IRAN: President To Gulf States: 'We Had No Choice But To Defend Ourselves'

Mar-04 16:31

President Masoud Pezeshkian posts on X: "Dear esteemed leaders of our friendly and neighboring count...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBP: GBPUSD Pullback Extends To 1.7%, BoE in Focus Thursday

Feb-02 16:21

- GBPUSD faces a similar fate to other major pairs on Monday, with an extension of the USD bounce pairing earlier strength in cable which saw it top out at 1.3868 multi-year highs on January 27. Price action capitalises on a bearish weekly and monthly close, following the rejection of the 1.3850 area.

- Next to well established USD focal points centering around the Warsh nomination, the sterling leg of the trade comes back into focus ahead of Thursday's Bank of England meeting. The MPC is expected to leave Bank Rate on hold and leave guidance unchanged, with questions twofold:

- First of all on the Agents' Annual Pay Survey, announced alongside the decision (MPC have already been privy to), which will be used as a guide for how sticky wage inflation is expected to be through 2026.

- Secondly, the individual member paragraphs will be watched - particularly Governor Bailey and both Breeden and Ramsden (assuming neither of the latter two vote for a sequential cut). Any hints guiding towards a March cut will be key here.

- Elsewhere, the results of the Feb 26 by-election risk to expose further cracks within the Labour party between loyalists to PM Starmer, and those on the left of the party speculated to be angling for a change in leadership. A serious leadership challenge would be GBP negative not only through higher instability but also through the potential for a new PM to favour fiscal expansion.

- Initial firm support for GBPUSD sits at the 20-day EMA, at 1.3578. Should the pair turn to retest the 1.3868 Jan 27 cycle highs that would result in a narrowing of the gap to the 1.40 area, which has moved from key support to resistance over the last three decades.

- Sellside views screen mixed on GBP: Scotia think "GBP’s latest upswing appears to be fundamentally supported by the rise in spreads" and TD Securities "can see some USD bounce back vs the GBP. Structurally, we like GBP upside vs the USD but downside vs the EUR." On EURGBP, CIBC say "the realization of market underpricing for March supports EUR/GBP […] look for a rebound back towards the 0.8716 high from 27 January", while Morgan Stanley say "a 'dovish hold' at the upcoming BoE, coupled with asymmetric downside risks to UK employment and inflation data, suggest that EURGBP longs via limited loss structures remain attractive."

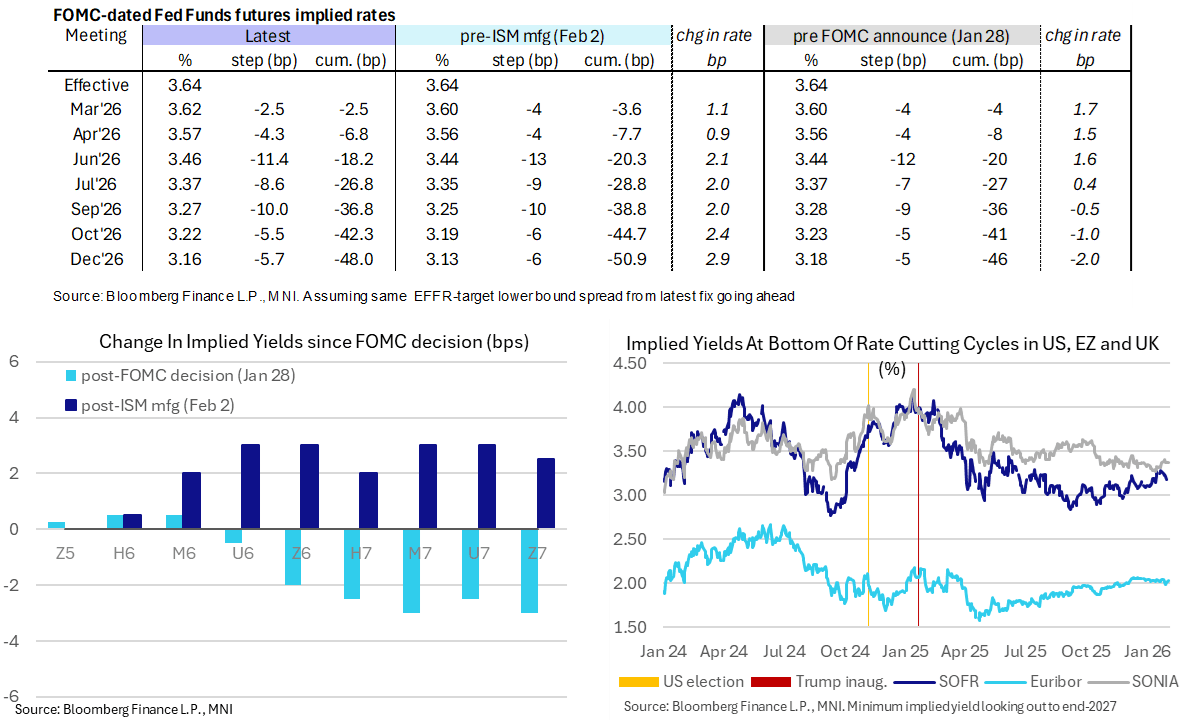

STIR: Hawkish Shift On ISM Manufacturing Held, Private Data In Near-Term Focus

Feb-02 16:18

- US rates are holding onto a swift hawkish shift on the far stronger than expected ISM manufacturing report, building on moves that had grown in the two hours ahead of the report despite oil prices still down heavily (WTI 1st -4.8%).

- FF implied rates are 1-3bp higher for meetings out to end-2026 since ISM, with renewed expectations of a next Fed cut coming in Jul rather than Jun (the latter 18bp vs 22.5bp as US desks filtered in).

- Cumulative cuts from 4.33% effective: 2.5bp Mar, 7bp Apr, 18bp Jun, 27bp Jul, 37bp Sep, 42.5bp Oct and 48bp Dec.

- SOFR futures are mostly 2-3 ticks lower post-ISM for 4-5 ticks lower on the day, with the terminal implied yield at 3.225% (Z6, +5bp) lifting off its lowest since mid-Jan.

- The shift unwinds much of the dovish moves that have played out since last week’s FOMC decision – see chart.

- As for upcoming data releases, we expect the ongoing partial government shutdown to rule out a JOLTS release tomorrow. Wednesday’s ADP and ISM Services releases will see additional focus whilst Friday’s BLS nonfarm payrolls report remains at risk of publication and will need a prompt re-opening to remain on schedule.

FED: US TSY 13W AUCTION: NON-COMP BIDS $1.832 BLN FROM $89.000 BLN TOTAL

Feb-02 16:15

- US TSY 13W AUCTION: NON-COMP BIDS $1.832 BLN FROM $89.000 BLN TOTAL