US DATA: Record Trade Deficit Driven By Metals Pre-Empting Tariffs

Mar-06 17:55

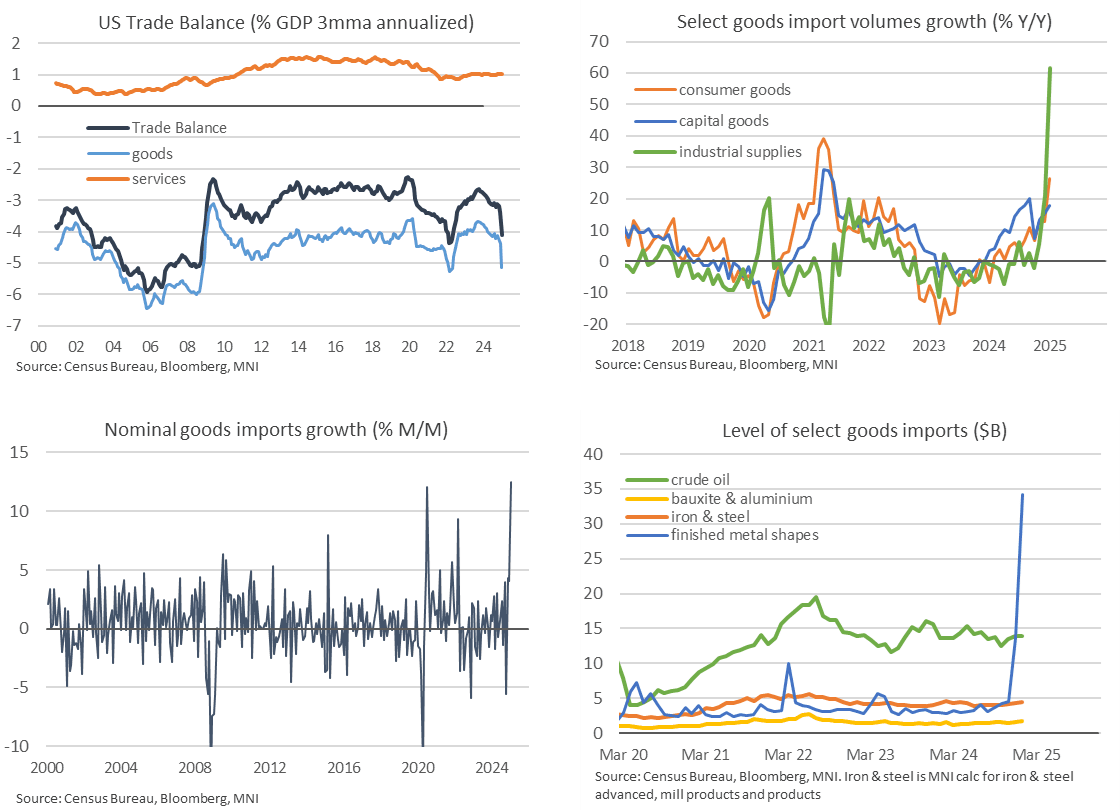

January's goods and services trade deficit was even wider than estimated at $131.4B ($2.6B bigger than consensus of $128.8B which had ballooned after the surging goods deficit), representing a material jump from December's $98.1B (downwardly revised from $98.4bln) and by far the largest monthly print in history.

- Whilst it’s a nominal measure and so historical comparisons should be taken with caution, the deficit compares with the previous record of $101.9bn from Mar 2022.

- The goods & services deficit widened to 4.1% of GDP on a three-month annualized basis vs 3.1% of GDP in the three months to October (pre US election result).

- The larger deficit was driven by a +10.0% M/M jump in goods & services imports (second highest on record) - following mid-3% sequential increases seen in both Nov/Dec. Unsurprisingly, goods imports were the standout at +12.3% M/M (+4.2% Nov/Dec), while services imports printed a much more regular +0.6% M/M (+1.6% Dec).

- Exports meanwhile increased just +1.2% M/M after seeing no clear trend in recent months (-2.6% Dec). Developments were positive across goods (+1.6% M/M) and services (+0.6% M/M).

