BOJ: Rinban Purchase Offer

The BoJ offers to buy a total of Y1.35tn of JGBs from the market:

- Y150bn worth of JGBs with <1 Year until maturity

- Y425bn worth of JGBs with 1-3 Years until maturity

- Y675bn worth of JGBs with 5-10 Years until maturity

- Y100bn worth of JGBs with 25+ Years until maturity

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

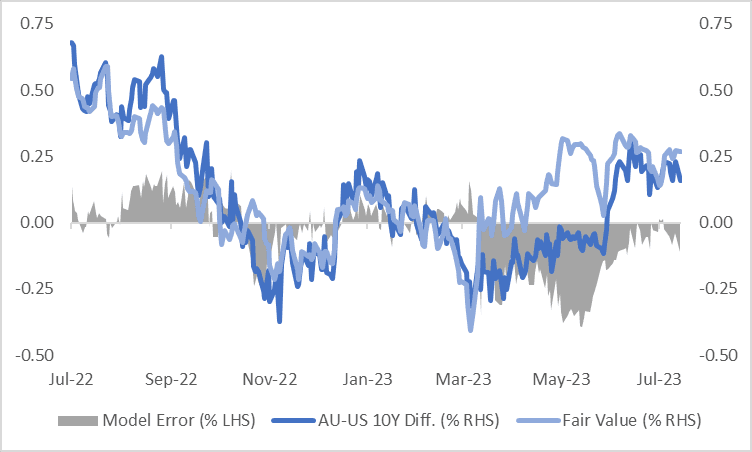

AUSSIE BONDS: AU-US 10-Year Yield Differential Is Too Tight

Today, the AU-US 10-year cash yield differential is tighter at +16bp after 10-year cash tsys finished 7bp cheaper in trade ahead of the weekend. It's important to note that cash tsys are closed in Asia today due to the observance of a national holiday in Japan. In contrast, 10-year cash ACGB is currently dealing 1bp richer at 3.98%, failing to sustain the break above the range it had been trading in since June 2022.

- At +16bp, the cash AU-US 10-year yield differential is currently within, albeit near the top, of the range of -30bp to +25bp that has been observed since November.

- The widening in the 10-year yield differential from -10bp in late May can be attributed to the divergent expected rate paths of the US Fed and the RBA. The RBA is expected to play catch up to the rate hikes that have already been implemented by the Fed. Currently, the RBA's cash rate stands at 4.10%, while the US Fed funds rate is at 5.0-5.25%.

- A simple regression of the AU-US cash 10-year yield differential and the AU-US 1Y3M swap differential over the current tightening cycle indicates that the 10-year yield differential is currently 11bp too tight versus its fair value (i.e., +16bp versus +27bp).

Figure 1: AU/US Cash 10-Year Yield Differential (%) Vs. Model Fair Value (%)

Source: MNI – Market News / Bloomberg

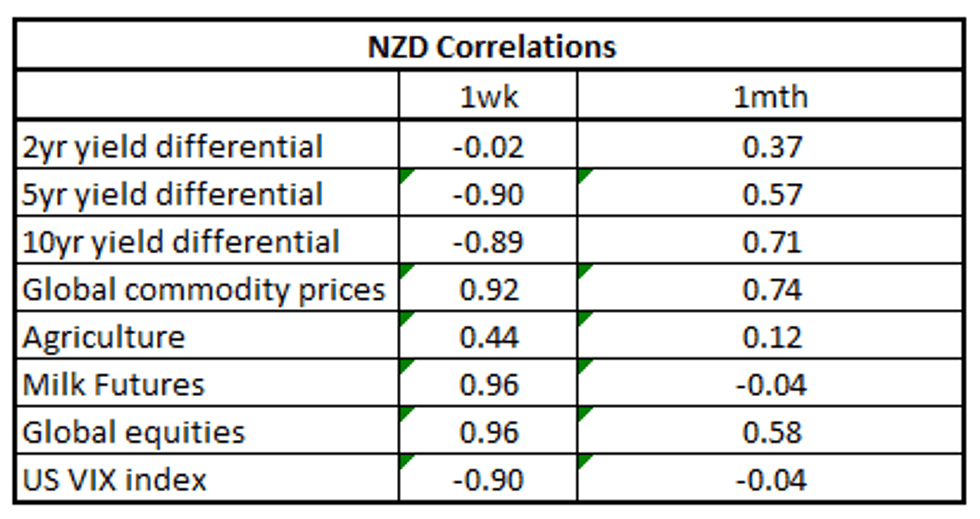

NZD: Global Equities, Milk & Commodities Dominant Drivers Last Week

NZD/USD correlations with global equities, milk futures and commodities have strengthened over the past week, standing out as a key macro driver in recent dealings. The table below presents levels of correlations between NZD and key macro drivers (note the yield differential reflects swap rates).

- Recent strength in NZD, up ~2.6% last week, looks to be associated with the recent strength in global equities, milk futures and commodities.

- The pair looked through narrowing 5-Year and 10-Year Yields differentials.

- Over the longer time frame rate differentials, commodities and global equities are the dominant macro drivers.

Fig 1: NZD/USD Correlation with Global Macro Drivers:

Source: MNI/Bloomberg

AUSTRALIA: Voters Turn Away From Main Parties - Newspoll

The July 16 Newspoll is showing that the incumbent Labor Party (ALP) has its lowest primary vote since the May 2022 election but on a two-party preferred basis moved in its favour, as reported by The Australian. Support for smaller parties rose at the expense of the two major parties.

- Support for the ALP fell 2pp to 36%, which is still above its 32.6% 2022 election result. The opposition Coalition fell 1pp to 34pp. Smaller parties and independents saw a 3pp rise in voter backing with Greens +1pp to 12%, One Nation +1pp to 7% and others/independents +1pp to 11%.

- The 2-part preferred breakdown rose in the ALP’s favour to 55:45 from 54:46.

- PM Albanese remains the preferred PM with his support rising 2pp to 54% and opposition leader Dutton’s declining 3pp to 29%.

- Some have speculated that PM Albanese’s future is linked to the outcome of the Voice referendum likely in October. Currently 41% of those surveyed in the July 16 Newspoll say they will vote Yes and 48% No as support continues to trend lower. To change the constitution a majority of people in a majority of state need to vote yes.