EU FINANCIALS: {r1}{3h}{IC} Kvika Banki (KVABNK) - €200m WNG Sr Pref 4yr - FV

May-23 07:59

- IPT: MS+270

- The IPT is wider than we would have expected from our initial thoughts - https://mni.marketnews.com/44KL1lE - investors demanding higher debut issuer, issuer size and potential liquidity premiums for the small issue

- FV: MS+205-215bps

- Fellow Icelandic banks ARION, ISLBAN & LANBNN, all A- rated would price around MS+135 at 4Y. We think 2 notches back is worth around 40-50bps, giving a 175-185 range

- These banks tend to trade ~40-50bps back of similarly rated larger EUR banks, using EUROB 4.875% 2031 as a comp at z+130 we get a range of Z+170-180

- From 170-180 we consider that the small issue size may reduce liquidity and likely investors will demand an additional premium for the small debut issuer.

- This is despite the core balance sheet strength displayed in the roadshow with Q1 RoTE 17.7% and a 590% capital adequacy ratio, strong liquidity and good asset quality.

- Exp. Ratings: Baa2 (Moody's)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBP: Potential Hammer Formation Headed into Trade Talks

Apr-23 07:57

- Tariff and Fed-independence induced volatility has prompted the potential formation of a hammer in the GBP/USD daily chart which, if confirmed, could see the pair establish a base and resume the short-term uptrend. Strength through 1.3400-24 would be key here - opening the 1.3434 bull trigger (the Sep'24 high).

- The prospects of a UK-US trade deal remain front page news. Today's Times runs that the government is "hopeful" that a deal will allow the UK to avoid the worst of the tariffs - specifically the 25% tariff on steel, aluminium and car imports - however the 10% blanket tariff could be here to stay. Chancellor Reeves is set to meet the US Treasury Secretary on Friday. The Times concludes that ministers hope that they will be able to get a deal over the line by the end of the month.

- JP Morgan write that GBP strength on any US-UK trade deal would present good entry levels to fade over the medium term - with any deal unlikely to undo the key impacts of the last months events on the currency. The UK could also get caught between opposing demands from the US and EU on trade. As a result, they use favourable levels to enter a short GBP position vs NOK, SEK cash basket. They see Sterling’s stagflationary reaction function as remaining on the table as a threat over the rest of the year.

GILTS: 5s Cheapen On 2s5s10s Fly After DMO Revision, Still At Rich End Of Range

Apr-23 07:51

This morning’s DMO remit revision has seen 5s cheapen by ~5bp on the 2s5s10s butterfly.

- The structure failed to break below the June ’24 low (-47.2bp) in recent weeks.

- Any fresh questions surrounding the UK’s fiscal health or the pricing of a deeper BoE easing cycle could result in fresh richening for 5s on the structure.

- However, today’s early focus on the DMO’s remit, aggressive curve flattening and prevailing level compared to the recent range suggests that those looking to express such a view will not be rushing to engage at this stage.

Fig. 1: UK 2-/5-/10-Year Butterfly (bp)

Source: MNI - Market News/Bloomberg

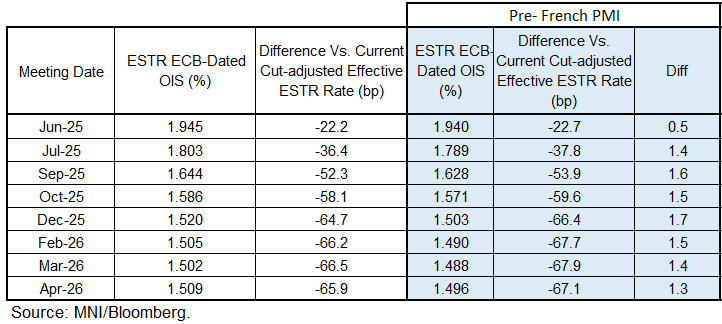

STIR: French/German Flash PMIs Don’t Change Near-term ECB Outlook

Apr-23 07:48

As noted above, there was little market reaction to the German and French flash April PMIs, even as both countries saw weaker-than-expected services readings. The prints haven’t really changed the outlook for near-term ECB policy, with a 25bp June cut still ~90% implied in OIS and a subsequent cut in July almost 60% implied.

- Year-end implied rates are ~1.5bps more hawkish than before the French data, with this morning’s rise in Bund yields setting the tone. 65bps of cuts are priced through December.

- After reaching a multi-month low of -39.0 ticks yesterday, the ER M5/M6 spread has since steepened back to -34.5 ticks at typing, +3.5 ticks on the session.