- In real terms, industrial supplies did indeed lead the surge in imports as the advance nominal details had indicated. They jumped 32% M/M for 62% Y/Y, with consumer goods 26% Y/Y and capital goods 18% Y/Y.

- In today's nominal details, this jump in industrial supplies comes from "finished metal shapes" in signs of clear tariff front-running. At $34.3bln, they're around around a 10x increase to its 2023 monthly average. There are yet signs of notable front-running in other key supplies, which possibly still be seen in February.

- Yesterday's postponement of US tariffs on cars and car parts imported from Canada and Mexico meeting some compliance criteria (followed up by a related announcement just now) suggests that imports on these goods might not plummet as much as otherwise expected imminently - however, inventories on affected products are potentially already well built up by now, meaning that current import levels are well above a sustainable level.

- Also from a consumption perspective, the recent deterioration in sentiment across a set of soft data in the US, with generally lower prints in the 'new orders' category, at least has the potential to also filter through lower imports at some stage.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

POLITICAL RISK: US Federal Layoffs Likely If Not Enough Quitters - WaPo

Feb-04 17:55

- The Washington Post (in full here) writes that federal government layoffs are likely if too few choose to quit.

- “Workers have until Thursday to decide whether to take an offer to resign now and be paid through the end of September.”

- A reminder that public sector payrolls growth has been providing an outsized impact on total nonfarm payrolls growth for some time, although that has been coming from the much larger state and especially local government sectors. There are around 3.0m federal employees, 5.5m state and almost 15m local.

- As such, whilst overall government job creation averaged a monthly 32k in Q4 for close to double the 18k averaged in 2019 and treble the 9k averaged through 2017-18, federal-specific job creation has averaged 3k in Q4 for no discernible change from the 2k in 2019.

- Quit rates are much lower in the public sector than the private sector, at 0.8% as of today's report for Dec (and just 0.4% specifically for federal workers) compared to 2.2% for private, suggesting layoffs could be likely.

PIPELINE: Corporate Bond Issuance Update: Foundry JV Guidance Update

Feb-04 17:54

$14.8B corporate issuance has launched so far, to expand once Foundry JV 5pt launch

- Date $MM Issuer (Priced *, Launch #)

- 02/04 $3B *EIB WNG 10Y +60

- 02/04 $2.5B #NextEra Capital Energy $1.5B 30.5NC5.25 6.375%, $1B 30.5NC10.25 6.5%

- 02/04 $2B *L-Bank $1B 2Y SOF+30, $1B 5Y SOFR+47

- 02/04 $1.5B #BNG Bank 3Y SOFR+37

- 02/04 $1.25B #BNY Mellon 6NC5 +62

- 02/04 $1.1B #National Rural Utilities $600M 3Y +52, $500M 5Y +67

- 02/04 $1B #Altria $500M 3Y +67, $500M 10Y +117

- 02/04 $1B #National Fuel Gas $00M 5Y +118, $500M 10Y +147

- 02/04 $800M #GATX $500M 10Y +102, $300M 2054 Tap +113

- 02/04 $650M #Valero Energy 5Y +87

- 02/04 $Benchmark Foundry JV 6Y +120, 8Y +150, 11Y +160, 12Y +170, 14Y +180

- Expected to issue Wednesday:

- 02/05 $1B KFW 4% 2026 TAP SOFR+20

- 02/05 $Benchmark IDA 10Y SOFR+63a

OPTIONS: More Limited Rates Trade After Prior Week's Flurry

Feb-04 17:52

Tuesday's Europe rates/bond options flow included:

- OEH5 118.25c, sold at 15.5 down to 14.5 in 14k

- ERM5 97.50 put, paper pays 1.25 on 16k

- SFIK5 95.75/95.90/96.05/96.20 call condor bought for 7-7.25 in 10k

- SFIM5 95.85/95.65ps 1x2 with SFIU5 96.00/95.70ps 1x2, bought the strip for 5.25 in 2.5k.