2.3% M/M drop in January. Intermediate goods saw more modest growth at 0.3% M/M (0.3% prior).

- Offsetting these, consumer goods dropped -0.4% M/M (-0.5% prior), a fourth straight decline, led by durables which saw another sharp drop at -4.2% M/M (-3.7% prior), while consumer nondurables rose slightly 0.1% M/M (-0.1% prior).

- Energy production also fell again at -1.2% M/M, continuing to dampen IP after a sharp -5.4% prior (revised down a notable 0.6ppt).

- Recent momentum remains fairly weak though with 3M/3M IP still down -0.2% 3M/3M (-0.5% prior, which followed threemonths positive, but has not been higher than 0.7% since mid-2022). Consumer goods, particularly durables, dragged down the rate here although weakness was fairly broad-based with only capital goods and energy showing modestly positive 3M/3M growth.

- On an annual basis, IP grew 1.5% Y/Y (WDA), up from 0.4% prior (revised down 0.1ppt). Here, the biggest drivers were transport equipment (11.2% Y/Y), mining and quarrying (6.7% Y/Y) and computers/electronics (6.1% Y/Y). Offsetting these were chemicals (-7.8% Y/Y), electricity/gas/steam/air conditioning (-4.0% Y/Y) and "other manufacturing" (-2.4% Y/Y).

- Eurozone-wide IP is due tomorrow (Wednesday), with consensus currently looking for 0.2% M/M (after 0.4% Feb).