CROSS ASSET: Risk Firms, But Market Sentiment Very Jittery On Iran Risks

Risk sentiment has calmed notably in recent dealings after the earlier sharp risk off. The risk off ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GLOBAL POLITICAL RISK: Gulf States Getting Closer To Joining Conflict - WSJ

Headlines have crossed from the WSJ that Gulf States, including Saudi Arabia, are considering joining attacks against Iran, see this link. It notes: "U.S. allies in the Persian Gulf are inching toward joining the fight against Iran, getting tougher following persistent attacks that have disrupted their economies and risk giving Tehran long-term leverage over the Strait of Hormuz." Adding, in relation to Saudi Arabia: "Crown Prince Mohammed bin Salman is now eager to re-establish deterrence and is close to a decision to join the attacks, the people said. It is only a matter of time before the kingdom enters the war, one of the people said."

- Oil prices have firmed a little as these headlines crossed. WTI is back above $90/bbl, up around +2.3% for the session (we opened up at $88.78/bbl)/ Brent crude is up around 1.6% to $101.50/bbl. We remain well off Monday highs though.

- US equity futures are softer, but up from session lows. The USD is higher against all the majors, with AUD and NZD down around 0.30%.

- Also impacting sentiment was earlier headlines from Iran around energy infrastructure assets being struck is also likely aiding firmer oil prices. Via BBG: "A gas pressure-regulation station and an associated administrative building were targeted in Iran’s central Isfahan province in recent US–Israeli attacks, the semi-official Fars news agency reports."

GOLD: Gold - Finds Demand Back Toward $4100, Trump Adds Tailwind To Reversal

The range overnight for gold was $4,099.17/oz - $4,512.76/oz, Asia is currently trading around $4420, +0.30%. After capitulating down around 9% at one point, demand returned toward the $4100 area, then Trump's comments saw it recoup most of those losses. That was a huge reversal, but an 18% collapse in 4 days probably pointed to most weak hands being squeezed out and starts looking like adding value again back toward $4000. The price action tells you the market had been caught wrong-footed but the retracement looked stretched. I suspect rallies back toward $4600-$4800 runs into sellers initially as those that held back use the bounce to pare back positioning. But I do think dips back toward $3800-$4100 will continue to see demand now and we will probably do some work in a choppy range as the market tries to find a base after this ugly washout.

