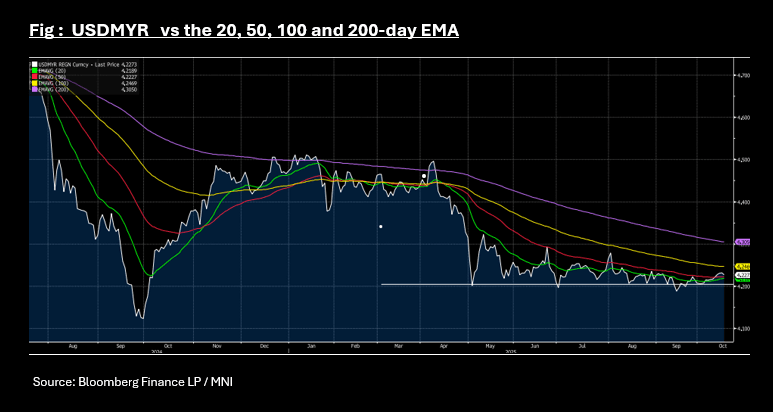

MYR: Ringgit Strong Up After Disappointing End to Wednesday

Oct-16 03:43

- Having delivered decent gains in morning trade yesterday, USDMYR failed to hold those gains and ended flat on the day.

- The ringgit is up +0.13% today at 4.2273, near to the 50-day EMA of 4.2228.

- The FTSE KLCI continues to underperform regional rallies, up just +0.15% today whilst other regional peers deliver strong gains. Bonds are flat with the MGS 10-Yr at 3.46% as it continues to range within 3.40 - 3.50%.

- Tomorrow sees the release of 3Q GDP with consensus forecasts for a moderation to 4.2% (from 4.4% in 2Q).

- Bank Negara Malaysia (BNM) remains optimistic about the trajectory of the ringgit, underpinned by Malaysia’s strong economic fundamentals and structural reforms.

- The central bank’s Governor Datuk said that the ringgit has strengthened against the US dollar by 5.8 per cent year-to-date amid a challenging global economic environment, at the launch of the Global Islamic Finance Forum (GIFF), suggesting that the ringgit could appreciate to RM4 against the US dollar by the end of the year, given Malaysia’s bright economic prospects.

- “While we do not target any level for the ringgit, we remain committed to ensuring the foreign exchange market remains resilient and stable. (as per BBG)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Weaker At Lunch, Koizumi/Kato Combo Weighs

Sep-16 03:22

At the Tokyo lunch break, JGB futures are weaker, -8 compared to settlement levels, after giving up early gains as trading resumed following the long weekend.

- Today, the local calendar will see the Tertiary Industry Index.

- (Bloomberg) “JGB traders are leaning hawkish as Shinjiro Koizumi taps Finance Minister Kato to steer his campaign. Traders see that pairing as the stronger ticket in the LDP race, and one that could give the Bank of Japan room to raise interest rates before year-end.”

- (Dow Jones) “The JGB yield curve may modestly flatten, assuming the Bank of Japan raises rates at a pace of 50bps per year, DBS Group Research's Eugene Leow says. The shape of the JGB yield curve depends largely on how aggressive Japan's central bank is likely to act in the coming few quarters, the senior rates strategist says.”

- Cash US tsys are marginally richer in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are flat to 1bp cheaper across benchmarks. The benchmark 10-year yield is 0.9bp higher at 1.603% versus the cycle high of 1.649%.

- Swap rates are flat to 2bps higher. Swap spreads are wider.

