US DATA: Private Demand Softens Again In Q2 Flash But Could Have Been Worse

Jul-30 12:56

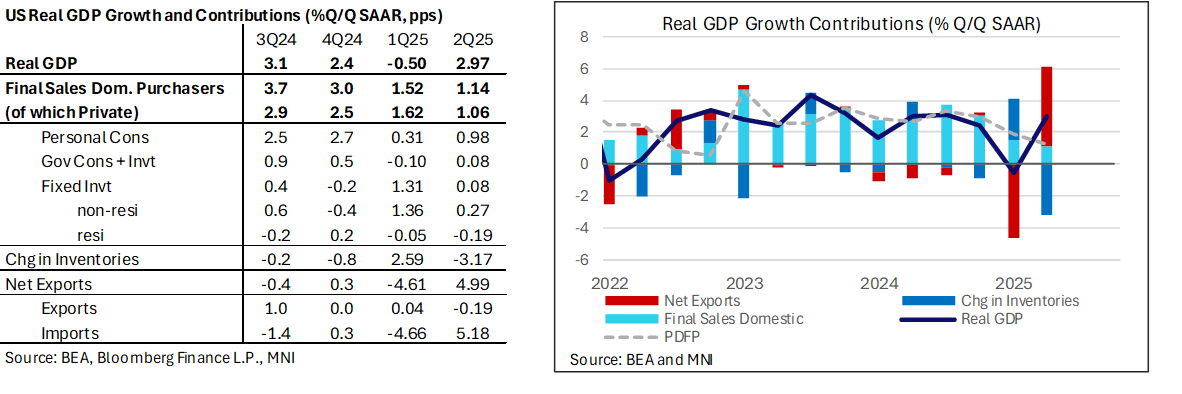

- Real GDP was stronger than expected in the Q2 advance release, rising 2.97% annualized vs Bloomberg consensus of 2.6%, although it was close to the 2.90% upgrade in yesterday’s final Atlanta Fed GDPNow entry.

- The 1.2% averaged in 1H25 compares with 2.5% in 2024.

- Private domestic final purchases (PDFP), a measure Powell frequently acknowledges, moderated further to 1.2% annualized (its weakest since 4Q22) from 1.9% in Q1. The 1.6% averaged in 1H25 compares with 3.0% in 2024.

- The 1.06pp contribution to GDP from PDFP was better than the 0.7pp pencilled in by GDPNow with an offset from weaker government consumption, only adding 0.1pp vs expectations of 0.4pp.

- The upward surprise to analyst expectations came away from private consumption, which underwhelmed slightly with 1.4% annualized (both Bloomberg consensus and GDPNow pencilled in 1.5%) after 0.5% in Q1. Tomorrow’s monthly PCE report for June will give a better idea of latest momentum.

- As for the noisier items, there were even larger swings in trade and inventories than expected, but they netted out relative to GDPNow expectations.

- Net exports: 4.99pp (GDPNow 4.00pp) after -4.6pp

- Changes in inventories: -3.17pp (GDPNow -2.2pp)

- Other notable contributions came from non-residential investment returning to a more typical 0.3pps after a booming 1.4pp in Q1 on likely tariff front-running whilst residential investment remains under pressure with -0.2pp. The latter has seen a volatile few quarters but its weakening trend is becoming increasingly clear with -1.3% Y/Y.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: EU Bank Put Spread

Jun-30 12:54

SX7E (18th July) 185/165ps, bought for 0.50 in 6k.

BONDS: Off Highs, Tight Ranges Intact

Jun-30 12:52

Generally sideways trade across major bond futures over the past couple of hours, with headline flow light and London morning ranges intact.

- The recently covered TY block sale applies some modest pressure, although contracts were already away from session highs.

- Lack of meaningful macro developments since London trade got underway, outside of the softer-than-expected German CPI data.

- Core global DM yields flat to 2bp lower on the day, early gilt outperformance vs. Tsys and Bunds more than reversed.

- EGB spreads to Bunds within ~0.5bp of Friday’s closing levels.

- Similarly, major global central bank pricing little changed vs. late Friday levels.

EGB OPTIONS: Bobl Put Spread seller

Jun-30 12:46

OEU5 117.50/116.50ps, sold at 29.5 in 2k.