Ringgit Opening Relatively Unchanged.

Dec-20 01:16

USD/MYR is up at 4.5070 in Kuala Lumpur this morning; versus yesterday's close of 4.5057.

- This week’s move has seen the Ringgit break through the 200-day EMA of 4.4926, with the next technical level 4.60 and is currently -0.92% weaker for the week.

- Bloomberg Dollar spot index is +0.08% higher in the morning’s trading.

- USD/MYR one-month implied volatility is up at 5.470 from yesterdays close of 5.4075%

- Malaysia's 10-year bond yield is at 3.872%

- Malaysia 5 yr USD CDS at 45bps (yesterday’s close 43bp, 5-year low 38bp in 2020).

Headlines

- Malaysia has identified eight social media and online messaging platforms that will be required to obtain a license by next year, even as the government faces resistance to its plans to regulate the industry, the New Straits Times reported. (source: BBG).

Data Today

- CPI YoY (forecast +2.1% vs +1.9% prior)

- Foreign Reserves (US$118.3bn prior)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: CHINA SETS YUAN CENTRAL PARITY AT 7.1935 WEDS VS 7.1911

Nov-20 01:16

- CHINA SETS YUAN CENTRAL PARITY AT 7.1935 WEDS VS 7.1911

ASIA STOCKS: Asian Equity Flows Mixed, Philippines Continue To See Outflows

Nov-20 01:11

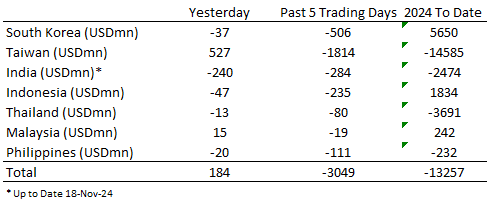

Taiwan saw its largest inflows since the US election, dip buyers emerged in Asia semiconductors stocks. Indonesia has now seen 10 straight sessions of outflows, while Philippines have seen 16 straight sessions of outflows.

- South Korea: Recorded outflows of -$37m yesterday, with a 5-day total of -$506m. YTD flows remain positive at +$5.65b. The 5-day average is -$101m, better than the 20-day average of -$156m but worse than the 100-day average of -$107m.

- Taiwan: Posted inflows of +$527m yesterday, totaling -$1.81b over the past 5 days. YTD flows remain negative at -$14.59b. The 5-day average is -$363m, worse than the 20-day average of -$216m and the 100-day average of -$212m.

- India: Experienced outflows of -$240m yesterday, with a 5-day outflow of -$284m. YTD flows are negative at -$2.47b. The 5-day average is -$57m, better than the 20-day average of -$251m but worse than the 100-day average of -$9m.

- Indonesia: Posted outflows of -$47m yesterday, bringing the 5-day total to -$235m. YTD flows remain positive at +$1.83b. The 5-day average is -$47m, slightly worse than the 20-day average of -$55m but better than the 100-day average of +$22m.

- Thailand: Recorded outflows of -$13m yesterday, with a total outflow of -$80m over the past 5 days. YTD flows are negative at -$3.69b. The 5-day average is -$16m, better than the 20-day average of -$27m but worse than the 100-day average of -$6m.

- Malaysia: Posted inflows of +$15m yesterday, reducing the 5-day outflow to -$19m. YTD flows remain positive at +$242m. The 5-day average is -$4m, better than the 20-day average of -$21m but worse than the 100-day average of +$4m.

- Philippines: Saw outflows of -$20m yesterday, with net outflows of -$111m over the past 5 days. YTD flows remain negative at -$232m. The 5-day average is -$22m, worse than the 20-day average of -$17m and the 100-day average of +$3m.

Table 1: EM Asia Equity Flows

JGBS: Cash Bonds Twist-Flatten

Nov-20 01:00

In Tokyo morning trade, JGB futures are stronger, +7 compared to settlement levels, but lower than overnight closing levels.

- Japan exports rose 3.1%y/y in Oct, above market expectations of a 1.0% gain. The prior outcome was -1.7% in y/y terms. Some tick up is not surprising given other trends in export linked economies in Northeast Asia.

- Exports may have received some benefit due to front loading ahead of the US election, although exports to the US were still -6.2%y/y. Exports to the EU were -11.3%y/y, while to the China rose +1.5%y/y and were positive to Asia more broadly.

- Imports rose 0.4%y/y, versus a -1.9%y/y contraction. This modest upside surprise left trade positions in deficit and slightly wider than forecast. We were at -¥461.2bn, which was consistent with recent trends.

- Cash US tsys are ~1bp richer in today’s Asia-Pac session after yesterday’s modest haven demand-induced gains.

- Cash JGB curve has twist-flattened, with yields 2bps higher to 2bps lower. The benchmark 10-year yield is 0.3bp lower at 1.065% versus the cycle high of 1.108%.

- The swaps curve has bear-steepened, with rates flat to 4bps higher. Swap spreads are mostly wider.