PLN: Zloty Holds Stable, Updates On Budget Eyed This Week

EUR/PLN is stable, trades marginally below the previous close, last at 4.2670. Familiar technical levels remain in play. Bears look for a move towards the 4.25 area and a cyclical low of 4.2471 in particular. Bulls are seeking recovery towards Aug 28/Sep 12 highs of 4.3039/43.

- Finance Minister Andrzej Domanski flagged the need to amend the 2025 budget due to the need to mitigate the effects of recent floods. The government will meet to discuss the matter on Saturday.

- Comments from MPC members have been converging around March as the potential starting point for a serious debate about cutting rates. Iwona Duda joined the ranks of policymakers signalling that loosening policy could be discussed at that point.

- POLGB yields sit 2.9-6.6bp lower across the curve, with 8s outperforming. The WIG20 Index operates 0.9% above neutral levels.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

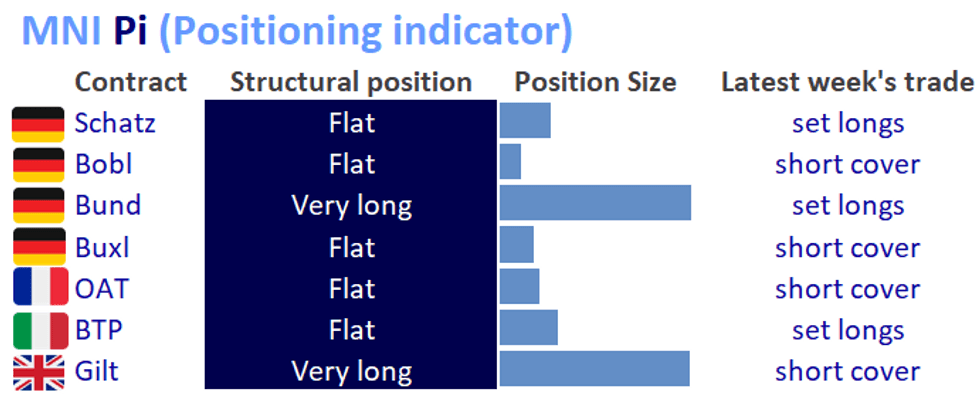

BONDS: MNI Europe Pi (Positioning Indicator): Flat/Long Pre-Roll

We've just published our latest MNI Europe Pi Positioning Indicator (PDF here):

- As we head into the quarterly Eurex roll (last trade for Sept contracts is Sep 6th), European bond futures structural positioning is largely flat.

- Longs built in early August have evaporated, with the exception of Bund and Gilt.

- Last week saw mixed indicative trade, with some longs set and some short covering across various contracts.

FOREX: FX OPTION EXPIRY

Of note:

EURGBP 2.58bn at 0.8475.

EURUSD 1.34bn at 1.1150.

EURUSD 3.43bn at 1.1150/1.1200 (wed).

USDJPY 3.51bn at 145.25/145.50 (wed).

AUDNZD 1.98bn at 1.0920 (thu).- EURUSD: 1.1100 (1bn), 1.1150 (1.34bn), 1.1170 (447mln).

- EURGBP: 0.8440 (225mln), 0.8450 (404mln), 0.8475 (2.58bn).

- USDJPY: 144.30 (550mln), 144.80 (280mln), 144.90 (456mln), 145.20 (438mln).

- USDCAD: 1.3485 (434mln), 1.3550 (430mln).

GILTS: 10-year Gilt/Bund Spread Widens As UK Markets Catch Up

The 10-year Gilt/Bund spread has mechanically widened over 4bps this morning to 174bps, as UK markets catch-up with FI counterparts following yesterday’s Bank holiday. This week’s UK data calendar lacks tier 1 releases, with focus on remarks from BoE's resident hawk Mann, due to speak tomorrow in Frankfurt.

- A near 3% surge in crude futures following Libyan supply outages weighed on global FI yesterday.

- The UK cash curve has bear steepened, with yields 3.5 to 4.5bps higher.

- In futures, U4 remains the active contract, though the roll to Z4 will likely be complete by tomorrow/Thursday. U4 currently trades -41 ticks at 99.53, with Z4 -50 ticks at 98.98.

- Overnight, the BRC shop-sales index fell 0.3% Y/Y (vs 0.2% prior).

- A reminder that BoE Governor Bailey re-iterated the August MPS guidance in his Jackson Hole remarks on Friday, endorsing a “steady course” for monetary policy.

- UK PM Starmer is expected to deliver his “State of the Nation” speech at around 10am today.