US DATA: Philly Fed Post-Election Optimism Fades

Dec-19 15:50

The Philadelphia Fed Business Outlook survey took an unexpected turn for the worse in December, with the index for current general activity dropping to -16.4 from -5.5 prior, versus the rise to +2.8 expected.

- That was the worst outturn since April 2023, and weakness was widespread throughout the survey: New Orders (-4.3, lowest since May) and Shipments (-1.9) both declined and turned negative, while Employment dipped 2 points to 6.6 and the average workweek index fell back into negative territory (-8.2) after a November jump.

- Optimism has faded too: the future general activity index dropped 26 points to 30.7 after two consecutive rises, with future new orders, future shipments, future employment, future capex, and future prices paid dropped - future prices received rose though. Note that optimism was a 42-month high in November, seemingly related to the election results, but that impact has more than fully reversed.

- And on inflation, prices paid rose 5 points to 31.2, though prices received dropped for a 3rd consecutive month to 7.3. A gap appears to be opening up between the two measures - this is the widest spread (-23.9) since April 2022, potentially suggestive of margin pressures building.

- Overall we would discount the month-to-month readings, but it's clear that the post-election optimism among regional manufacturers has faded, and the survey continues to point to sluggish manufacturing activity.

- Indeed, using appropriate weightings, this survey is equivalent to a roughly 49 ISM Manufacturing reading.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK DATA: MNI UK Inflation Preview - October 2024

Nov-19 15:42

- After reaching its near-term trough in September, UK CPI is expected to increase in October, largely driven by utilities prices, but the main focus will remain on services inflation which is expected to remain broadly unchanged.

- Consensus expects the more important services CPI to print broadly around the same level as in September (MNI median 4.9%, MNI mean 4.91%, Bloomberg consensus 4.9%, BOE 4.97%). We remain wary of upside risks from air fares.

- We also see the potential for moves higher in clothing and second hand car prices within core goods.

- A decent surprise either way in services CPI could move the market, but if the upside risks that we have identified prevail to see a higher-than-consensus print we still think there is scope for cuts at least in February and May (which aren’t quite fully priced by the market yet). We therefore think there is potential for a bigger market move on a downside surprise.

