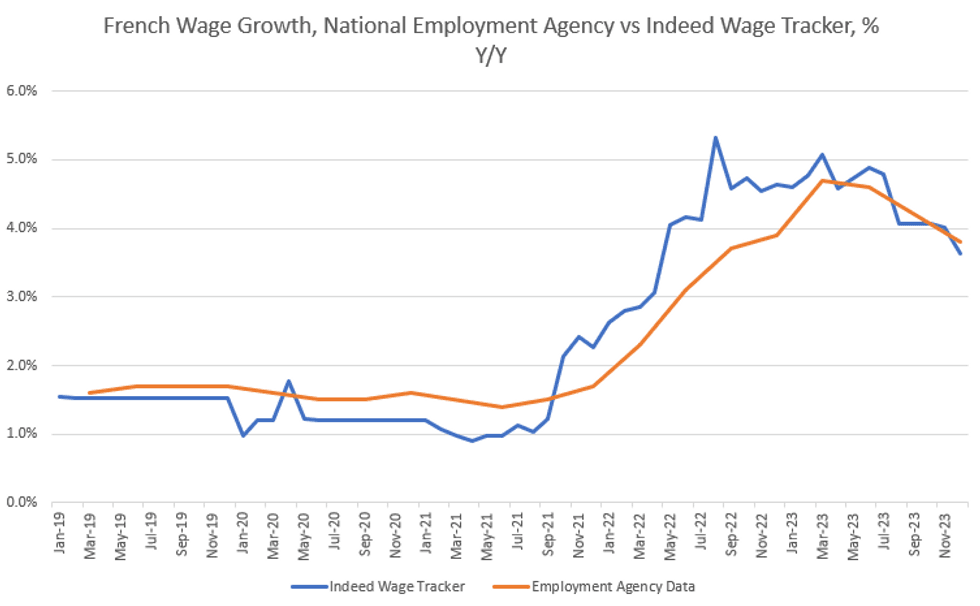

FRANCE DATA: Real Wages Rise For First Time In Cycle In Q4

French nominal wages increased in Q4 2023 by +0.3% Q/Q (vs +0.5% prior) and +3.8% Y/Y (vs +4.2% prior). This was the fourth consecutive slowdown in the Y/Y rate, but nonetheless marks the first time in the current cycle that the yearly wage growth rate exceeded the average CPI inflation rate (3.7% Y/Y) of the respective quarter.

- Looking at the individual sectors, wage growth developments were fairly uniform, with industrial wages excl. construction and services wages rising +0.3% Q/Q (vs +0.5% prior, both), and construction wages at +0.2% Q/Q (vs +0.4% prior).

- The official Q4 growth rate largely mirrors the monthly data from the Indeed.com wage tracker, which printed at +3.6% Y/Y (+4.0% prior) in December 2023.

- Wage growth in France has been softer than in some Eurozone peers since the beginning of 2023, which has allowed French unit labour costs to remain relatively in-line with others despite poor productivity.

- That intersection between wage growth and productivity will be a key to unlocking ECB rate cuts, as stressed again by ECB's Lane and Schnabel in recent interviews and panel discussions.

- Additionally the nascent pickup in French real wage growth will be eyed as a constructive macro factor, with ECB President Lagarde noting in January's press conference: "one of the reasons why we see [Euro area] growth coming up and the recovery beginning in the course of 2024; because of rising wages while inflation comes down, which will free up some purchasing power, which hopefully will stimulate consumption."

MNI, Indeed.com, Ministry of Labour

MNI, Indeed.com, Ministry of Labour

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Spain 10-year: Spread set

- Size: EUR Benchmark (MNI expects E10-13bln)

- Book in excess of E130bln (inc E6.25bln JLM interest)

- Spread set at: 3.55% Oct-33 Obli (mid) + 9bps (Guidance was + 11bps area)

- Maturity: 30-April-2034

- Settlement: 17-Jan-2024 (T+5)

- Coupon: Fixed, annual ACT/ACT, short first to 30-April-2024

- ISIN: ES0000012M85

- Bookrunners: Barclays, BBVA, CACIB, DB, JPM, SANTANDER (B&D/DM)

- Timing: Books to close at 10:15GMT / 11:15CET

BTP: Tighter Vs. Bunds With Syndication Pressure In Rear-View

The very tail end of ’23 and first few days of ’24 saw BTPs under some pressure on issuance worry and markets paring ECB policy rate path pricing back from dovish extremes, amid a broader unwind of part of the late ’23 bond rally.

- Still, the move was relatively contained with the 10-Year BTP/Bund spread finishing last week just below 170bp.

- Take up/demand at yesterday’s dual BTP syndication (demand of ~EUR165bn against EUR15bn of issuance) and the passage of related hedging flow has allowed the spread to re-tighten, trading back at ~162bp last, moving back toward last year’s tights (~156bp in closing terms).

Fig. 1: 10-Year BTP/Bund Spread (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

SLOVAKIA: Pellegrini Reaffirms Intention To Run In March 23 Presidential Election

Slovak National Council Speaker Peter Pellegrini on Tuesday confirmed the date for this year's presidential election, with the first round scheduled for March 23 and a potential second round pencilled in for April 6. Pellegrini also reaffirmed his intention to run and said that, barring unexpected developments, he will formally launch his campaign in his home town of Banska Bystrica on January 19.

- Incumbent liberal President Zuzana Caputova had earlier noted that she would not seek another five-year term in office due to the stress caused by several national and international crises which hit Slovakia in the recent years.

- Pellegrini assumed the top job in parliament as part of his post-election power-sharing deal with Prime Minister Robert Fico, who is expected to back his presidential bid and refrain from fielding a rival candidate.

- Early opinion polls suggest that if the election was held today, Pellegrini would likely advance to the run-off with ex-Foreign Minister Ivan Korcok and would be a clear favourite in the second round.

- The powers of the Slovak President are limited, but there are certain areas where they can exercise discretion, such as some appointments of senior public officials and granting pardon or parole.

- Despite its largely ceremonial role, claiming the presidency would allow the current ruling coalition to consolidate its influence on Slovak politics and face less resistance to its domestic and international policy plans.