AUSSIE BONDS: Richer With US Tsys, RBA Staffers: Cash Rate Hinges On Q4 Data

ACGBs (YM +4.0 & XM +4.0) are stronger after US tsys finished 6-9bps richer.

- US tsys turned to alternative employment data due to the ongoing US Govt shutdown. Revelio Labs' estimate of October nonfarm payrolls growth came in at -9.1k vs +33.0k prior (rev from +60.1k) and August's actual figure reported by the BLS of +22k (Revelio estimates Aug at +14.5k). That is the first negative M/M reading for the Revelio series since May.

- MNI: RBA Cash Rate Strategy Hinges On Q4 Data - Fmr Staffers. A further 1% quarter-on-quarter rise in trimmed-mean inflation in Q4 will pressure the Reserve Bank of Australia to raise its 3.6% cash rate in 2026, but geopolitical and global economic risks are likely to encourage caution, and higher unemployment could eventually prompt a return to easing later in the year, former staffers told MNI.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at +24bps.

- The bills strip is flat to +3 across contracts, with a flattening bias.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at an 11% probability, with a cumulative 21bps of easing priced by mid-2026.

- Today, the local calendar will see Foreign Reserves.

- The AOFM also plans to sell A$800mn of the 3.00% 21 November 2033 bond.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Reversal Lower Extends

- RES 3: 95.960 - High Apr 7 (cont.)

- RES 2: 95.875 - High Jul 2 (cont.)

- RES 1: 95.780 - High Sep 12, 18 and 19

- PRICE: 95.625 @ 16:28 BST Oct 07

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures are trading closer to their recent lows. It is still possible that the recent move down is a correction. Near-term resistance to watch is 95.780, the Sep 12 high. A clear break of this level would signal scope for a continuation higher and open 95.875, the Jul 2 high on the continuation chart. On the downside, key short-term support to watch has been defined at 95.510, the Sep 3 low. Clearance of this level would instead be bearish.

AUSSIE BONDS: Richer With US Tsys

ACGBs (YM +1.5 & XM +3.0) are stronger after US tsys finished 2-3bps richer across benchmarks.

- MNI BRIEF: Federal Reserve Governor Stephen Miran said Tuesday the central bank needs to lower interest rates and that stable long-term interest rates flow from success in achieving the central bank's dual mandate goals. "Most people think that achieving moderate, long-term interest rates will naturally come out of achieving maximum employment and stable prices," he said in Q&A at an event hosted by the Managed Funds Association. "I agree with that. I could imagine there being sort of tail scenarios of the world in which that's not the case. But I don't think that any of those tail scenarios are remotely describing a reality that I see now, or that I would expect to see."

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at +24bps.

- The bills strip is +1 to +2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in November is given a 40% probability, with a cumulative 14bps of easing priced by year-end.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond today.

- Today, the local calendar will also see Foreign Reserves data.

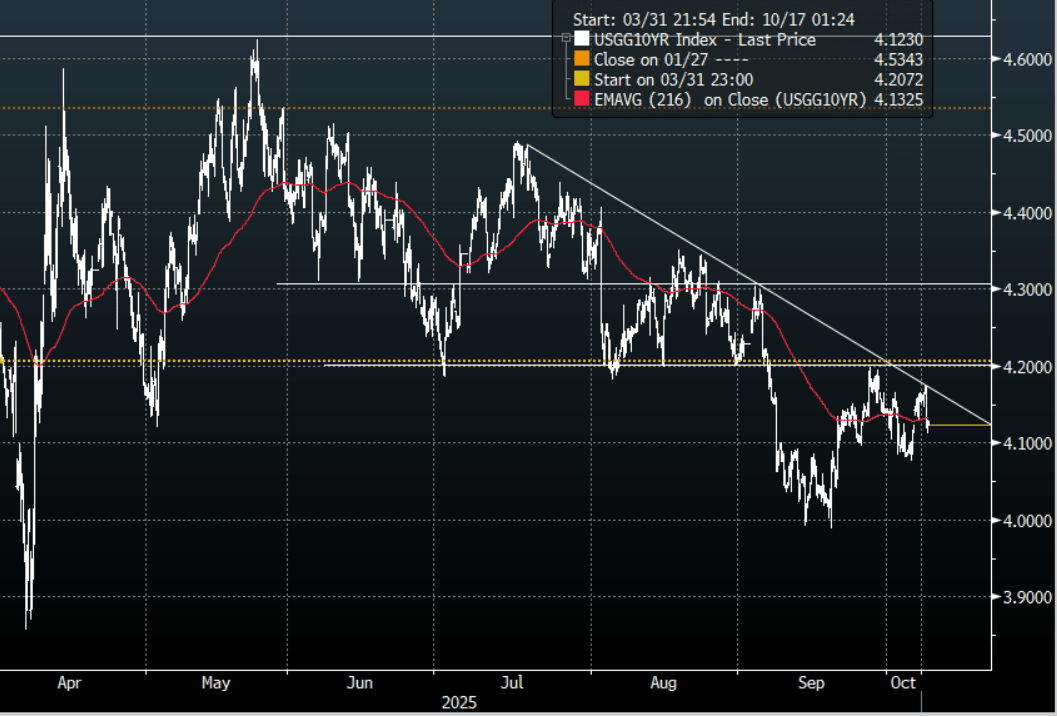

US TSYS: US Yields Turn Lower

TYZ5 reopens at 112-21, down 0-00+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.1114% - 4.1753%, closing around 4.127%.

- Treasury yields moved broadly lower overnight; (2s10s -0.63 at 55.730, 5s30s +0.85 at 102.031).

- 10-Year yields bounced to start the week on the back of global politics but remains subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around the 4.20% area initially and look to fade any move higher for now.

- MNI BRIEF: Third Mandate Flows From Dual Mandate Success-Miran. Federal Reserve Governor Stephen Miran said Tuesday the central bank needs to lower interest rates and that stable long term interest rates flow from success in achieving the central bank's dual mandate goals. "Most people think that achieving moderate, long term interest rates will naturally come out of achieving maximum employment and stable prices," he said in Q&A at an event hosted by the Managed Funds Association. "I agree with that. I could imagine there being sort of tail scenarios of the world in which that's not the case. But I don't think that any of those tail scenarios are remotely describing a reality that I see now, or that I would expect to see."

- MNI US DATA: Consumer Inflation Expectations Firm Mildly In September - NY Fed. The NY Fed consumer survey saw inflation expectations on balance increase in September. 1Y and 3Y expectations remain comfortably rangebound whilst the 5Y approach is at the high end of its short historical range.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P