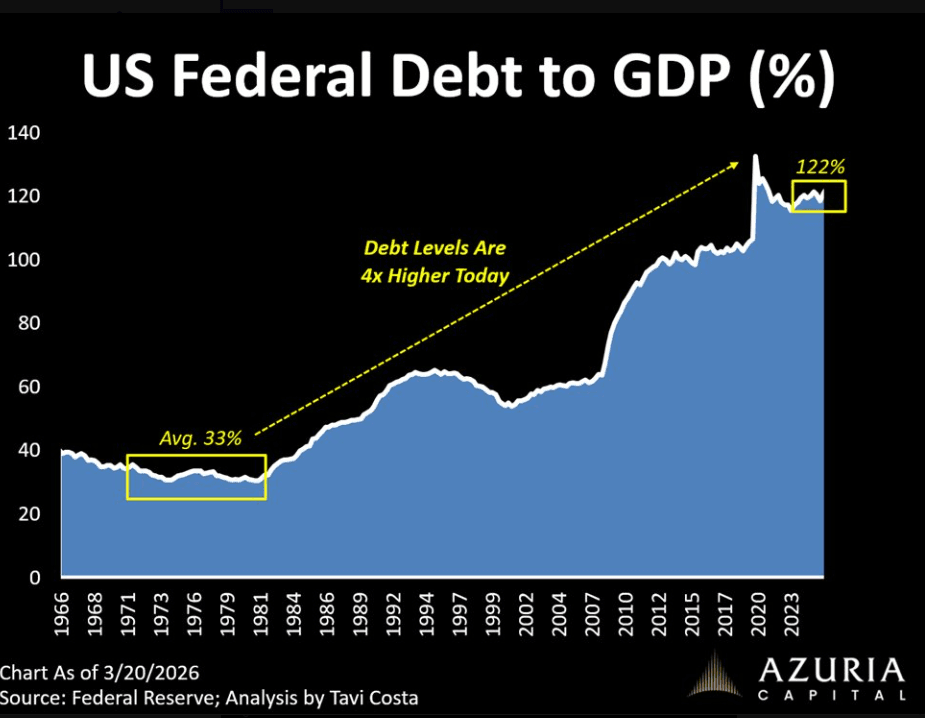

- Otavio Costa on X: “Seeing a narrative going around that gold is selling off because everyone is getting liquidated. Please. If that were the case, people would be selling stocks first. Gold is leading the downside. To me, this still looks like a market pricing in an extremely tight monetary policy to deal with a reacceleration of inflation. I really struggle with that view. This is not the 1970s. Back then, the Fed had room to act. Debt levels were low, and rates could be pushed into double digits without immediately destabilizing the system. Today couldn’t look more different.” See Fig.1 below.

- The XAU Average True Range(ATR) for the last 10 Trading days: $208.19/oz

Fig 1 : US Debt to GDP

Source: MNI - Market News/@TaviCosta

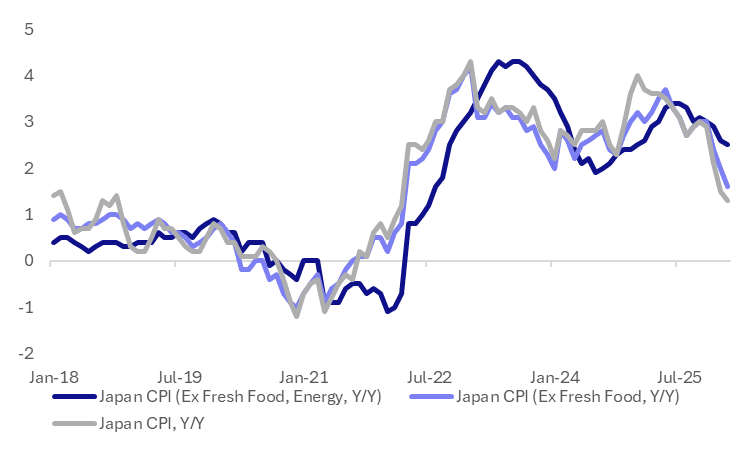

JAPAN DATA: Headline Weighed By Energy Subsidies, Core-Core, Services Y/Y Steady

Japan nationwide CPI for Feb was a touch below market forecasts. Headline CPI printed at 1.3%y/y (versus 1.5% forecast, which was also the prior outcome). Ex fresh food printed 1.6%y/y (1.7% was the forecast, prior printed at 2.0%). The ex fresh food and energy measure was 2.5%y/y, versus 2.6% forecast, which was also the Jan outcome. The close watched services inflation print was unchanged in y/y terms, coming in at 1.4%. We were up a modest 0.1% in m/m terms, although services cumulative gains since Nov last year are flat. This is unlikely to change BoJ thinking (around achieving its inflation target in the second half of its forecast horizon), particularly as the data pre-dates the surge in energy prices from March onwards. The central bank is likely to be focused on second round impacts, pass through to core inflation risks.

- Elsewhere in m/m terms, headline fell 0.2%, while ex fresh food was down 0.3%m/m. The ex fresh food, energy measure ticked up 0.1%m/m, the same as the Jan outcome. Goods prices were down 0.6%m/m.

- Utility prices fell 8.1%m/m, as the main drag (thanks to government subsidies in the space), but food prices -0.4%m/m (with fresh food down 2.8%m/m) also weighed. The main positive was entertainment, up 0.6% but this follows a 1.4% decline in Jan.

Fig 1: Japan CPI Y/Y Trends

Source: Bloomberg Finance L.P./MNI