POWER: Poland's February Climbs 12% On Week, Gap Widens Further from EMAs

Poland’s February settled around 12% higher on the week to track price increases in European coal and EU ETS, while cooler temperature forecast continues to provide an outlook for strong heating demand. The contract ended the week well above its 10-day and 20-day EMAs, with the gap widening on the week.

- EUA DEC 26 up 0.3% at 92.49 EUR/MT

- Rotterdam Coal FEB 26 up 1.2% at 96.45 USD/MT

- Poland’s February baseload power settled at PLN575/MWh compared to its settled price of PLN561.32/MWh on 15 January, according to data on Polish power exchange TGE.

- The contract climbed for the six consecutive session to reach another fresh all-time high and remains well above the 10-day EMA and 20-day EMAs at €534.63/MWh and 516.53/MWh, respectively, (see chart).

- EUAs Dec26 are on track to increase by just above near 4% on the week. Support comes from ongoing bullish sentiment since late 2025 amid tighter supplies this year.

- Average temperatures in Warsaw were generally unchanged over 1-28 February and expected to be below the seasonal norm throughout the period.

- The 829MW unit 5 at the 3GW Opole plant is still planned to be offline over 8 February-1 March.

- Despite this, over February, power plant availability will be firm next month.

- Closer in, average temperatures in Warsaw were mostly revised higher over 17-21 January, however temperatures will be below the seasonal norm throughout the 14-day ECMWF forecast – dropping to as low as -16.5C on 26 January, albeit it up from -18.80C estimated on 15 January for the same day.

- The 630MW Plock power plant will still have planned works until 24 January, with the 910MW Jaworzno 2 power plant still curtailed by 507MW until 17 January, extended from 16 January.

- The 1.83GW Turow power plant will be fully available to the grid by 20 January.

The day-ahead dropped to PLN514.07/MWh for Saturday delivery from PLN536.11/MWh for Friday amid typically lower weekend power demand and as wind is expected remain firm on the day at a 42% load factors tomorrow, edging down 47% today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Democrat Obamacare Petition Reaches 218 Backers, Set To Face Full House Vote

Following on from Rep. Brian Fitzpatrick (R-PA) (US: GOP Moderate Signs Dem Petition As Healthcare Battle Dominates Congress), three more moderate Republicans - Mike Lawler (R-NY), Rob Bresnahan (R-PA) and Ryan Mackenzie (R-PA) - have signed House Minority Leader Hakeem Jeffries' (D-NY) discharge petition seeking a clean, three-year extension to healthcare premium subsidies under the Affordable Care Act (ACA). This circumvents House Speaker Mike Johnson (R-LA) and forces a full floor vote on the issue.

- It is unclear whether the eventual floor vote will succeed. Lawler said before signing the petition that “I still believe a straight three-year extension is not the right policy. But I fundamentally believe doing nothing is even worse. “And to me, leadership left us with no option.” Instead, Speaker Johnson may look to re-open the issue within the House Republican conference and move forward with moderate amendments, rather than risk outright defeat to the Democrats. In any case, Johnson is set to emerge from the healthcare battle in a weakened position.

- So far, the White House has kept the healthcare issue, risking a spike in premiums for millions of Americans, at arms-length given the toxic political debate within the GOP and Congress in general on the topic. It remains to be seen whether this remains the case with the discharge petition going to the House floor.

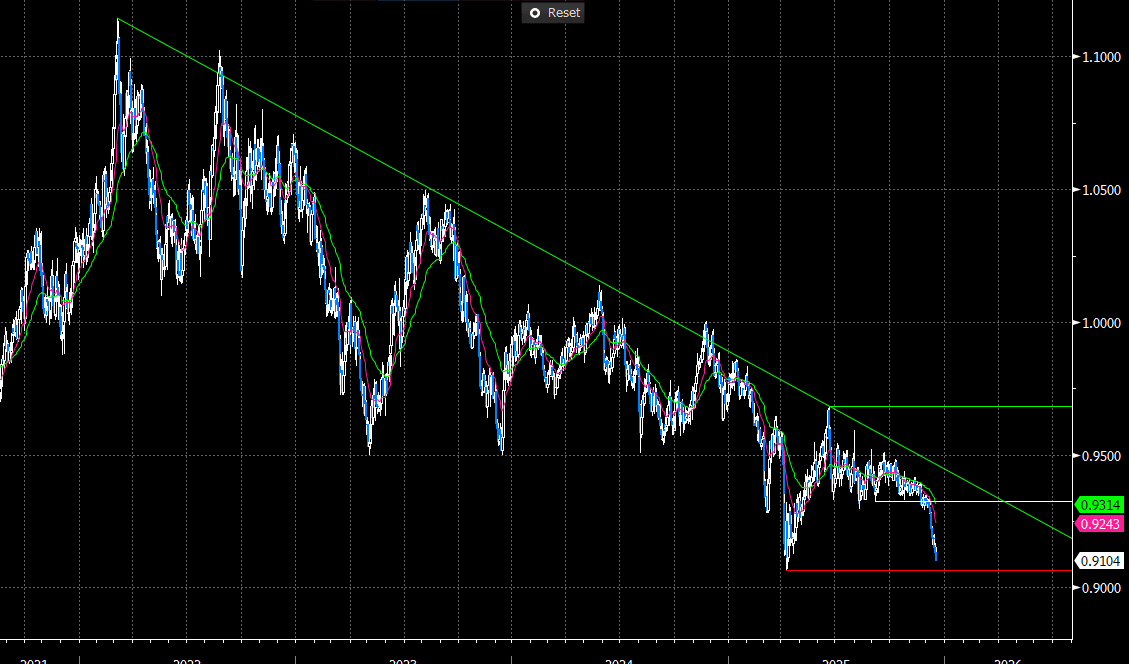

SCANDIS: NOKSEK Probing 0.9100, Key Support At 0.9065

NOKSEK is probing the 0.9100 figure amid a brief impulse of SEK strength. This narrows the gap to key support at 0.9065, the April 9 low.

- Tomorrow’s Riksbank and Norges Bank decisions may set the tone for the cross into year end.

- On balance, we see dovish risks to the Riksbank and hawkish risks to the Norges Bank. If realised, this may help NOKSEK find a short-term bottom.

- We highlighted last week that NOKSEK has entered a key long-term support zone around 0.9000 – which may prove a solid psychological barrier to further downside heading into next year.

Figure 1: NOKSEK Since 2022 (Source: Bloomberg Finance L.P)

GILTS: OI Continues To Signal Low Conviction Markets Despite 'Credible' Budget

OI data points to fairly low conviction trade in gilt futures between December 9-16, with OI in the contract essentially unchanged across that window.

- Over a slightly longer horizon, post-Budget OI dynamics also fail to signal high conviction net long setting in the contract despite the market deeming Chancellor Reeves’ (relatively backloaded on the tightening side) fiscal plans to be credible.

- OI in the contract has only risen by ~7K or 0.6%, in the time since the Budget.

- Price action is also unconvincing in the time since, with the contract settling ~30 ticks below pre-Budget closing levels on Tuesday (today’s CPI-driven rally takes it ~30 ticks above the same closing level).

- Cash curve considerations are slightly more constructive over that window, with the 2s10s and 5s30s curves flattening, adding by the DMO’s ongoing skew away from long end issuance.