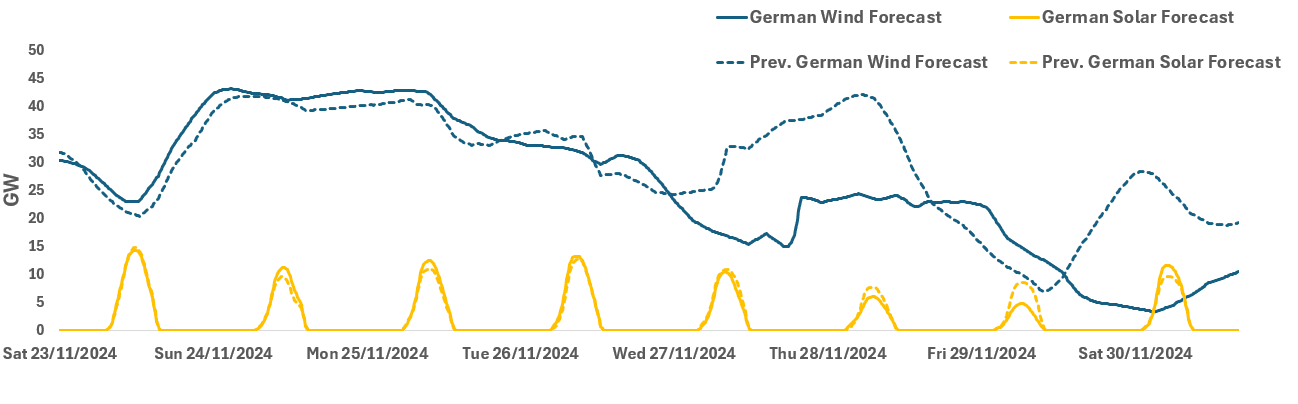

RENEWABLES: German Morning Renewable Forecast

See the latest German renewables forecast for base-load hours for the next seven days from this morning. German wind is expected to be the lowest next week on 27 Nov and 29 Nov – which may raise prices to the highest over the weekday period.

German: Wind for 23-30 November

- 23 November: 29.34GW (+1.36GW),

- 24 November: 42.21GW (+1.12GW),

- 25 November: 40.08GW (+1.75GW),

- 26 November: 31.92GW (-675MW),

- 27 November: 19.01GW (+524MW),

- 28 November: 23.37GW (+357MW),

- 29 November: 15.77GW (unchanged)

- 30 November: 5.83GW

German: Solar for 23-30 November

- 23 November: 2.91GW (-182MW),

- 24 November: 2.08GW (+163MW),

- 25 November: 2.42GW (-162MW),

- 26 November: 2.57GW (-117MW),

- 27 November: 1.97GW (+323MW),

- 28 November: 1.21GW (unchanged),

- 29 November: 0.895GW (unchanged)

30 November: 2.20GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Schatz Upside Rolled Out

DUX4 vs. DUZ4 107.0/107.3/107.7 broken call fly paper lifted the Dec to roll out existing long, paying net 1.25 on 2.5K (13% delta).

