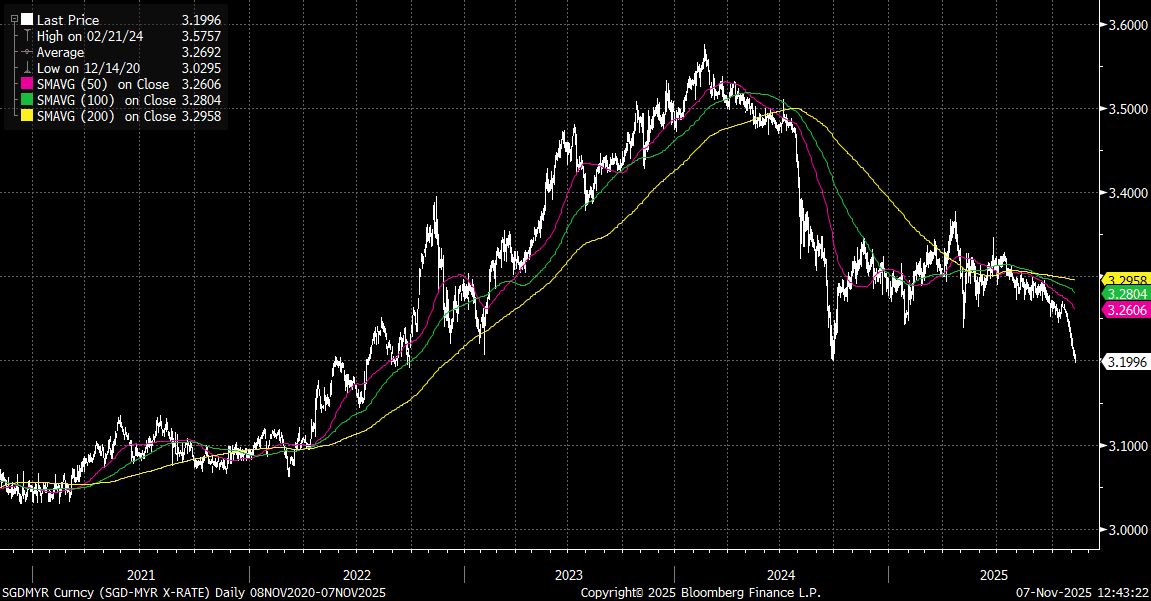

MYR: Ringgit Outperforms Amid Multiple Supports, SGD/MYR Under 3.2000

Ringgit is outperforming the mostly stronger USD/Asia trends elsewhere so far in Friday trade. The pair last near 4.1740/45, near fresh lows back to early Oct last year. Fresh lows from that period were around 4.1000, but given broader risk trends, playing MYR from the crosses may be a preferred option. Notably SGD/MYR is breaking lower today, testing under 3.2000, see the chart below. Less build up of tech related equity inflows may be a relative positive for MYR against the current macro backdrop.

- There will be some degree of correlation with the steady yuan backdrop, while yesterday's on hold BNM outcome is also likely feeding through in terms of ringgit resilience. The market outlook has little priced in terms of the outlook (from a cut standpoint)

- Softer growth in the Philippines has also likely provided a positive contrast for Malaysia (where recent growth outcomes have been more resilient, Q3 growth still above 5%y/y).

- Bond inflows for Malaysia for Oct, were also quite firm, back above $1bn, while markets like Indonesia were flat in that month. Relative fiscal/political stability in Malaysia may also be aiding such inflows.