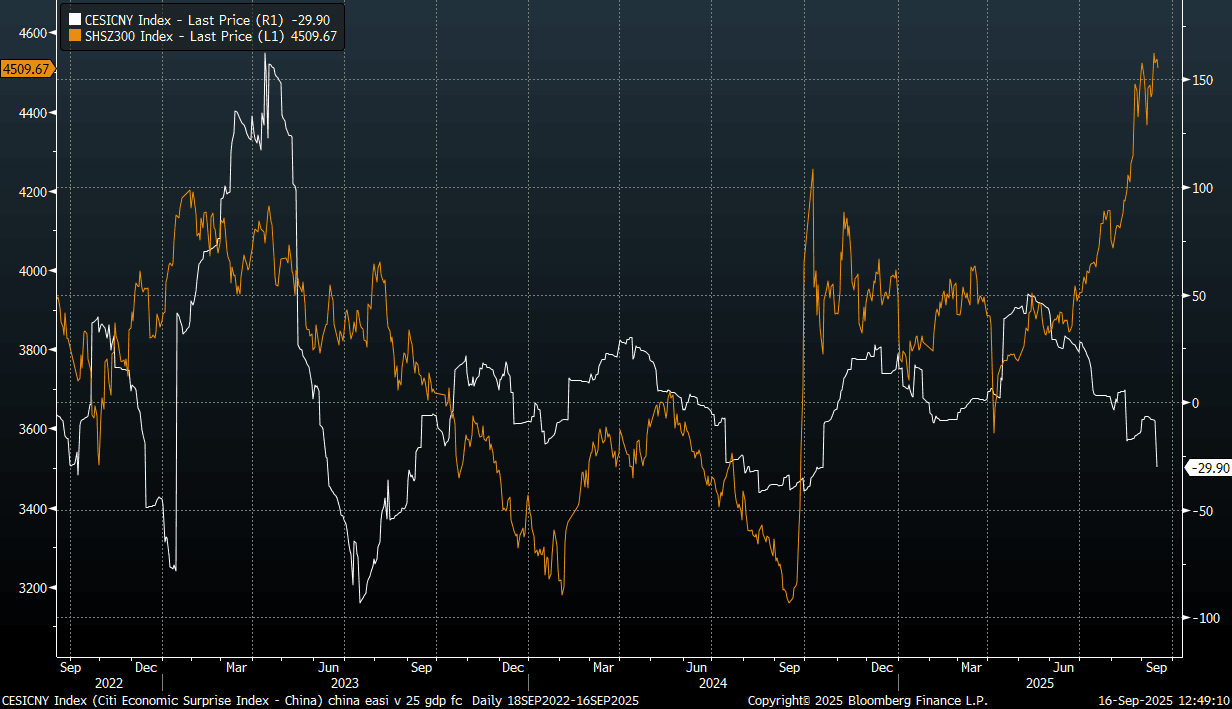

CHINA: China Surprise Index At Fresh 2025 Lows, But Local Equities Supported

Sep-16 03:06

Yesterday's softer than expected China data outcomes for August sent the Citi China economic surprise index (EASI) to fresh lows for 2025. It also widened the wedge between this surprise index and China equity trends, see the chart below. Even with mainland China equities down modestly so far today, this only closes the gap a touch (CSI 300 is off around 0.50%).

- To be sure, there have been divergences in the past but usually what we see is positive correlation between the two series, with positive data surprises usually coinciding with higher equity index levels. At face value, concerns around China growth momentum could weigh on equity trends at some stage.

- Still, we may remain divergent in the near term. Firstly, China isn't alone is having softer data outcomes recently relative to expectations. The other major economy EASIs have also softened (although they remain at higher levels relative to the China index). This is impacting these equity markets either, where in the US for example we have hit fresh record highs.

- Focus remains in the tech/AI space. For China the Chinext is up over 40% from start July levels, while the CSI 300 index is up a more modest 15% over the same period.

- The policy shift towards reducing excess capacity in parts of the economy may also weigh on economic activity but aid profitability. This has been a focus in the steel sector in recent months.

- Finally, softer data may encourage views that easier policy settings/economic support will come from the China authorities. Easing Fed expectations has certainly been a support for US/tech led global equity indices in recent months.

Fig 1: Citi China Surprise Index (White Line) and CSI 300 Equity Index (Orange Line)

Source: Citi/Bloomberg Finance L.P./MNI

INDONESIA: MNI Bank Indonesia Preview-Sep 2025: BI Pause, Monitors Events

Sep-16 02:49

- Download Full Report Here

- After Bank Indonesia (BI) has had to intervene to defend the rupiah over the last two weeks due to political unrest and then President Prabowo’s decision to remove respected finance minister Indrawati, rates are likely to be left at 5% on 17 September especially given the central bank’s focus on FX stability.

- BI has monthly meetings, so it can be cautious to ensure that the rupiah stabilises, that there aren’t significant portfolio outflows and to monitor political and fiscal developments.

- It expects inflation to stay within its target band this year and next and has eased 125bp so far this cycle and so it can continue to focus on FX stability and be cautious with further rate cuts. We expect it to retain its easing bias.