EU ENERGY SECTOR: Repsol: Soft Trading Update

(REPSM; Baa1/BBB+/BBB+) Q4 production looks like a 3.9% miss while refining margins are a 2.5% beat...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

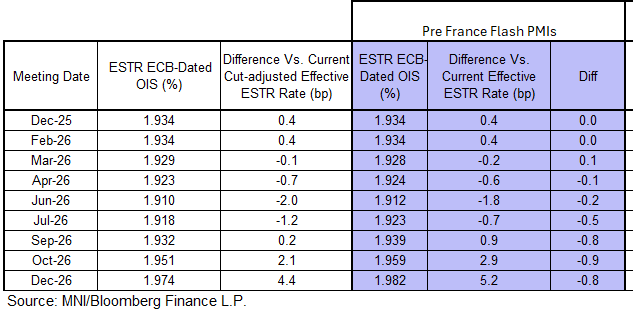

STIR: Slightly Soft December Flash PMIs Remove A Basis Point Of Hike Pricing

The weaker-than-expected German and French flash December PMIs remove about a basis point of implied ECB rate hikes through the end of next year. ECB-dated OIS now price ~4.5bps of easing through December 2026.

- There’s not enough in the reports to meaningfully change the recent narrative around improving growth momentum. However, sluggish new orders and subdued services confidence highlight that there are still risks to growth in both directions – we expect President Lagarde to stress this at Thursday’s press conference (even if she concedes that overall risks are now roughly balanced).

- With implied hike pricing paring back a little further, the bar to a material market reaction on Thursday inches higher. Focus remains on the ECB’s updated macroeconomic projections and the characterisation of risks.

- Euribor futures are now flat to +1.0 ticks through the blues, with light upside concentrated in the whites/reds.

SOFR: SFRZ6 Sold

Ongoing activity in SOFR futures, with SFRZ6 seeing 5K sold (and more trading on the follow) at 96.885 ahead of the flash PMI data out of France and Germany. Small bid there last.

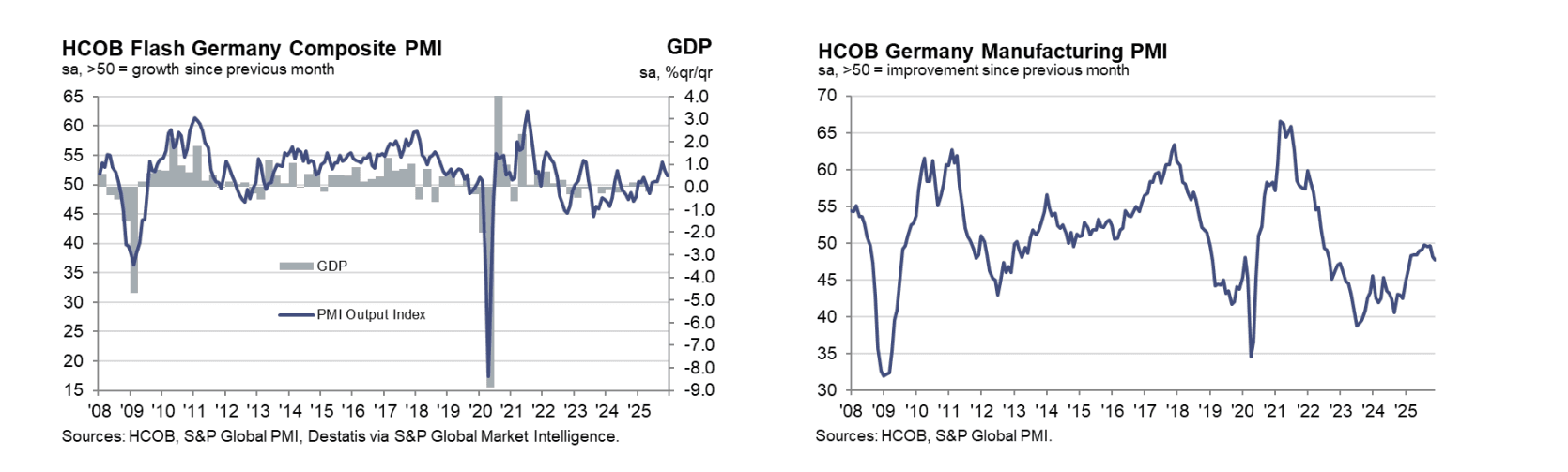

GERMAN DATA: Dec Flash PMIs: Both Sectors Weaker Than Expected

The German composite PMI remains in expansionary territory, but the 51.5 December flash reading (vs 52.4 cons) was the second consecutive pullback from 52.4 in November and 53.9 in October. Manufacturing saw a deeper retracement than services to a 10-month low, but both sector's PMIs were weaker-than-expected.

- MNI: GERMANY DEC FLASH MANUF PMI 47.7 (48.6 FCAST, 48.2 NOV)

- MNI: GERMANY DEC FLASH SERV PMI 52.6 (53.0 FCAST, 53.1 NOV)

The details of the release show plenty of services/manufacturing divergences across subcomponents:

- Weak export demand dragged on manufacturing orders, potentially an ongoing impact of higher US effective tariff rates.

- Despite the overall services PMI remaining in expansionary territory, the fall in year-ahead business confidence was driven exclusively by that sector – manufacturing confidence rose relative to November.

Key notes from the release:

- “Total inflows of new business were unchanged in December compared with the month before, after having risen in both October and November. Service providers reported a modest increase in new work that was the weakest in the current three month period of expansion”.

- “Demand conditions meanwhile deteriorated in the manufacturing sector, with new orders falling for the third time in four months and at the quickest rate since January. This partly reflected a deepening decline in factory export sales.”

- “Concerns about the health of the economy, the unsettled geopolitical environment and the competitiveness of German companies weighed on business confidence in December”….“ That said, the overall drop in expectations was driven exclusively by the service sector and masked an uptick in confidence among manufacturers”

- “On the labour market front, December’s flash data indicated a slight reduction in employment”…. “reflecting a pick-up in the pace of job creation in services and a slightly slower decrease in factory staffing levels”

- “Services firms noted the sharpest rise in input prices since February, while manufacturers recorded an increase in average purchasing costs prices for the first time since January 2023”…“ Strong competition for new work led to another modest decrease in average manufacturing output prices in December. However, due to a faster rise in prices charged by service providers, the overall rate of output price inflation ticked up”