STIR: Repo Reference Rates

Feb-28 13:05

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.741T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $664B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $652B

- (rate, volume levels reflect prior session)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: What to Watch: Tsy Quarterly Refunding, Borrow Estimates

Jan-29 12:59

- Relatively quiet start to the week regarding data with Dallas Fed Mfg Activity at 1030ET while the US Tsy auctions $79B 13W, $70B 26 Bill at 1130ET.

- Today's focus is on Treasury’s Quarterly Refunding process for the Feb-Apr quarter with borrowing estimates released at 1500ET. The refunding announcement is scheduled for Wednesday at 0830ET.

- Meanwhile, main focus for the week is on the Fed's FOMC policy annc Wednesday at 1400ET, followed by January employment data Friday morning.

- Flood of earnings announcements this week: Nucor Corp, Corning, Pfizer, UPS, GM, MSFT, Alphabet, Starbucks, Boeing, Boston Scientific. Mastercard, MetLife and Meta, all by Wednesday.

STIR: Goldman Sachs On ECB Pricing Into CPI

Jan-29 12:50

Goldman Sachs write “although we think markets can price more ECB easing over 2024 than the ~145bp priced currently (and continue to recommend April-December 2024 ECB OIS flatteners) - the risk that an initially reluctant ECB is forced to deliver larger increments in H2 has arguably diminished after last week’s ECB.”

- “Against that backdrop, markets' ability to price 50bps cuts is more likely to hinge on activity and labour market resilience; we also note that President Lagarde refused to provide guidance on the neutral rate, as a possible clue for the speed of adjustment.”

- “Our economists are expecting a decline in core HICP to 3.2% in January, which we think will be consistent with the path towards our April cut base case, but any substantial downside surprise could see March pricing shift towards easing.”

- “In contrast, an upside surprise - given uncertainties around one-off adjustments to taxes and energy subsidies - may not have much of an effect given only 5bps of cuts are priced for March.”

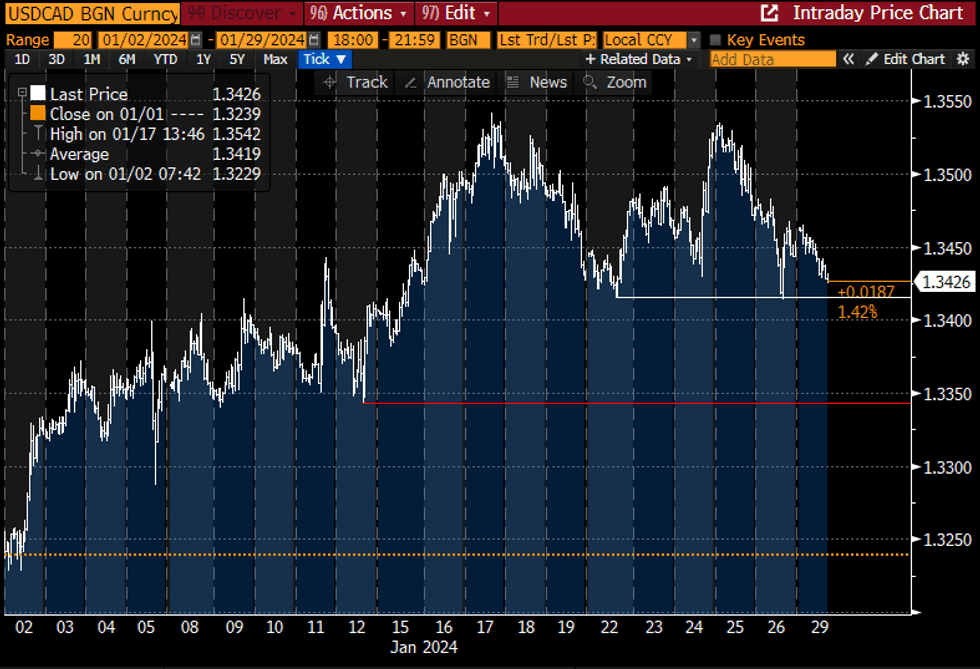

CANADA: USDCAD Tests Bullish Theme With Tilt Towards Initial Support

Jan-29 12:44

- USDCAD has pushed to the day’s low of 1.3426 as the S&P e-mini continues to make intraday gains, but in both cases remaining within Friday’s range.

- Friday’s low of 1.3415 tied with the Jan 22 low, forming initial support after which lies 1.3343 (Jan 12 low) but the technical outlook continues to see the pullback in the pair as corrective with a bull trigger at 1.3542 (Jan 17 high).

- Crude oil futures are off overnight highs but still consolidate Friday’s push higher, helping CAD outperform all majors except for Antipodeans.

- Latest CFTC data showed CAD net shorts were trimmed to -5.4% OI as of Jan 23, moving back close to the -4.3% on Jan 09 which marked the smallest net short position since early August.

Source: Bloomberg

Source: Bloomberg