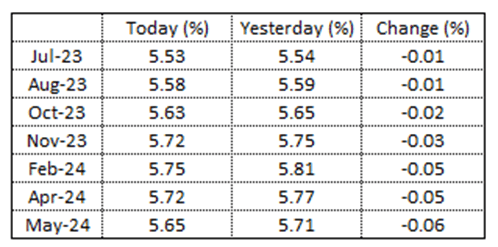

STIR: RBNZ Dated OIS Prices A No-Change Outcome Tomorrow

Today RBNZ dated OIS pricing is 1-6bp softer across meetings beyond July ahead of the RBNZ policy decision meeting tomorrow. See the MNI RBNZ Preview here.

- Bloomberg’s consensus is unanimous in expecting a no-change outcome after the RBNZ steered the market in its May Monetary Policy Statement that it expected that no further increases in the OCR would be required and that now is the time to “watch, worry and wait”.

- A 12% chance of a 25bp hike is priced for tomorrow’s policy meeting.

- However, it is important to note that terminal OCR expectations have shifted 10bp firmer since last week and currently sit at 5.75%.

Figure 1: RBNZ Dated OIS: Today Vs. Yesterday

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Key Support Zone Remains Exposed

- RES 4: 1.3730 76.4% retracement of the Mar 10 - Apr 14 low

- RES 3: 1.3695 High Mar 28

- RES 2: 1.3668 High Apr 28 and key resistance

- RES 1: 1.3479/85 20-day EMA / High Jun 1

- PRICE: 1.3327 @ 16:29 BST Jun 9

- SUP 1: 1.3313 Low Jun 09

- SUP 2: 1.3302 Low Apr 14 and a key near-term support

- SUP 3: 1.3275 Low Feb 14

- SUP 4: 1.3214 2.0% 10-dma envelope

USDCAD maintains a softer tone and traded to new multi-month lows Friday. The resumption of weakness exposes 1.3302, the Apr 14 lows and a key support. Clearance of this level would strengthen bearish conditions. On the upside, initial firm resistance is at 1.3479, the 20-day EMA. A break of this level is required to ease bearish pressure.

AUDUSD TECHS: Bullish Friday Close

- RES 4: 0.6818 High May 10 and key resistance

- RES 3: 0.6789 3.0% 10-dma envelope

- RES 2: 0.6755 2.0% Upper Bollinger Band

- RES 1: 0.6751 High Jun 9

- PRICE: 0.6744 @ 16:27 BST Jun 9

- SUP 1: 0.6623 20-day EMA

- SUP 2: 0.6567/6458 Low May 31 and the bear trigger

- SUP 3: 0.6403 76.4% of the Oct - Feb bull cycle

- SUP 4: 0.6387 Low Nov 10 2022

The AUDUSD bull cycle that started on May 31 remains in play and the pair is trading at its recent highs. Resistance at the 50-day EMA has been cleared. The break higher strengthened on the break of 0.6733, 76.4% of the downleg in May. On the downside, a reversal lower is required to refocus attention on 0.6458, the May 31 low. Initial support is seen at 0.6623, the 20-day EMA.

US TSYS: Fading Canada Jobs Move, Tsys Weaker Ahead Next Wks FOMC, ECB, Boj Annc

- Treasury futures holding modestly weaker levels after the bell, near the middle of a decent session range. On what would have been a quiet Friday session ahead next week's FOMC (Wed), ECB (Thu) and BOJ (Fri) policy announcements, futures gapped off weaker levels following a drop in Canada employment data (-17.3k vs. +25k exp).

- Treasuries scaled back from post-Canada employment data induced highs, levels are back near opening levels with front month 10Y futures at 113-13 (-10.5). Curves extend inversion (2s10s -5.543 at -85.851) as short end rates underperformed ahead next week's bill and coupon supply (large 2s/30Y ultra flattener also note: -13,328 TUU3 102-13.75, through 102-14.12 post-time bid vs. +2,364 WNU3 135-12.

- Fed Funds implied rates are drawing to the end of the week with yesterday’s initial claims spike still weighing on pricing for next week’s FOMC but meetings later on in the year having clawed back the drop.

- The further trimming of cuts sees just 24bp from July’s terminal to year-end and 38bp from July to Jan for the smallest since Mar 09 as rate cut expectations began to surge on regional banking woes.

- Cumulative changes from current 5.08% effective: +7bp Jun (+0.5bp on the day), +20bp Jul (+0.5bp), +18.5bp Sep (+1.5bp), +9bp Nov (+2.5bp), -4bp Dec (+3.5bp) and -18bp Jan (+5bp).