IRAN: Reports Of Rift In Tehran Over Delegation Composition (1/2)

UK-based outlet Iran International reports : https://www.iranintl.com/202604104967of a rift at the t...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Futures Stabiles Ahead Of Round Number Support

A pullback in crude oil allowed gilts to stabilise, with futures basing ahead of 90.00, protecting next support at the March 6 low (89.43). Yields 8-10bp higher, 5s under the most pressure.

- Oil market developments continue to dominate any (limited) local developments.

- Fiscal support from an elongated conflict in the Middle East presents a potential headwind over the medium-term.

- BoE-dated OIS has stabilised around pricing 5bp of rate cuts.

- A BBG report has flagged real money demand for gilts in recent sessions, noting that “a dramatic selloff in the UK’s bonds since conflict broke out in the Middle East is a buying opportunity for a handful of investors willing to brave the volatility. Fund managers at the likes of Russell Investments, Marlborough Investment Management and Nedgroup Investments have grabbed exposure to gilts in recent days, during wild gyrations that drove short-term yields to the highest in nearly a year”.

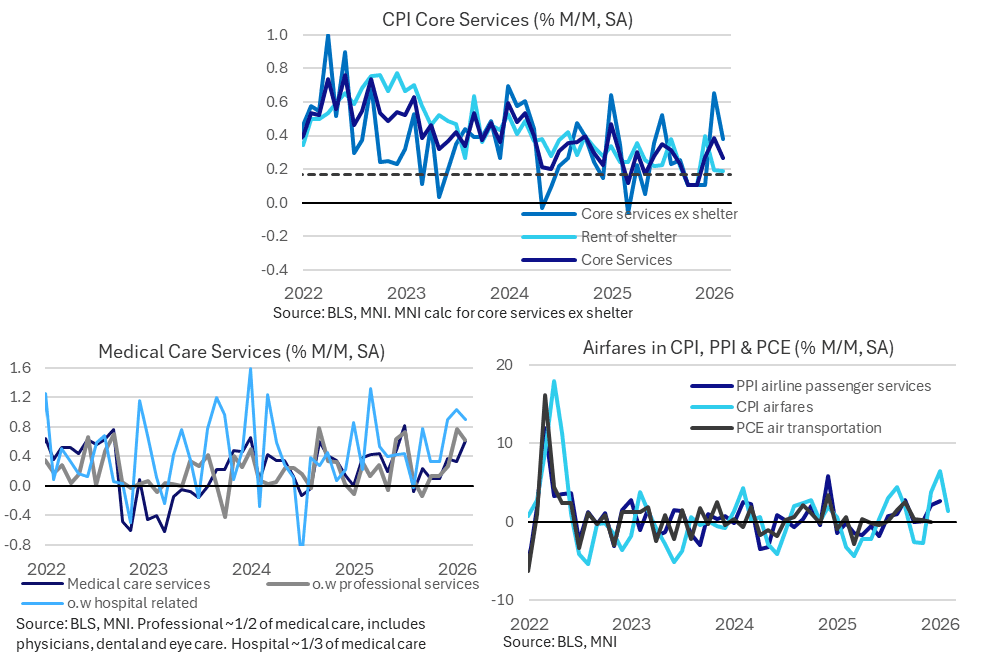

US DATA: Core Services Inflation Remains Elevated, Mixed PCE Implications

Supercore CPI (services ex-housing) registered a rise of 0.35% in February, well down from 0.59% prior but a little on the hotter side of expectations (0.27%). Overall core services were down to 0.27% (exactly as expected) after 0.39% prior, returning to December's still-elevated level. When we look at the details, there are mixed risks to the core PCE readthrough versus its CPI counterpart.

- Airfares (0.9% of CPI basket) came back to earth as expected at 1.4% after January's 6.5%, though lodging (1.3% of CPI basket) posted a slightly bigger upside reversal than anticipated at 1.0% (-0.1% prior), though both of these categories are notoriously volatile. We also note auto insurance (2.7% of CPI) on the soft side of expectations at -0.3% after -0.4% in January.

- Note though, airfares and auto insurance coming in on the weaker side won't help bias core PCE estimates lower, since these categories are taken from the PPI report, not CPI.

- Medical care services - 7% of the CPI basket - posted a jump to 0.6% after 0.3%, highest since July, led by professional services (0.6% after 0.8%) and hospital/related services (0.9% after 1.0%). This appeared to be a surprise with analysts suggesting that January's burst would be reversed. Dental prices - a core PCE contributor from the CPI report - jumped 1.3% M/M after 0.9% for the biggest rise since July 2025. Note that PCE takes physician services prices and hospital service inflation from the PPI report.

- Elsewhere we saw a large drop in recreation services (-0.2% after +0.4%) for the lowest since August 2025 in this category worth 3.2% of the overall CPI basket. Education and communication services (5% of CPI) were relatively steady at 0.3% after 0.4%, but other personal services prices fell 0.2% after +1.6%.

OIL: IEA Statement Due Imminently

IEA Executive Director Birol will issue a statement at 15:00 CET/14:00 London/10:00 NY.

- We expect this to include the Agency's recommendation re: a coordinated strategic oil reserve release.