CHILE: Record Copper Prices Propel CLP to Cycle High, Boric Meets With Kast

- The rally in copper to record highs this week, amid supply concerns, has provided continued support to the Chilean peso, which is trading around cycle highs. Despite a slight pullback in copper today, USDCLP has edged lower in early trade, keeping the pair just above this week’s low of 879.75.

- As noted, the trend condition for the pair remains bearish, with sights on 878.22 and 865.80, the 1.236 and 1.382 projections of the Apr 9 - Jul 2 - Jul 30 2025 price swing. On the upside, initial resistance is at 898.81, the 20-day EMA. Short-term gains would be considered corrective.

- With copper at record highs, the robust outlook for the mining sector should remain supportive for the peso’s medium-term outlook. Chile’s mining industry group Sonami has said this week that mining output could rise by 10% to 20% over the next two years, and yesterday Codelco said that it had secured approval for a $2.8bn project to expand and extend its Ministro Hales mine.

- Today, President Boric is due to meet with President-elect Kast at a ceremonial event.

- No macro date are due, with the calendar clear until the next BCCh traders survey on Jan 22, followed by December PPI stats Jan 23. These come just ahead of the Jan 27 BCCh MPC meeting, where the central bank is widely expected to remain on hold at 4.50%, before delivering a final cut to neutral later this quarter.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Dec16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1750-55(E1.8bln)

- USD/JPY: Y156.00($1.1bln)

- GBP/USD: $1.3500(Gbp3.8bln)

- NZD/USD: $0.5845-50(N$540mln)

- USD/CAD: C$1.3750($885mln)

ECB: Balance Sheet Suggests Little Need For Liquidity Action in Eurozone

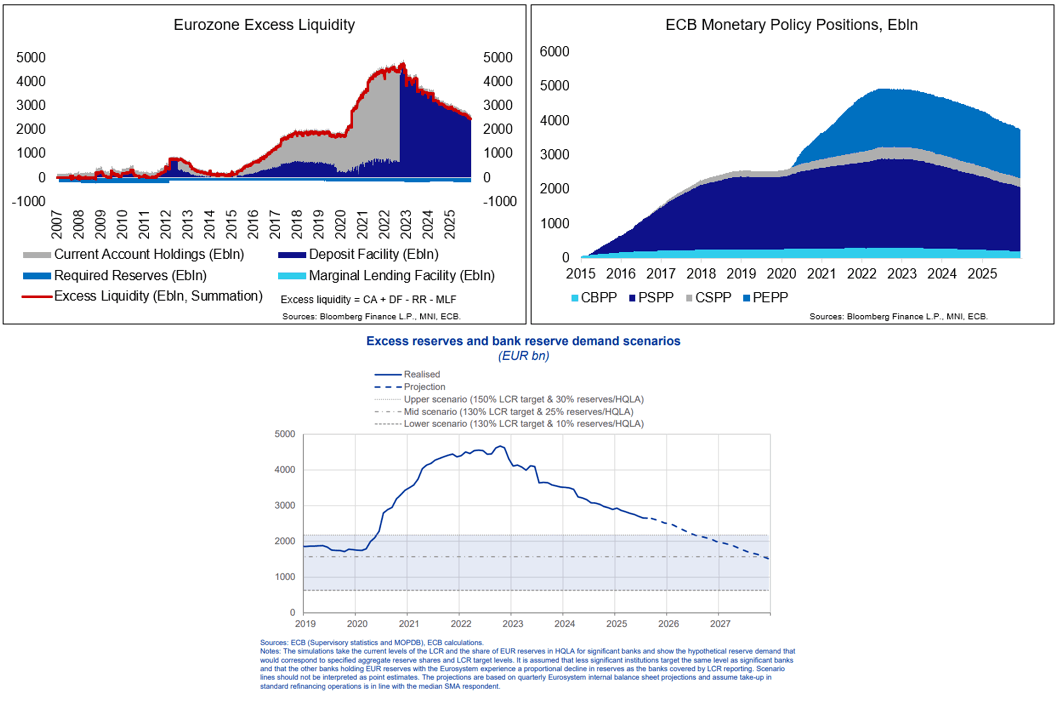

ECB balance sheet data ahead of Thursday's meeting confirms that excess reserves remain well above levels approaching scarcity across the Eurozone, leaving little pressure on the ECB to act on the structural bond portfolio for now.

- This is contrary to the Fed & BoE which both have provided fresh liquidity support/increased focus on bank liquidity provisions in recent months, after bank reserves in their respective jurisdictions moved towards / reached a less abundant state. Latest ECB projections see excess reserves hitting bank demand in mid-2026 in an "upper scenario" but not until late 2027 in a "mid scenario".

- Passive run-off of the ECB balance sheet can be bumpy in the short term but a longer-term downtrend remains intact. This led Eurozone excess liquidity to decrease by roughly €32bln/month YTD 2025, bringing the measure to around €2.465trl, down by 48% from the series' high of €4.748trl in November 2022.

- When liquidity ultimately becomes "scarce" (or close to it) that will show in money market tensions and increased takeup in the ECB's standard refinancing operations, neither of which are apparent at this stage.

The long-term liquidity decline since the peak was initially been driven by a roll-off of the ECB's TLTROs (with the TLTRO III programme starting in 2019 with three-year maturities and with the final maturity in Dec 2024) but mostly comes on the back of the declining ECB's monetary policy positions (PEPP + APP), which are standing at a current €3.753trl combined. Amongst the policy positions, the ECB envisages a further average monthly roll-off of around €13.4bln of the PEPP through Dec-26 and of around €28.6bln of the APP through Jul-26 (respective f'cast horizons).

- Latest ECBspeak on the balance sheet came from Schnabel in a speech titled "Towards a new Eurosystem balance sheet" (speech here, later slides here. Mirroring the above, Schnabel highlighted:

- "Quantitative normalisation is proceeding smoothly, with strong liquidity positions of banks and abundant excess liquidity"

- "Operational framework suggests a sequence for how to supply reserves in the future, with a persistent take-up of standard refinancing operations to precede the launch of structural operations, starting with longer-term refinancing operations and followed by a structural securities portfolio"

- "Considerations about stance neutrality, policy space and financial soundness suggest tilting the new structural securities portfolio towards shorter-term securities"

US TSYS: A Bearish Outlook For TY Awaiting NFPs and Retail Sales

Treasuries have pared small further gains overnight over the past two hours as US desks start to filter in. Cumulative overnight volumes have been very thin ahead of an important docket that sees the November payrolls report and October retail sales as well as flash PMIs for December and the latest weekly ADP update to main a few other releases.

- Cash yields are 0-0.5bp higher on the day.

- 5s30s earlier hit 113.4bp for a fresh three-month high, currently at 112.4bp.

- TYH6 trades at 112-10 (+01) on very thin volumes of 190k, holding within yesterday’s range.

- The technical set-up points to a bearish outlook with support at the bear trigger of 111-29 (Dec 10 low) before 111-19 (Fibo projection). Resistance meanwhile is seen at 112-20 (20-day EMA) before 112-23 (Dec 11 high).

- Data: Weekly ADP (0815ET), NFP Nov (0830ET), Retail sales Oct (0830ET), NY Fed services (0830ET), Weekly Redbook retail sales (0855ET), S&P Global PMIs Dec prelim (0945ET), Business inventories Sep (1000ET)

- Bill issuance: US Tsy $75B 6W Bill auction (1130ET)

- Politics: Trump in ambassador credentialing ceremony (1400ET, closed press), Trump participates in Hanukkah reception (2015ET)