CANADA: PM-Deep Negotiations Ongoing w/US & Restarting Broad Engagement w/China

Prime Minister Mark Carney has just finished speaking at a presser, ostensibly focused on measures to combat crime, but is also addressing questions on other topics.

- On relations w/the US, Carney says that "We are engaged in deep negotiations with the US on several sectors", and that "There are times to hit back against the US, and there are times to talk, and right now is the time to talk."

- On relations w/China, PM says "We are restarting a broad engagement with China [and] in the process of having discussions on a much broader range of issues than single sectors." Says that he expects to meet senior Chinese leaders in the coming month [likely at the APAC summit in South Korea at end-Oct].

- Claims that the CEO of multinational autos manufacturer Stellantis told him the firm is looking at producing a different model at the Brampton, Ont. plant. This comes after the Canadian gov't threatened Stellantis with legal action after the auto manufacturer announced plans for a USD13bln investment in the US and the shift of assembly of its Jeep Compass model to Illiniois. The auto sector remains a major employer in Ontario, and the impact of US tariffs continues to pose a major economic and employment risk to industrial regions of the province.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Back Near Pre-Retail Sales Levels After Two-Way Moves

- Treasuries have on the whole pushed back to pre-retail sales levels, having sold off on the stronger than expected release before what was a hard to square away rally shortly after.

- The recent losses go against S&P 500 futures holding and recently extending their intraday decline, after earlier losses initially appeared to be supporting the bid in bonds.

- TYZ5 is back to 113-12+ (-02+) from an earlier high of 113-18, having seen a post-0830ET data low of 113-08+. Cumulative volumes are on the low side again, having just nudged over 800k.

- Resistance remains at 113-29 (Sep 5 high), as part of a bullish trend sequence, whilst support is seen at 112-25+ (20-day EMA).

- Cash yields range from 1bp lower (2s) to 1bp higher (10s and 20s) on the day, with 20s continuing to modestly underperform with upcoming supply.

- $13bn 20Y re-open at 1300ET (912810UN6). Last week’s 30Y auction was on the screws but with stronger details. That’s in contrast to last month’s 20Y auction which was in-line but with the bid-to-cover slipping from 2.79 to 2.54 and indirect take-up dropping from 67.4% to 60.6%.

- Beyond retail sales, the day’s data was mixed with stronger import prices partly offset by further large downward revisions to prior months, with a similar story for IP and a surprisingly soft NY Fed services survey.

MNI EXCLUSIVE: EU Officials On Inflation Implications From CO2 Trading Scheme

European officials and parliamentarians look at the implications of ETS2 CO2 trading rules for inflation. -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

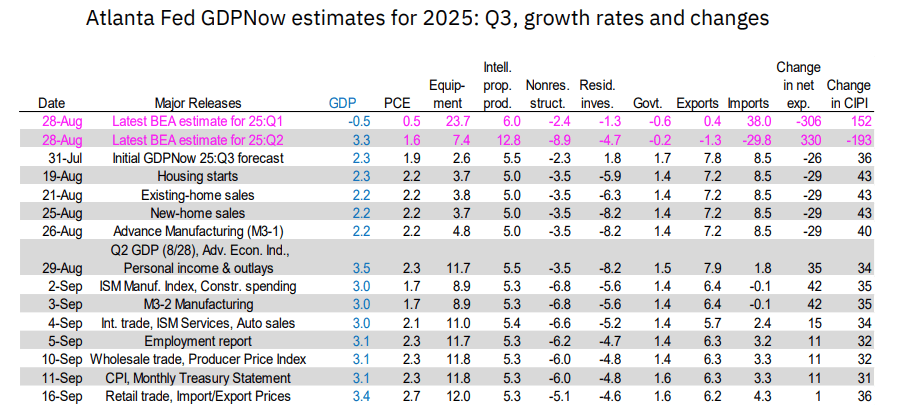

US OUTLOOK/OPINION: GDPNow Suggests Pickup In Private Domestic Demand In Q3

The Atlanta Fed's latest GDPNow estimate for Q3 jumped to 3.41% from 3.09% in the last full update on September 10 (and 3.3% posted in Q2). This was very much a domestic demand-driven upgrade, with real PCE now seen contributing well over half of growth (1.85pp vs 1.54pp in the previous estimate) thanks to better-than-expected advance retail sales.

- The underlying details from the GDPNow estimate imply final sales to private domestic purchasers, closely watched by the Fed, is growing at around 2.4%, a pickup after 1.9% in both Q1 and Q2.

- "After recent releases from the US Census Bureau, US Bureau of Labor Statistics, and Treasury's Bureau of the Fiscal Service, the nowcasts of third-quarter real personal consumption expenditures growth and real gross private domestic investment growth increased from 2.3 percent and 6.2 percent, respectively, to 2.7 percent and 6.9 percent, while the nowcast of the contribution of net exports to third-quarter real GDP growth decreased from 0.23 percentage points to 0.08 percentage points."

- The next release will be Wednesday after housing starts/permits data.