EM LATAM CREDIT: Raizen: 2Q 2025 Earnings - Negative

(RAIZBZ; Baa3/BBBneg/BBB)

Another disappointing earnings report for the Brazil sugarcane and ethanol processor with adjusted EBITDA declining 23% while net debt rose 56% YOY resulting in a reported net debt/adjusted EBITDA LTM of 4.5x, up from 3.2x last quarter and up from 2.3x a year ago. We would not be surprised to see further negative rating actions as a result.

Raizen ethanol processing results were weaker with EBITDA dropping 23.7% YoY and Argentina fuel distribution lower by 50.6% while Brazil fuel distribution managed a small 3.3% gain.

The company replaced short term working capital lines like supplier agreements and customer advances with longer term debt which improved balance sheet liquidity but at a cost of raising debt leverage which the company estimated at .8x.

Some divestitures were announced during the quarter and the company projected BRL2.6bn of proceeds by the end of the crop year for previously announced asset disposals.

Further asset sales were planned with local news reports about a week ago suggesting a USD1.5bn price tag for Argentina assets with Trafigura being a potential buyer. The company also mentioned a potential capital increase from its shareholders, though it qualified that initiative as in the early stages.

RAIZBZ 35s were last quoted T+229bp, 7bp tighter QTD and 18bp wider YTD.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

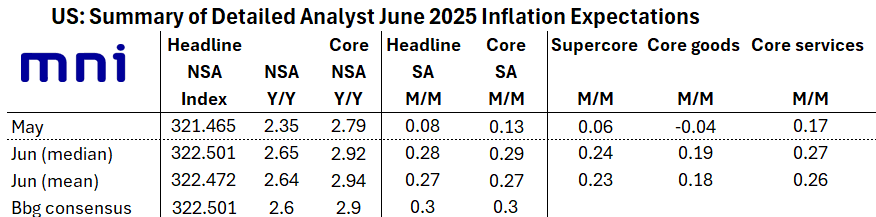

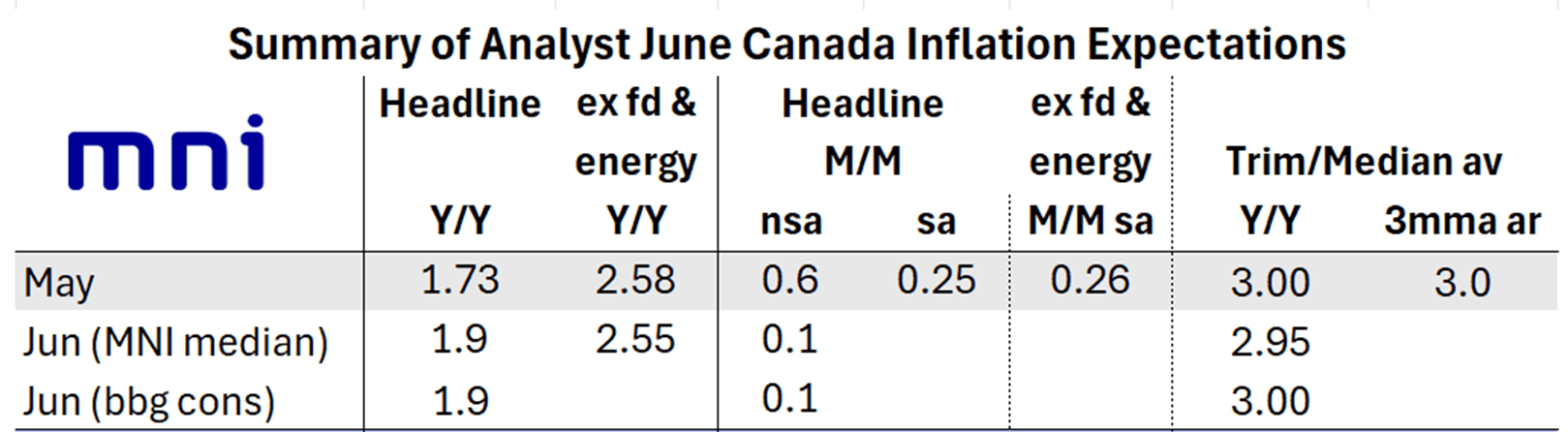

INFLATION: US And Canada Y/Y CPI Expected To Pick Up In June

It's North American inflation day, with the US and Canada reporting CPI at 0830ET:

In the US, consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June on a rounded basis, but with sizeable risk of undershooting at 0.2% (MNI median unrounded estimate at 0.24% M/M /average 0.25%). This would mark an acceleration from 0.13% M/M in May, with core services ticking up and core goods

more than reversing May’s unexpected M/M deflation. Y/Y core is seen up to 2.9% from 2.8%.