Fig 1: SGD/MYR testing Under 3.2000

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

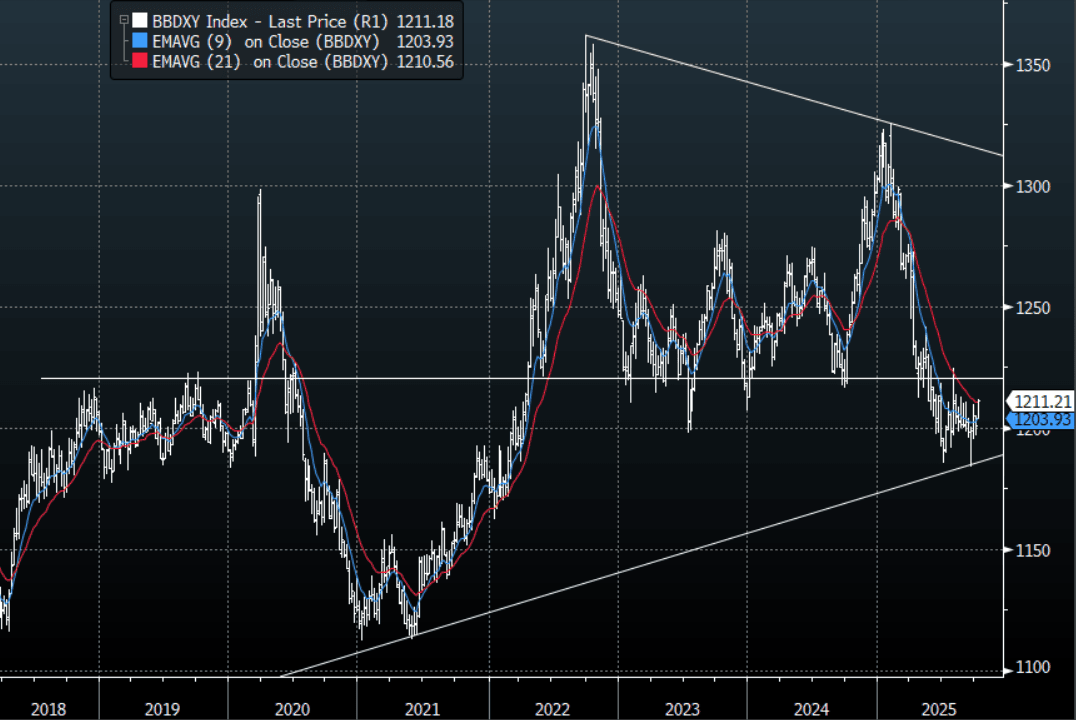

USD: BBDXY - Extends Gains Above 1200, Approaching Strong Resistance 1215-1225

The BBDXY range overnight was 1205.10 - 1209.29, Asia is currently trading around 1211, +0.15%. The USD got a welcome reprieve from the surge in USD/JPY, after failing to build any downward momentum below 1200 last week. This move extended overnight as the USD was able to build on this pullback. The 1215-1225 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts, but the weaker hands are definitely beginning to fold.

- MNI BRIEF: International Role Of The Euro Crucial Now -Lagarde. The international role of the euro can no longer remain a secondary issue in the context of trade tensions and global fragmentation, European Central Bank President Christine Lagarde said Tuesday, noting it was crucial to move from being a safe-haven currency to being a truly global one.

- David Lee on X: “Citadel CEO Griffin on Gold - “People are looking for ways to effectively de-dollarize or de-risk their portfolio vis-a-vis US sovereign risk.”

- Bloomberg - “Reserve Managers Are Falling Out of Love With the Dollar. Headline numbers for dollar reserves rose in the second quarter but, under the surface, demand for the US currency is waning. Foreigners' attitude to the dollar is changing. The shift won’t be abrupt, but steady and measured as it has been for the last five years or so during which we’ve seen dollar reserves as percentage of total FX + gold reserves falling from 52% to 40%.”

- Zerohedge on X: "Over the last 1 month the US dollar has been MORE volatile than the S&P 500. This has happened twice in the last 7 yrs (dec 2023 and jul 2025) - "long gold", "long bitcoin", "long stocks" is on everyone's favorite trade list / but in reality it seems to just all equate to "short fiat.” - Goldman

