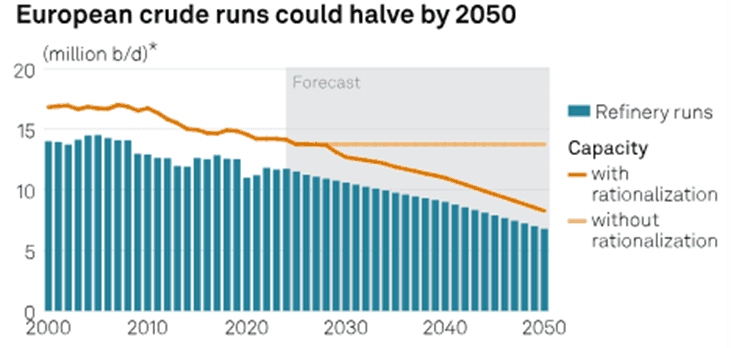

REFINING: Europe Faces Potential Wave of Refining Capacity Closures by 2030

Europe's downstream oil sector could soon see a wave of capacity closures amid the energy transition while margins have trended back toward historical norms, according to S&P Global.

- IEA forecast 1-1.5mb/d of capacity at risk of closure in Europe by 2030 based on expected overcapacity.

- NW Europe's ULSD cracks could fall 36% to $16.27/bbl by 2026, according to S&P Commodity Insights while US Gulf Coast cracks are expected to fall 16% in the same period.

- Refinery utilization rates are forecast to fall from around 84% in 2024 to 81% in 2027.

- Crude processing at Germany’s Wesseling due to end by 2025 and Gelsenkirchen will cut capacity by a third. Italy's Livorno has suspended crude processing with designated for conversion into a biofuel plant and UK's Grangemouth could face closure.

- Overcapacity could drive refiners to consider run cuts, conversions or upgrades to clean fuels as refiners shift from record refining margins to changing demand patterns.

- Europe's gasoil and gasoline demand are set to progressively erode beyond 2025 amid rising electric vehicle uptake.

- Operating costs could also rise due to emissions charges while new facilities such as Nigeria's Dangote and Mexico’s Olmeca add competition.

Source: S&P Global

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA: Sonia put spread trades for more

SFIQ4 94.90/94.75ps 1x2, bought for 2.25 again in 2k, was bought earlier in 5k.

EQUITY TECHS: E-MINI S&P TECHS: (U4) Bull Cycle Extends

- RES 4: 5622.69 2.764 proj of the Apr 19 - 29 - May 2 price swing

- RES 3: 5600.00 Round number resistance

- RES 2: 5594.66 2.618 proj of the Apr 19 - 29 - May 2 price swing

- RES 1: 5572.00 2.50 proj of the Apr 19 - 29 - May 2 price swing

- PRICE: 5565.50 @ 14:24 BST Jun 19

- SUP 1: 5433.13/5345.64 20- and 50-day EMA values

- SUP 2: 5267.75 Low May 31 and key support

- SUP 3: 5213.25 Low May 6

- SUP 4: 5155.75 Low May 3

The uptrend in S&P E-Minis remains intact and the contract has traded higher this week, confirming an extension of the current bull cycle. Price has recently cleared 5430.75, the May 23 high and bull trigger. This confirmed a resumption of the uptrend. Note that MA studies are in a bull-mode position too, highlighting positive market sentiment. Sights are on 5572.00 next, a Fibonacci projection. Initial support lies at 5433.13, the 20-day EMA.

US TSYS: Recent Yield Ranges Set To Remain Intact, Higher For Longer Embedded For Now

While cash Tsys are closed for the US holiday, the modest downtick in futures is set to leave the multi-week ranges in yields intact at the Asia cash open.

- Ultimately, the recent mix of Fedspeak, updated dot plot and general direction of travel for data has embedded the higher-for-longer rates mantra, albeit with some contained bouts of volatility around recent tier 1 data releases.

- May’s PCE data (Jun 28) provides the next meaningful inflation input, with CPI & PPI already biasing sell-side estimates lower.

- The early BBG survey medians point to +2.6% Y/Y for both headline PCE (vs. +2.7% prior) and core PCE (vs. +2.8% prior). While this is still above the Fed’s inflation target, Chair Powell previously noted that “if you're at 2.6-2.7%, that's a really good place to be.” This suggests that a run of inflation releases around those sort of levels could give the Fed greater confidence to actively consider reducing rates.

Fig. 1: U.S. 10-Year Tsy Yield (%)