PERU: Peru: Market Reaction to President Impeachment – Neutral

(PERU; Baa1/BBB-BBB)

• The market shrugged off the latest Peru presidential impeachment with Peru USD 36s unchanged in price as we expected given the country has had 3 presidents in about four years and seven in the past nine years, so it has become part of the political landscape.

• Peru inflation is low, economic growth is solid, gross debt/GDP is one of the lowest in Latin America at 33.7% according to the IMF, external debt/GDP is also relatively low at about 15%, and reserves are strong based on IMF ARA measures.

• Ex-President Boluarte at last count had an approval rating of 3% and violent crime was escalating while certain comments she made on the issue seemed insensitive so finally, she was ousted with a congressional leader replacing her until the election next year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Monitoring Support

- RES 4: 151.62 61.8% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 150.92 High Aug 1 and a key resistance

- RES 2: 149.81 76.4% retracement of the Aug 1 - 14 bear leg

- RES 1: 147.61/149.14 20-day EMA / High Sep 3

- PRICE: 147.35 @ 16:31 BST Sep 10

- SUP 1: 146.21 Low Aug 14

- SUP 2: 145.86 Low Jul 24

- SUP 3: 145.53 Trendline drawn from the Apr 22 low

- SUP 4: 145.40 50% retracement of the Apr - Aug upleg

USDJPY continues to trade inside a range. Attention is on key short-term support at 146.21, the Aug 14 low and a bear trigger. A break of this level would highlight a stronger bearish threat and highlight a range breakout. This would expose 145.40, a Fibonacci retracement. On the upside, clearance of 149.14, the Sep 3 high is required to reinstate a bullish theme. Moving average studies are in a bull-mode position, highlighting a dominant uptrend.

US PREVIEW: August CPI: Analyst Unrounded Core CPI Range: 0.29-0.36% (3/4)

Below is our collation of detailed analyst expectations for the August CPI report, ordered from lowest-to-highest core CPI % M/M expectation.

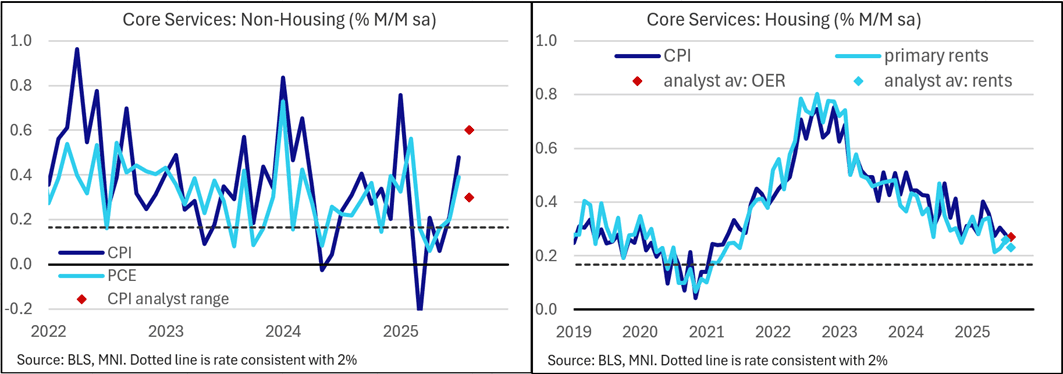

US PREVIEW: August CPI: Supercore Seen Cooling From July (2/4)

In terms of the category-by-category breakdown, supercore CPI is seen slowing from July's 0.48% (albeit there is a very wide range of views) to around 0.40% with housing CPI seen relatively steady but upside pressure vs July in services areas such as lodging and car insurance (airfares are also seen remaining strong). Outside of the categories below - Medical care printed 0.8% M/M in July, a 34-month high, but this is seen moderating at least somewhat in August.

- And core goods prices are roundly seen higher (had printed a below-expected 0.21% in Jul), with vehicle prices seen driving much of the upside, and tariff-impacted categories like apparel seen by many to accelerate.

- Analyst Expectations Of Key Sequential Drivers:

- Lodging away from home (+ve): After a 5th consecutive monthly contraction (1% M/M decline in July), lodging prices are seen rebounding somewhat (0.4% median).

- Used cars (+ve): Prices here are seen picking up from July’s 0.5% M/M, with some estimates above 1% for the highest print since January. While industry data suggests flat M/M prices, the seasonal adjustment is seen pushing SA CPI higher.

- Airfares* (small -ve): While airfare inflation is seen moderating in August, that’s to a still-robust pace (3%, ranges between 1.9 and 5.5%) from 4.0% in July.

- Apparel (neutral): Limited forecasts for this tariff-sensitive category suggest something similar or slightly higher than the 0.07% M/M seen in July.

- Vehicle insurance* (small +ve): Again, a very slight acceleration is seen for auto insurance (0.3-0.4% from 0.1%).

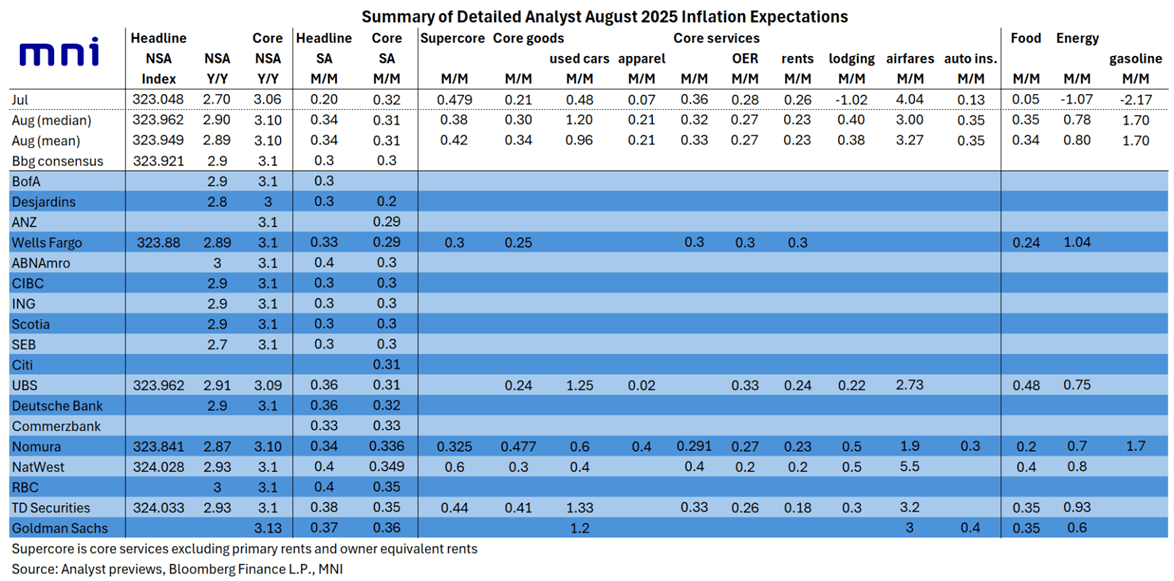

- Rents (neutral to slight -ve): OER and rents are seen steady or perhaps a little softer in August vs July, with risks seen as largely to the downside amid a perceived secular decline in market rents. OER is seen at around the same 0.28% M/M in August, with rents a few basis points lower from July’s 0.26%.

- Non-core: Food (+ve): Food prices surprised to the downside in July at under 0.1% M/M, but are seen bouncing in June with around 0.3-0.4% M/M gains expected.

- Energy (+ve): A resurgence in gasoline prices in August on a seasonally-adjusted basis is expected to help July’s -1.1% M/M in this category largely reverse, with estimates centering around +0.8% M/M.