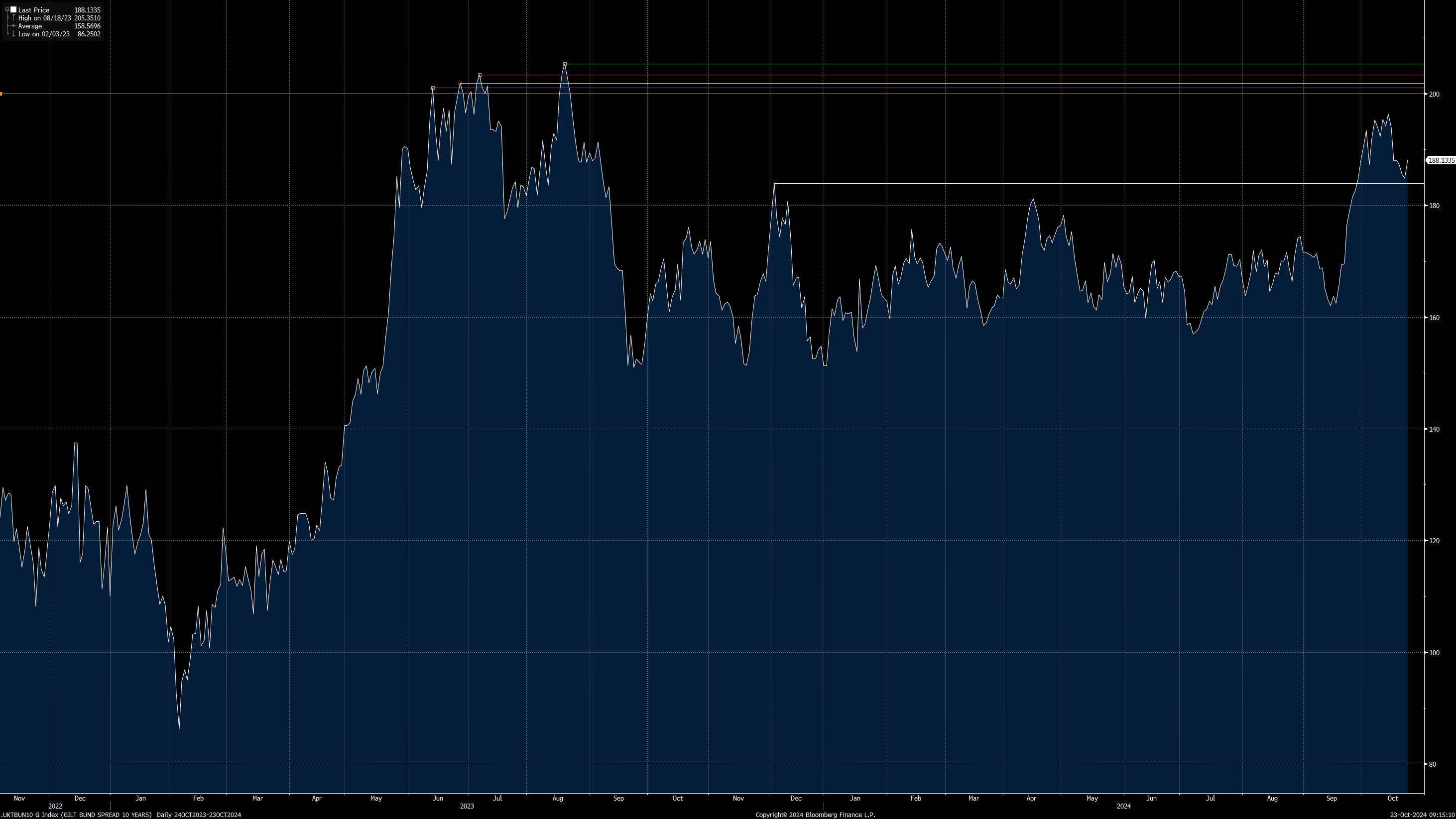

BONDS: Gilt/Bund Spread Reverses Some Of Recent Narrowing

Dovish ECB repricing, linked to the latest round of ECB sources pieces, continues to promote gilt/Bund spread widening this morning.

- Speculation surrounding increased UK government spending on public sector pensions may also be factoring in over the last hour or so.

- 10-Year yield spread back above, 188bp, widening by over 3.5bp on the day.

- Labour’s apparent focus on maximising the fiscal take in the upcoming Budget had allowed the spread to tighten away from cycle closing highs above 196bp in recent sessions.

- Tuesday saw the first close below 185bp since late September.

- Little changed from a technical standpoint in the spread, with old resistance at the Dec ’23 high now initial support.

- To the upside, a break above cycle highs would target 200bp, which protects a cluster of closing highs from summer ’23.

- Looking ahead, the UK Budget (October 30) presents the key near-term risk event for the spread, with a particular focus on the gilt remit. Expect our full preview of the event late this week/early next week.

Fig. 1: 10-Year Gilt/Bund Spread (bp)

EURIBOR OPTIONS: A very busy session in Euribor Options, looking for deeper cuts

- It has been a while since Euribor Option has been this busy for this time of day, interest seems to be back on bigger cut, as some of the latest ECB speakers have not put cold water on potential 50bps cut, sticking to the Data dependency.

Some of the ERZ4 targets levels at the August high and above, looking for 2.75% rates in futures.

- ERX4 97.25/97.12/97.00p fly sold at 4.25 in 10.5k.

- ERZ4 97.37/97.50cs, bought for 1.25 in 10.5k total.

- ERZ4 97.12/97.25/97.37c fly, sold at 1.75 in 4k.

(Chart source: MNI/Bloomberg):