Fig 1: BBDXY Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

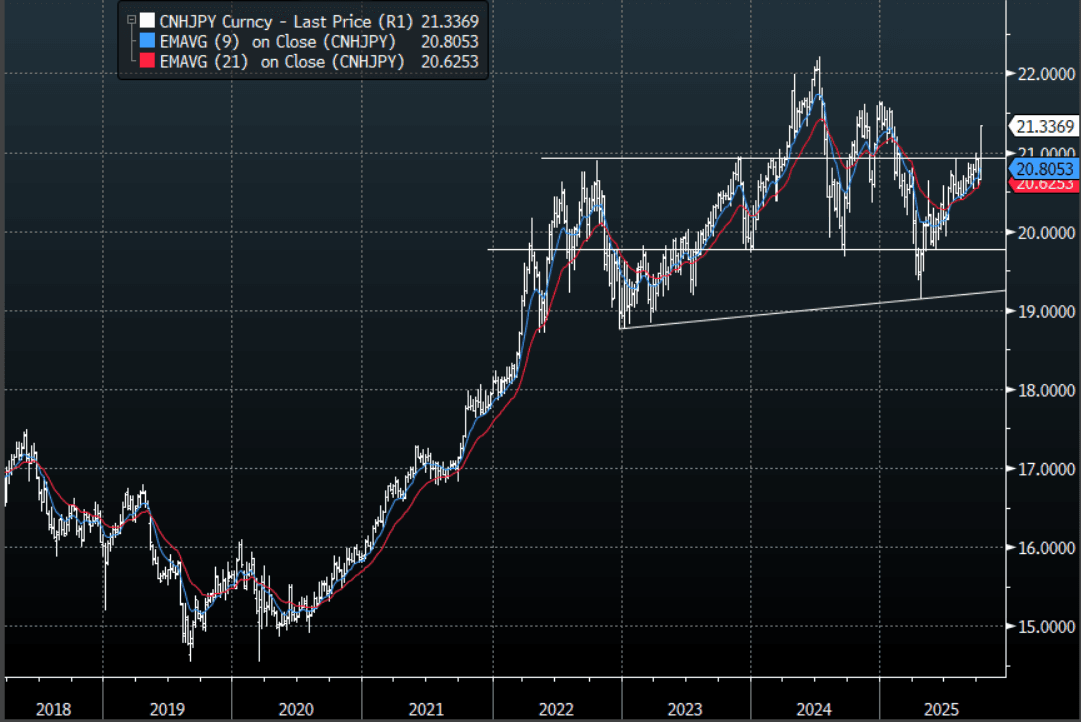

FOREX: JPY Crosses - Extend Move Higher, Breaking Pivotal Levels

US equities have shown the first signs of the huge rally potentially becoming exhaustive as momentum higher seems to be stalling. This morning US futures have traded a little higher, E-minis(S&P) +0.10%, NQZ5 +0.15%. Many crosses are extending breaks through some pivotal areas(CNH/JPY Above 21.00) and unless the government says something to contradict the markets thinking these could begin to gather momentum as carry trades are added to.

- EUR/JPY - Overnight range 175.79 - 177.15, Asia is trading around 177.35. The pair extended its gains building on the break above 175.50. Dips should now continue to be supported as the move higher looks to build momentum.

- GBP/JPY - Overnight 202.13 - 204.07, Asia trades around 204.35. This pair has finally found the momentum to accelerate above the 200.00 area. This should signal that this move could potentially trend higher from here, dips should now be supported with the focus turning toward the 2024 highs just below 208.

- NZD/JPY - Overnight range 87.42 - 88.13, Asia is currently dealing 87.70. This pair which was the best way to play a long JPY in the crosses has found some reprieve thanks to a dovish 50bps cut by the RBNZ. This might just be a stay of execution as the JPY crosses all look to be moving higher. If you wanted a long JPY trade in your basket as a hedge this would be it, a break above 89.00/90.00 and you are wrong.

- CNH/JPY - Overnight range 21.0757 - 21.2729, Asia is currently trading around 21.3300. The pair has broken convincingly above the 21.00 area and is building momentum above it. This could signal the start of the next leg higher targeting the 21.50/60 area first and then 22.00. Look for dips to now be supported.

Fig 1 : CNH/JPY Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBNZ: Larger Cut Gives Sluggish Economic Recovery Extra Boost, Easing Bias

The MPC discussed cutting the OCR by 25bp or 50bp and all members agreed the latter was appropriate given material spare capacity in the economy. Given that this is likely to persist for some time and that while the economy has begun to recover it remains lacklustre, further cuts bringing policy into stimulatory territory are likely. In line with this it said that “the Committee remains open to further reductions in the OCR”.

- The discussion included both 25bp and 50bp cuts. Arguments for 50bp to 2.5% included “prolonged spare capacity”, downside risks to growth and therefore inflation, moderation in domestic inflation resulting in greater confidence inflation is contained, and risk that households and businesses are being particularly cautious. The MPC wanted to send “a clear signal” to support the economy.

- Monetary policy lags, “signs of recovery”, time to ensure inflation returning to 2%, upside inflation risks from “constrained supply and cost pressures” and that signalling further easing for November would ease financial conditions argued for a more cautious 25bp cut.

- The MPC’s inflation concern appeared to shift this month. In August, it said it could ease policy further “if medium-term inflation pressures continued to ease as expected”, whereas this month it seemed more concerned with undershooting the target mid-point stating it “remains open to further reductions … for inflation to settle sustainably” near the 2% mid-point over the medium-term.

- It now expects inflation around 2% over H1 2026 rather than “by mid-2026” which may reflect its marginal revision to spare capacity and risks following the 0.9% q/q GDP contraction and recent modest activity data. Q2 GDP was impacted by a “large seasonal balancing item”, which the RBNZ expects to be reversed.

- There will be no press conference or forecast update today.