US TSYS: Risk-Off Unwinds as Oil Retreats, BoE & ECB Hold Rates Steady

* Treasuries loo to finish near late session highs on heavier volumes (TYM6 over 1.9M) Thursday, p...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Bear Cycle Intact

- RES 4: 0.7187 High Mar 11 and the bull trigger

- RES 3: 0.7123 High Mar 18

- RES 2: 0.6995 20-day EMA

- RES 1: 0.6969 50-day EMA

- PRICE: 0.6855 @ 17:16 GMT Mar 31

- SUP 1: 0.6833 Low Mar 30

- SUP 2: 0.6767 High Jan 7

- SUP 3: 0.6705 Trendline support drawn from the Apr 9 ‘25 low

- SUP 4: 0.6701 38.2% retracement of the Apr 9 ‘25 - Mar 11 bull leg

A bear cycle in AUDUSD remains intact and the cross is trading at its recent lows. The pair has recently traded through the 50-day EMA and this undermines a bull theme and signals scope for a deeper retracement. Sights are on the 0.6800 handle ahead of an important trendline support at 0.6708 The trendline is drawn from the Apr 9 ‘25 low. Initial firm resistance is at 0.6995, the 20-day EMA.

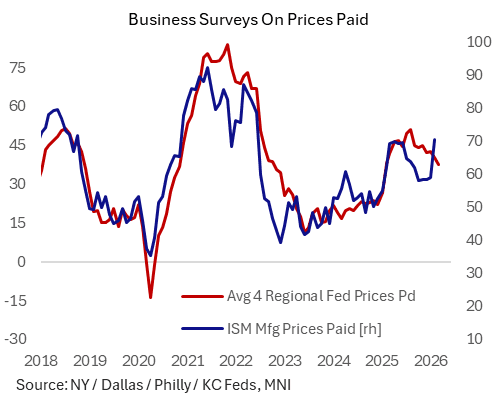

US PREVIEW: ISM Manufacturing Prices Paid Set To Remain Elevated (2/2)

The most notable aspect of February's ISM Manufacturing report was a jump in Prices Paid to 70.5 (+11.5pts) in Feb for its highest since Jun 2022 in a

resurgence of input cost pressure signs after four particularly stable months. That resurgence is seen continuing in March, with the Prices Paid gauge seen rising to 73.8 from 70.5 prior or a fresh post-Jun 2022 high.

- March saw mixed regional Fed prices paid dynamics: they fell sharply in New York and in Kansas City, but rose strongly in Philadelphia and Dallas, with Richmond reporting a diminished % Y/Y 12-month lookback. Overall the average actually fell to a 13-month low (ex-Richmond) though that was heavily influenced by what appears to be an outlier in the Empire State reading (36.6 after 49.1).

- In the Chicago Business Barometer, produced with MNI, Prices Paid gained 3.4 points in March, now at the highest level since last December. Respondents noted that metals were already driving cost increases, and that geopolitical tensions have driven up other costs too.

- March S&P flash PMI "Higher prices were widely linked to the war-related spike in energy costs and tightening supply conditions. Supplier delivery times in manufacturing lengthened to the greatest extent since October 2022."

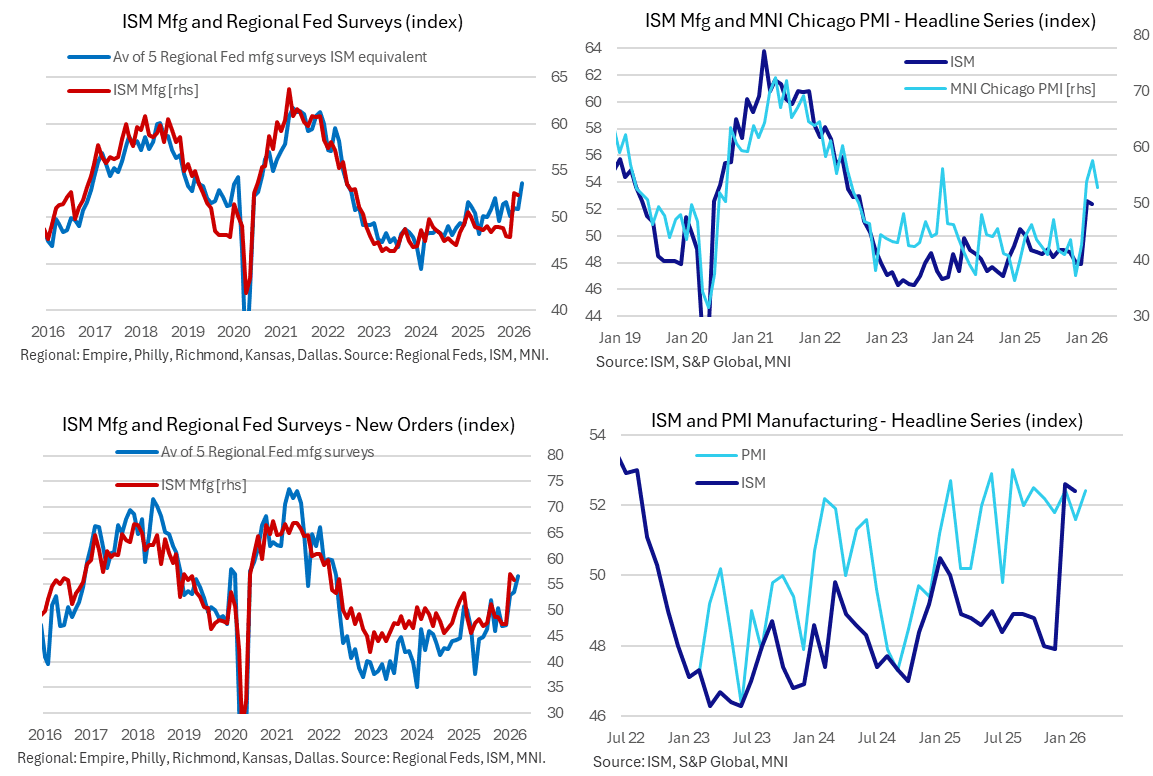

US PREVIEW: ISM Manufacturing Set For Solid March Despite Energy Headwinds (1/2)

March's ISM Manufacturing report is expected to show a steady headline PMI reading at 52.3 (52.4 prior), with a pickup in prices reflecting the ongoing energy shock from the conflict in the Middle East. New Orders are seen dipping to 55.0 after 55.8, with the Employment gauge up slightly to 49.0 after 48.8.

- Despite those expectations for a retreat, indicators of manufacturing activity in March have been largely positive.

- Regional Fed surveys' national ISM manufacturing equivalents were very strong across the board in 4 of 5 regions, each of which saw rises in March on an ISM basis, some to multi-year highs. The exception was Dallas which saw a pullback (51.0 from 55.2). Average New Orders across the 5 surveys jumped to 56.5 from 53.6 (led by KC), highest since April 2022; Employment rose to 51.3 from 49.0 for a 4-month high, again led by KC.

- The Chicago Business Barometer, produced with MNI, tempered 4.9 points to 52.8 after three consecutive rises with the decline driven by Employment, Production and New Orders. Lifts in Order Backlogs and Supplier Deliveries provided some offset. The ISM-weighted equivalent fell 3.9 points to 52.0.

- S&P Global flash US manufacturing PMI showed an above-expected 52.4 (cons 51.5) after 51.6 in February - a 2-month high, noting "a more upbeat perspective among manufacturers ... buoyed in part by fewer tariff-related worries".