- Headline CPI meanwhile is seen at 0.3% M/M or 0.25% M/M unrounded after 0.08% in May, amid a bounce in gasoline-driven energy prices, with Y/Y up to 2.6-2.7% from 2.35% prior.

- Consensus table below - our full US preview is here, including category-by-category details.

In Canada, Headline CPI is seen rising to 1.9% Y/Y in June, up from 1.73% (unrounded) in May, which would mark a 3-month high. On a M/M non-seasonally adjusted basis, CPI is seen pulling back to 0.1% from 0.6% (0.55% unrounded) prior. MNI's summary of analyst consensus is below.

- More importantly from the Bank of Canada's perspective, the average of trim/median inflation is seen basically steady, at 2.95% (MNI median, 3.00% BBG consensus), vs 3.00% in May. More specifically, Median is seen coming in at 2.9% with Trim at 3.0%. Even a soft reading is unlikely to convince the BOC to cut on July 30, though.

US: MNI POLITICAL RISK - Trump Continues Hawkish Pivot On Russia

Download Full Report Here

- President Donald Trump is eyeing investment deals at today's inaugural Pennsylvania Energy and Innovation Event.

- Former NSA Mike Waltz's appearance before the Senate Foreign Relations Committee today offers Democrats a rare chance to grill a Trump administration insider.

- House Ways and Means Republicans will meet USTR Jamieson Greer this morning and Commerce Secretary Howard Lutnick on Wednesday for trade negotiation updates.

- The EU has finalised a list of countermeasures targeting goods worth around USD$85 billion, but will refrain from retaliation while negotiations are ongoing.

- Treasury Secretary Scott Bessent said he expects to meet his Chinese counterpart in the coming weeks.

- Japanese officials say Tokyo has no plans for tariff retaliation.

- Senate Majority Leader John Thune (R-SD) could delay a first procedural vote on Trump’s USD$9.4 billion rescissions package.

- White House NEC Director Kevin Hassett, a close Trump ally, is firming as favourite to become the next Fed Chair.

- Trump increased pressure on Russia, announcing plans to send defensive and offensive weapons to Ukraine via NATO partners and issuing Russian President Vladimir Putin a 50-day ultimatum to reach a peace deal with Ukraine, or be hit by “very severe tariffs”. Thune said he would hold off on advancing a bipartisan Russia sanctions bill, in light of Trump's statement.

- Poll of the Day: Trump’s approval ratings ticked back up despite a turbulent week for his administration.

Full Article: US DAILY BRIEF

SEK: EURSEK Narrowing Gap To Resistance At July 7 High

SEK is once again underperforming the G10 basket, with EURSEK up 0.45% and narrowing the gap to resistance at 11.2784 (Jul 7 high). Clearance of this level would see the cross fully unwind the June flash CPI-induced fall, suggesting markets do not consider the print a serious impediment to future Riksbank easing. We wrote yesterday that an August Riksbank cut still can’t be fully ruled out, with another inflation report still due on August 7 (flash print, final on 14th) and growth data printing softly in recent months.

- Clearance of the Jul 7 high in EURSEK would expose 11.3203, the 76.4% retracement of the March – April selloff.

- This morning, 5-year ahead money market participant CPIF inflation expectations fell two tenths to 1.8% - the lowest since July 2021. The survey was conducted between June 30 – July 6, so did not include the stronger-than-expected flash June inflation report. The Riksbank will likely need to see several 5-year prints below the 2% target to become concerned about a de-anchoring of inflation expectations, not just in the monthly money market participant survey but also the broader quarterly survey (which includes social partners’ expectations).

- The Swedish macro calendar thins out for the remainder of this week, but we will still pay attention to the Public Employment Service’s June labour market report tomorrow – particularly data on redundancies and vacancies.