AUSSIE BONDS: Richer With US Tsys

ACGBs (YM +1.5 & XM +3.0) are stronger after US tsys finished 2-3bps richer across benchmarks.

- MNI BRIEF: Federal Reserve Governor Stephen Miran said Tuesday the central bank needs to lower interest rates and that stable long-term interest rates flow from success in achieving the central bank's dual mandate goals. "Most people think that achieving moderate, long-term interest rates will naturally come out of achieving maximum employment and stable prices," he said in Q&A at an event hosted by the Managed Funds Association. "I agree with that. I could imagine there being sort of tail scenarios of the world in which that's not the case. But I don't think that any of those tail scenarios are remotely describing a reality that I see now, or that I would expect to see."

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at +24bps.

- The bills strip is +1 to +2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in November is given a 40% probability, with a cumulative 14bps of easing priced by year-end.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond today.

- Today, the local calendar will also see Foreign Reserves data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: NFP Sees Yields Break Lower

TYZ5 reopens at 113-11, down 0-01+ from closing levels in today’s Asia-Pac session.

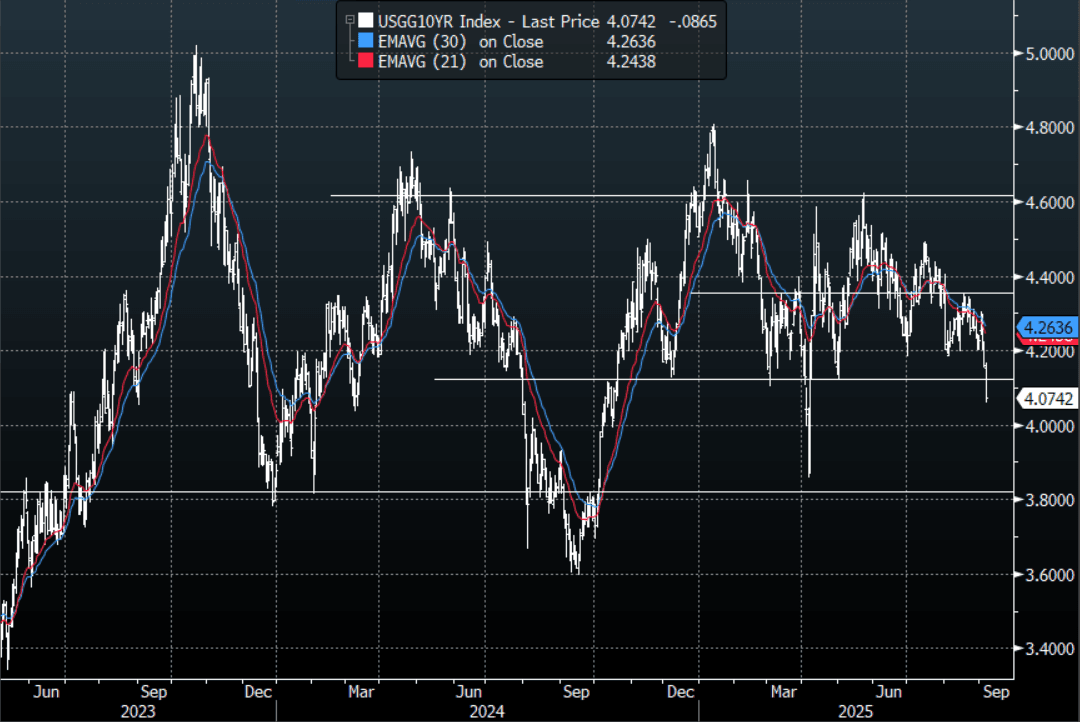

- Friday night the US 10-year yield had a range of 4.0609% - 4.1664%, closing around 4.074%.

- Treasury yields accelerated lower Friday night as data continues to show the labour market is potentially rolling over; (2s10s -0.79 at 56.297, 5s30s -3.24 at 117.355).

- MNI US DATA: Another Tepid Month Of Job Creation Although June Remains The Low. Nonfarm payrolls growth was softer than expected in August at 22k (sa, cons 75k) along with a two-month downward revision of -21k coming entirely in June. The private sector saw a similar story on balance, with a slightly smaller miss with 38k (sa, cons 75k) but a larger downward revision of -36k.

- MNI US DATA: AHE On The Soft Side, Especially Considering Lower Hours. For completeness, AHE on the soft side of 0.3% M/M rounding (cons 0.3) although the non-supervisory category was strong.