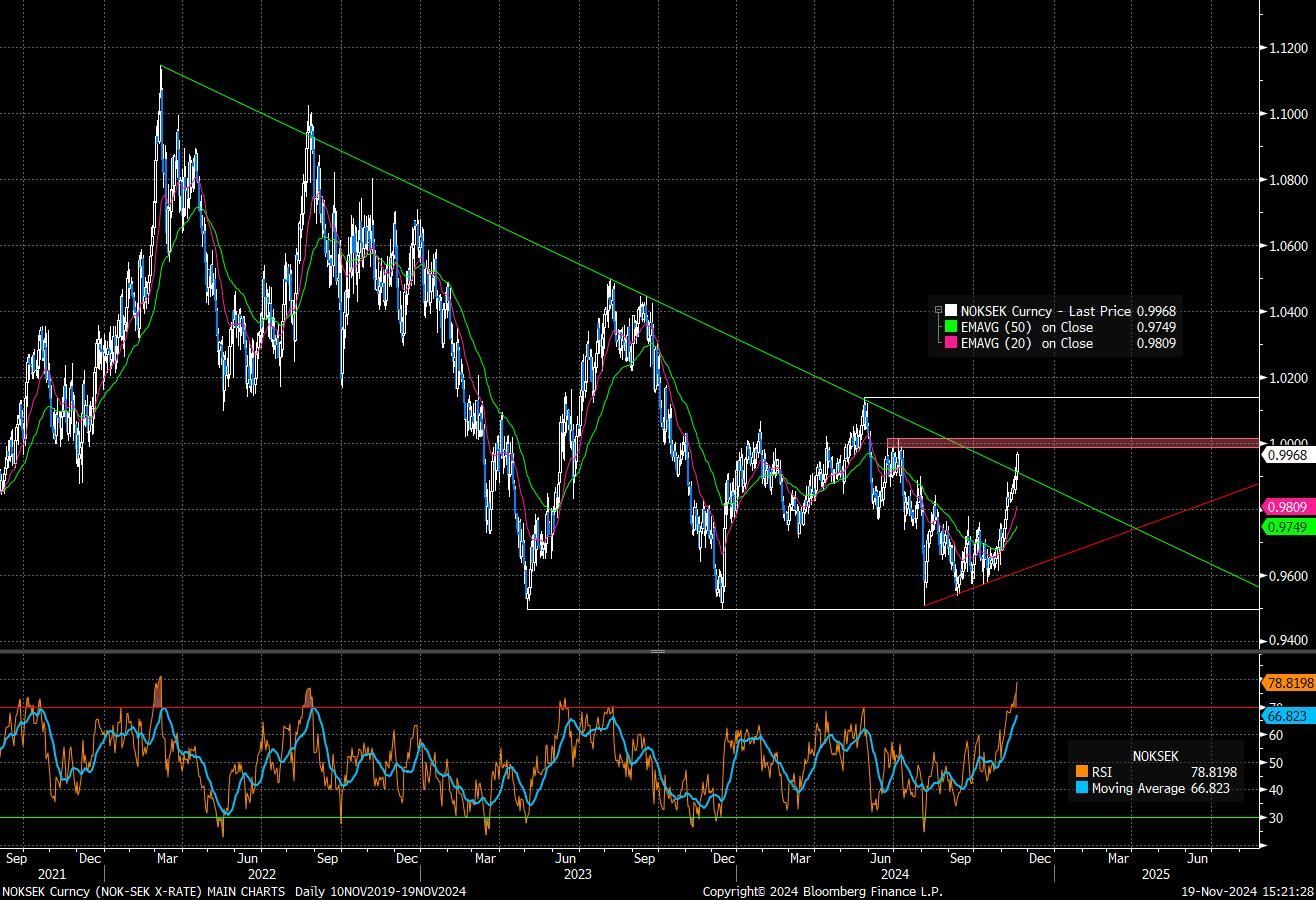

SCANDIS: NOKSEK Breaches Trendline Resistance, Eyes Parity

Nov-19 15:35

NOKSEK has pushed through trendline resistance drawn from the March 2022 high, allowing the aggressive November rally to reach 3%.

- Clustered resistance around 0.9988 (June 21 high), parity and 1.0016 (July 4 high) provides the next topside target. However, we caution that the 14-day RSI has reached its most overbought since March 2022 - which was followed by a consolidative phase and a >5% move off highs.

- As such, a meaningful push beyond parity may first require some profit taking, to allow the overbought condition to unwind. Initial support is the 20-day EMA at 0.9793 and smaller pullbacks will be considered corrective.

- Intraday strength (+0.55%) has largely been SEK led, with the krona pressured alongside risk assets on this morning’s Russia/Ukraine war escalation.

- More broadly, this month’s rally has been aided by a cautious Norges Bank decision on Nov 7 and breaches of key resistance levels.

- Tomorrow’s Scandinavian data calendar is light, but Thursday sees Q3 Norwegian GDP (expected at 0.3% Q/Q by analysts and Norges Bank). A softer than-expected print may increase speculation of a Norges Bank rate cut in December. However, we continue to see a Q1 2025 cut as most likely, absent a major surprise in growth and inflation readings ahead of the Dec 19 decision.

US: No Changes In Core Leadership Team Expected In House Democrat Elections

Nov-19 15:31

House Democrats will hold internal leadership elections today, with little change expected to the core leadership team.

- House Minority Leader Hakeem Jeffries (D-NY), Minority Whip Katherine Clark (D-MA), and Caucus Chair Pete Aguilar (D-NY) are all running unopposed despite Democrats' failure to recapture control of the House.

- Punchbowl notes: “…rank-and-file lawmakers are largely pleased with their leaders, concluding that House Democrats did the best they could in a tough political environment. The anger and frustration from rank-and-file Democrats is aimed at the top of the ticket, not their own leaders.”

- Craig Caplan at C-Span notes: "The key contested race is for Democratic Policy and Communications Committee (DPCC) chair, the House Democrats’ chief messenger, between current chair 5th term Rep. Debbie Dingell (D-MI) and 1st term Rep. Jasmine Crockett (D-TX)."

- There is also interest in the successor to outgoing Annie Kuster (D-NH) as chair of the Centre-left New Democrat Coalition, a group expected to wield more power in the Democrat caucus after a backlash to progressive influence. The Washington Examiner notes that Rep. Brad Schneider (D-IL), current New Dems vice chairman for communications, will take on Rep. Sharice Davids (D-KS), vice chairwoman for new member services, for the role.