FED: Richmond's Barkin: Last Mile In Bringing Inflation To Target

Richmond Fed Pres Barkin (an FOMC voter in 2027) is as usual very noncommittal on his rate outlook in a speech Tuesday. Here's the concluding paragraph which reinforces MNI's view that Barkin is a little more hawkish than the overall FOMC median participant, but unlike some outright hawks remains relatively open-minded to rate cuts should the data make a compelling case:

- "We raised rates three years ago to bring inflation under control. As the inflation rate has fallen, we have been bringing rates back down toward neutral levels, reducing the fed funds rate 175 basis points over the last year and a half. I think of these cuts as having taken out some insurance to support the labor market as we work to complete the last mile to bring inflation back to target. So far, so good. But we know things change, and as they do, we remain ready to respond as appropriate."

- Note that he sees rates as having been brought down "toward" neutral levels and not necessarily at/below neutral, so there's some wiggle room here for supporting further easing.

- On the whole he continues to sound pretty cautious on making further cuts, noting the "remarkably resilient" economy "enabled by strong underlying dynamics", and "while we’ve made a lot of progress on inflation, it still remains above our target".

- And his business contacts continue to suggest that labor market layoffs aren't a major problem. That said, "low hiring hasn’t been translating into rising unemployment because the growth in labor supply has shrunk at about the same pace as labor demand. But slow job growth is not a comfortable place to be."

- And on policy patience in navigating an uncertain backdrop amid worsened data visibility related to the federal government shutdown: "as we move into 2026, it feels like the fog is starting to lift...we can better see the road ahead, but to echo all of our family road trips: Are we there yet? Not quite. We have some distance to travel before we get home."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

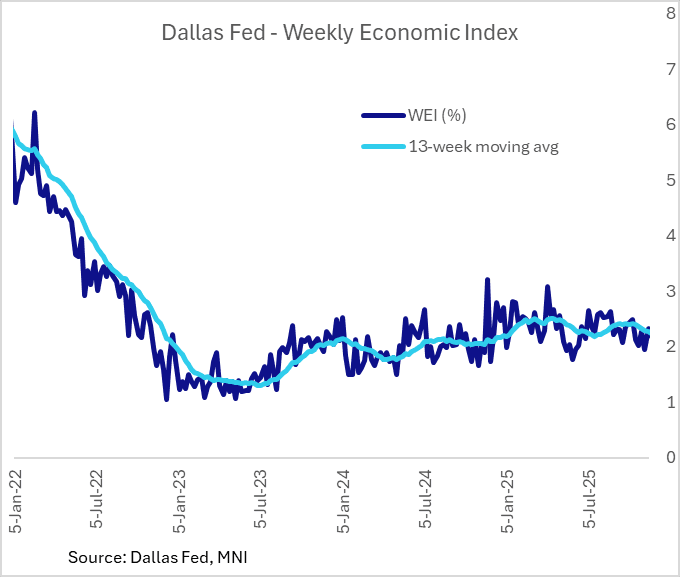

US DATA: Dallas Fed Weekly Index Ends Year Tracking Solid Q4 GDP Growth

The Dallas Fed's Weekly Economic Index concluded 2026 on a bright note, with the 4-quarter-scaled GDP growth rate ticking up in the Dec 27 week to 2.23% Y/Y from 2.21% prior.

- This should be caveated slightly by the fact that railroad traffic, electricity output, and fuel sales were not released for the latest week due to holidays, but it kept the 13-week (ie quarterly) moving average rate at 2.24% for a 6th consecutive week between 2.24-2.25%.

- The WEI was consistent with real GDP growth of 4+% Q/Q SAAR in Q3, which was closer to the mark than most (the official reading was 4.3%).

- Its final reading of Q4 means it tracked the equivalent of 2.5-3.0% Q/Q SAAR growth for the quarter, a little below the Atlanta Fed GDPNow estimate of 3.0%. We get the next Atlanta Fed reading on Monday after the ISM Manufacturing release for December.

US PREVIEW: Payrolls Seen Steadying Out In December After Noisy Oct/Nov (2/2)

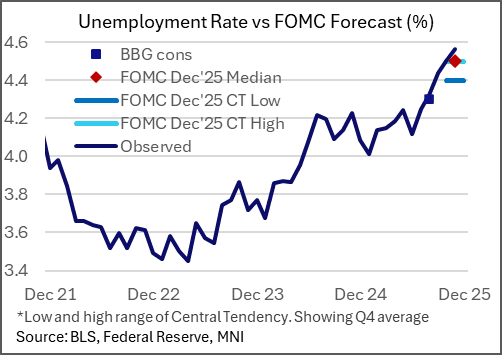

Next Friday's release of the December employment report is the highlight of the week's macro calendar. Our usual preview will be out early next week but early consensus expectations are for relatively steady readings vs November, with 55k nonfarm payroll gains (64k in Nov) and an unemployment rate of 4.5% (4.6% in Nov), with a slight moderation in participation and an uptick in hourly earnings growth.