- 10-Year Yields have broken through its support as the market reacts to a labour market that is rapidly cooling. This move should now see buyers return on bounces with the first buy-zone back towards 4.20%. First target the 4.00% zone then the 3.80% area.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

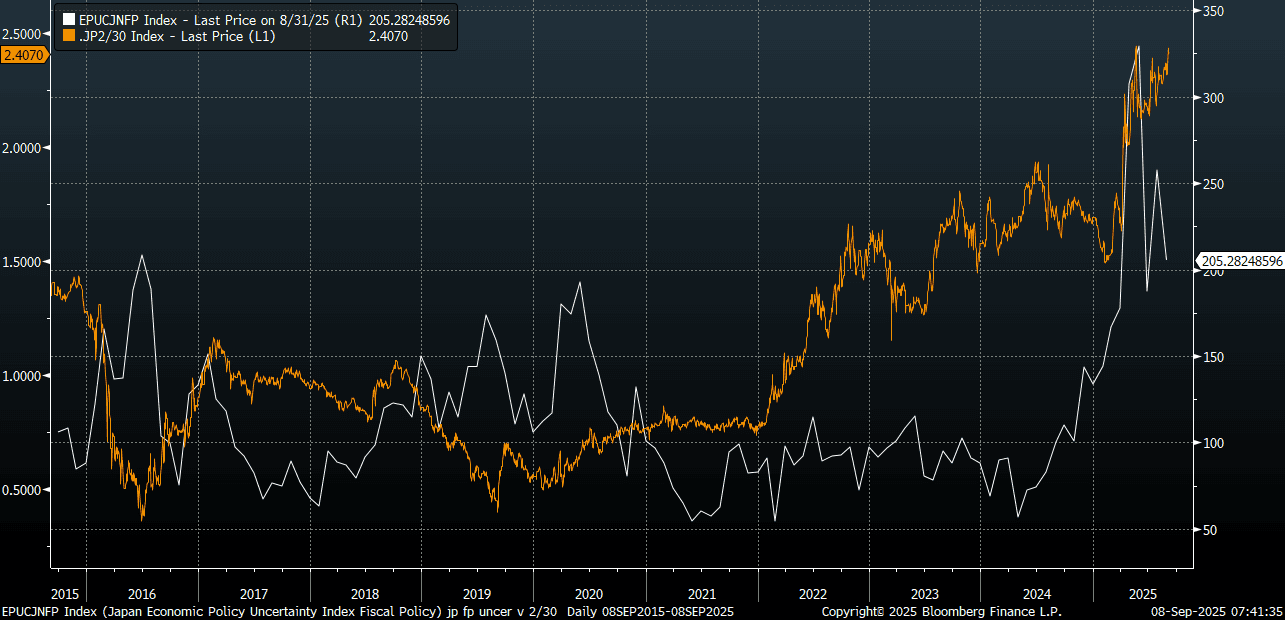

JAPAN: Ishiba Stepping Down Injects Fresh Uncertainty Into Macro Outlook

Weekend news that Japan PM Ishiba will be stepping down injects fresh political uncertainty into Japan's broader economic outlook. Japan's LDP was set to hold a leadership vote on Monday, but that has now been cancelled following the resignation of leader Ishiba on Sunday. Odds that PM Ishiba would leave office spiked in the aftermath of the LDP losing its majority at the July upper house elections. Still, last week we were around the 20-35% region per Polymarket odds on Ishiba being the first leader out in 2025. That ended Friday at 44%. Hence the weekend outcome will not come as a total surprise to the market.

- Focus will now turn to the LDP leadership race. When Ishiba secured the PM position last Oct, the runner up was Sanae Takaichi. Via ABC news: "A Nikkei survey held at the end of August put Ms Takaichi as the most "fitting" successor to Ishiba."

- Takaichi could arguably generate the most significant market reaction if she is successful becoming the new PM, as she has been outspoken in terms of being more dovish in terms of the BoJ outlook and looking to boost fiscal spending.

- This comes at a time when back end yields are already around record highs, amid fiscal pressure concerns in Japan and more broadly. The chart below plots the Japan JGB 2/30's curve versus the local economic policy uncertainty index (for fiscal policy).

- Via BBG: "“If Ms. Takaichi is appointed, bond selling could intensify due to the risk of a credit rating downgrade,” Sumitomo Mitsui Trust’s Inadome said. In that scenario, “we could see a triple dip: falling bond prices, a weaker yen, and declining stock prices.”

- Other candidates are likely to include Shinjiro Koizumi, the current agricultural minister, as well as Takayuki Kobayashi, the current chief cabinet secretary.

- Also note, via ABC news: "Since the party does not have a majority in either house, it is not guaranteed that the LDP president will become prime minister. In Japan, the prime minister is chosen by parliament, not automatically by the ruling party."

- Market reaction this morning has been for yen to weaken, off around 0.45% versus the USD. Focus will also be on equities and particularly the bond market when they open later.

Fig 1: Japan Fiscal Policy Uncertainty & JGBs 2/30 Curve

Source: Bloomberg Finance L.P./MNI

AUSSIE 3-YEAR TECHS: (U5) Bounces Further Off Support

- RES 3: 97.190 - High May 5 2023

- RES 2: 96.932 - 76.4% of Mar-Nov ‘23 bear leg

- RES 1: 96.860 - High Apr 07

- PRICE: 96.580 @ 15:59 BST Sep 5

- SUP 1: 96.430/95.900 - Low Sep 3 / Low Jan 14

- SUP 2: 95.760 - Low 14 Nov ‘24

- SUP 3: 95.480 - Low Jan 11 2023 and a major support

Aussie 3-yr futures are trading further off the lows. A resumption of gains from here would further narrow the gap with resistance at 96.730, the Sep 17 ‘24 high, leaving 96.860 as the next key level. Any continuation lower would instead strengthen a bearish threat. This would refocus attention on 95.760, the 14 Nov ‘24 low. Conversely, a reversal higher would open 96.860, the Apr 7 high.