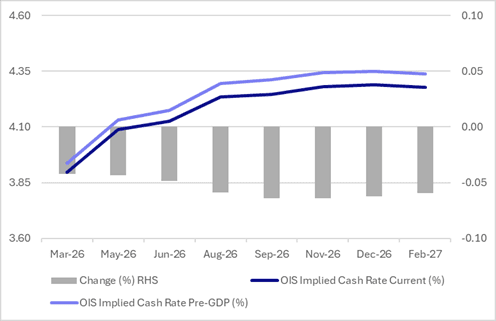

STIR: RBA-Dated OIS Pricing Softens After Q4 GDP

RBA-dated OIS pricing is 4-7bps softer across meetings after today’s Q4 GDP print.

- Australia's economy was growing at 2.6% y/y in the December quarter, up from 2.1% in the previous quarter.

- The economy grew by 0.8% q/q in Q4, which was stronger than the 0.5% recorded in Q3.

- However, the market appears to have focused on soft household spending in the 4Q GDP data which came in below the RBA’s February forecasts.

- (Bloomberg) “Given there has been a focus on that in the RBA communications, I think paring back some of the pricing of a third hike this year is reasonable.” says Kenneth Crompton, head of rates strategy in Sydney

- RBA-dated OIS pricing still shows tightening across all meetings, with the probability of a 25bp hike rising from 17% for March (35% pre-data) to 110% by June (129% pre-data) and 175% by December 2026 (200% pre-data).

Figure 1: RBA-Dated OIS - Current Vs. Pre-GDP

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Metal Vol Continues, Around Weaker Bias, USD Only Modestly Higher

Cross asset market focus remains on the metal space, with early sharp losses for both gold and silver in Monday trade. Volatility remains very elevated. So far today silver has had a $75.10 to $87.95 range, we were last near $82, down around 4% versus end Friday levels. Earlier lows weren't sub Friday lows just under $74. For gold, we were last around $4700, with a range of $4586.44 to $4894.23. Earlier lows did breach the Friday low (which was just under $4700). Oil is weaker as well, down over 3%, WTI last near $63, which is a level that prevailed mid last week.

- Bitcoin is firmer, back above 77k, with dips under 76k supported so far, but Bitcoin did weaken notably over the weekend (ending last Friday around 84.1k.

- The USD is higher so far today, but comfortably off best levels (BBDXY highs of 1190.03, last 1189.15/20). AUD and NZD are little changed, while USD/JPY is firmer, above 155.00. This is at odds with the softer US equity futures backdrop, currently off 0.30-0.50% for Eminis/Nasdaq futures.

- However, weekend comments from Japan PM Takaichi around some of the benefits of a weaker yen (which were tempered somewhat), may still be impacting. Spot USD/KRW is also higher, pushing back towards 1460 (down a further 1.2% in won terms).

- US Tsy futures are down a touch, while that is also the tone for regional bond futures.

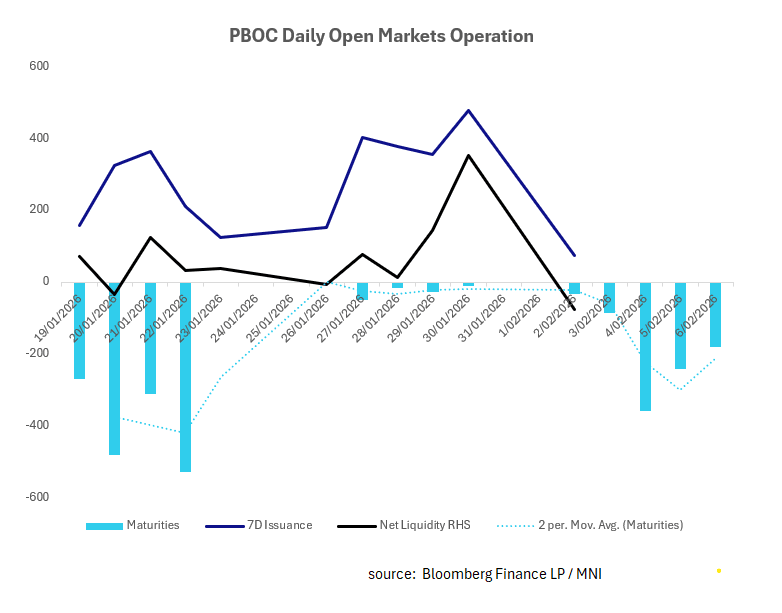

CHINA: Central Bank Withdraws CNY75.5bn via OMO

After large injections Thursday and Friday last week, it is not surprising to see a modest withdrawal today, especially given some stabilization in repo rates. Repo rates however remain stubbornly higher than near term lows and with market volatility expected to rise and a reasonable maturity schedule this week, a return to injections seems logical.

- The PBOC issued CNY75bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY150.5bn.

- Net liquidity withdrawal CNY75.5bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.44%, from prior close of 1.59%.

- The China overnight interbank repo rate is at 1.36%, from the prior close of 1.32%.

- The China 7-day interbank repo rate is at 1.50%, from the prior close of 1.59%. .

CNH: USD/CNY Fixing Edges Up, But Error Term back To Negative

The USD/CNY fix printed at 6.9695, versus the 6.9718 market estimate. The error term was -23pips, versus +226pips from Friday. This is the first negative fixing error since late Nov last year. The fixing was set higher than Friday's outcome (6.9678) but only marginally. Looking at the longer term trend of the fixing outcome, little has changed despite the recent USD bounce. The weekend onshore media highlighted the push for CNY to become a global reserve currency. This, along with today's fixing result, is likely to reaffirm the relative stability of the yuan during a potential USD bounce. USD/CNH is down slightly so far today, last 6.9555, outperforming the 0.10-0.15% rise in the BBDXY.