- This is the last payrolls report before the FOMC's end-January meeting, at which participants would probably require substantially weaker-than-expected NFPs to spur even consideration of a another 25bp cut.

- That said the December data will carry more signal to the market and Fed than the highly unusual November report, which was both delayed and abbreviated (no October Household Report/unemployment rate) due to the federal government shutdown. Additionally, there were apparent distortions blurring the signal from the data, from the shutdown-driven jump in unemployment, to the new historical low for the household survey response rate and higher standard errors.

- Note that the FOMC's December 2025 median for the Q4 unemployment rate was 4.5% so a steady rate from November would imply a dovish "miss" to the upside though the significance will be muted by the noise in the household data. That said with Fed Chair Powell stating last month that nonfarm payroll gains are overstated by 60k/month, the consensus expectation will - to the leadership of the FOMC - imply only continued softness in the labor market, keeping further rate cuts in play this year.

- So far, indicators point to a relatively steady labor market overall in December vs November. The Chicago Fed's advance estimate of December's unemployment rate is 4.56% - which would be unchanged from November's unrounded BLS reading.

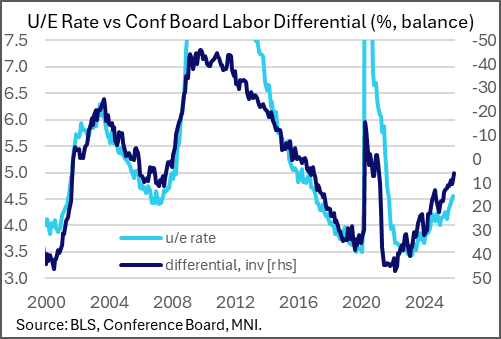

- The "labor differential" in the December Conference Board consumer survey its lowest since February 2021 at 5.9, pointing to a continued pickup in the unemployment rate, while the UMIchigan survey's expected job changes expected during the next year remains at levels consistent with meaningful monthly nonfarm payrolls contractions.

- However, jobless claims data for the reference week were on the lower side of the range seen in recent months' reference periods (initial 224k, continuing 1,913k in Dec 13 week).

EUROZONE ISSUANCE: EGB Supply – W/C 5 January

Germany, Spain, and France are scheduled to kick off auction issuance for the year in the upcoming week. We pencil in issuance of E55.5bln for the week, after this week saw no scheduled operations amid the holiday period. Slovenia will also hold a syndication in the week with syndications also possible from Austria, Belgium, Germany, Ireland, Portugal and the EFSF.

- Slovenia has already announced a mandate for a new 10-year SLOREP. We expect the transaction to take place on Monday 5 January with a E1.5bln size.

- Germany will be looking to kick off EGB auction issuance for the year on Tuesday with E6bln of the 2.00% Dec-27 Schatz (ISIN: DE000BU22114).

- Germany will return to the market on Wednesday with E6bln of the new Feb-36 Bund (ISIN: DE000BU2Z064). The coupon will be announced on Tuesday.

- Spain will come to the market on Thursday with a Bono/Obli/ObliEi auction, with the 2.70% Jan-30 Bono (ISIN: ES0000012O00), the 3.00% Jan-33 Obli (ISIN: ES0000012P74), the 3.45% Jul-43 Obli (ISIN: ES0000012K95) alongside the 1.15% Nov-36 Obli-Ei (ISIN: ES0000012O18) on offer. The combined auction size is to be confirmed on Monday.

- France will come to the market on Thursday to hold a LT OAT auction, selling a combined E11.5-13.5bln of the 3.50% Nov-35 OAT (ISIN: FR0014012II5), the 0.50% May-40 OAT (ISIN: FR0013515806), the 3.60% May-42 OAT (ISIN: FR001400WYO4) and the 3.75% May-56 OAT (ISIN: FR001400XJJ3).

NOMINAL FLOWS: The upcoming week will see no redemptions. Coupon payments for the week total E4.1bln of which E4.0bln are from Germany. This leaves estimated net flows for the week at positive E51.4bln, versus negative E1.4bln this week.