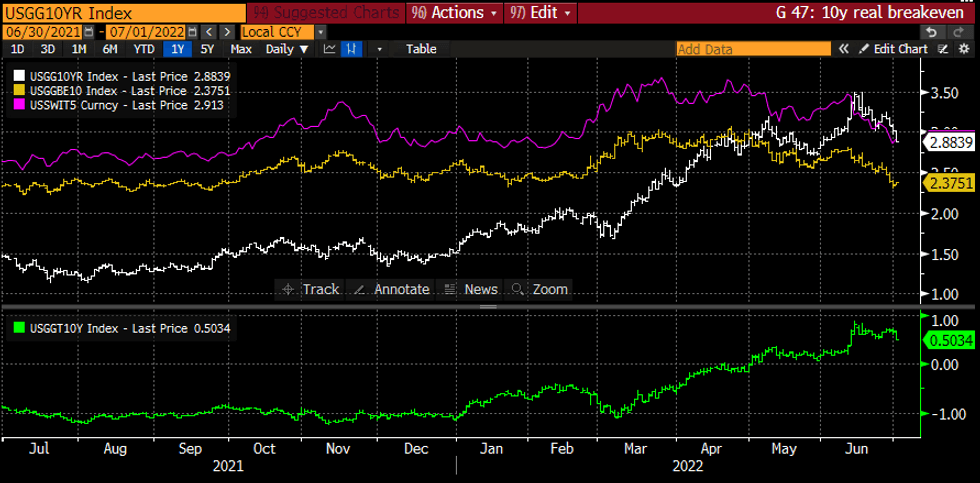

US TSYS: Real Yields Tumble On Growth Concerns

Jul-01 13:30

- Growth concerns are particularly evident in real yields today, with 10Y real yields sliding 15bps to +51bps although still some 25bps higher than prior to the US CPI surprise on Jun 10 that helped push the FOMC to a 75bp hike.

- With nominal yields sliding 12bps, the inflation breakeven has nudged 3bps higher but this counts as a stabilisation after sliding over the past month to pre-taper levels at 2.38%.

- Focus will be on upcoming mfg surveys, with the final US PMI (Eurozone largely unrevised this morning) and then more importantly ISM at 1000ET. Regional Fed surveys and yesterday’s miss in the MNI Chicago PMI both implying downside risk to ISM consensus for a fall from 56.1 to 54.5.

US 10y real yields (green), nominal yields (white) and breakeven (yellow), plus 5Y inflation swap (pink). Source: Bloomberg

US 10y real yields (green), nominal yields (white) and breakeven (yellow), plus 5Y inflation swap (pink). Source: Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: USDCAD at new session low

Jun-01 13:29

- USDCAD is heading towards the 1.2600 figure now at 1.2616, on elevated Oil and Risk back towards the upper end of the range, heading into the Equity cash open.

- Attention quickly turns to the BoC rate at the top of the hour, when a 50bps HIKE to 1.50% will be expected.

PIPELINE: June Issuance Starts Off With a Bang

Jun-01 13:28

John Deere, More Banks Join Issuer List

- Date $MM Issuer (Priced *, Launch #)

- 06/01 $1.8B Tenet Healthcare 8NC3

- 06/01 $1B #Province of Saskatchewan 5Y SOFR+55

- 06/01 $500M Baltimore Gas&Electric WNG 30Y +180a

- 06/01 $Benchmark John Deere 3Y +80a, 3Y SOFR, 10Y +130a

- 06/01 $Benchmark TD Bank 3Y +115a, 3Y SOFR, 5Y +140a, 5Y SOFR, 10Y +180a

- 06/01 $Benchmark Truist Financial 6NC5 +140a

- 06/01 $Benchmark SEB 3Y +110a, 3Y SOFR

- 06/01 $Benchmark NY Life 2Y +75a, 2Y SOFR

- 06/01 $Benchmark Liberty Mutual 30Y +260a

- 06/01 $Benchmark PNC Financial 11NC10 +200a

- 06/01 $Benchmark Handelsbanken 3Y, 3Y SOFR, 5Y

- 06/01 $Benchmark Royal Bank pf Canada 3Y SOFR+65a

FRANCE: Macron-Led Alliance Retakes Lead In Latest Legislative Election Poll

Jun-01 13:21

The latest opinion poll from Ifop ahead of the 12/19 June legislative election shows President Emmanuel Macron's centrist Ensemble! alliance retaking the lead from the leftist NUPES alliance.

- Ensemble: 27 % (+1), NUPES: 25 % (-2), Rassembelement National (RN): 21 % (-2), Les Republicains and allies: 10 % (-1), Reconquest: 6 %, Miscellaneous left: 4 %.IFOP, 28/05/22. Chgs w/13-16 May,

- Seat Projection: Ensemble: 275-310, NUPES: 170-205, LR & allies: 35-55, RN: 20-50, Reconquest: 1-4, Others: 8-15. IFOP, 28/05/22.

- A total of 289 seats are required to command a majority in the National Assembly. This means that should Macron's bloc's seat total fall at the bottom end of their projection estimate it would be short of a majority and reliant on support from other parties.

- The likelihood remains that the next gov't will be led by Ensemble, with the leftist NUPES (comprising Jean-Luc Melenchon's La France Insoumise, and the Communist, Green, and Socialist parties) unlikely to be able to pull together enough support from other representatives (who are all likely to come from the centre-right or right) to overtake Ensemble.