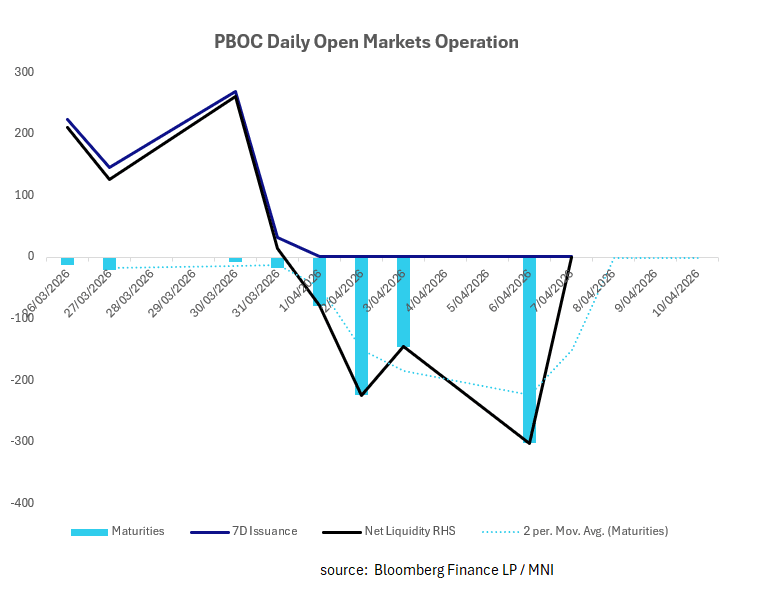

CHINA: PBOC Injects CNY0.5bn via OMO

The shortened week this week for OMO was dominated by the 3-month reverse repo to sure up liquidity ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

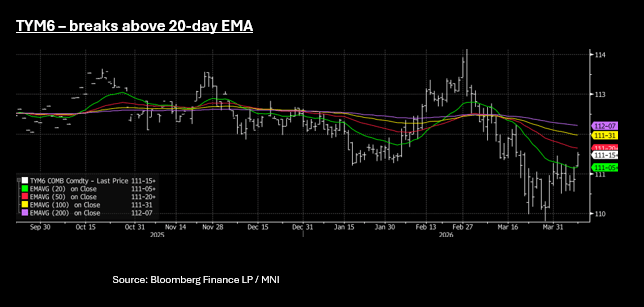

US TSYS: Yields Gap Lower on Ceasefire, TYM6 Breaks Above Key Level

Yields are trending lower again in the Asia trading day as the agreed two week extension removes some of the short term risks. Yields are down 4-6bps in shorter maturities with the front end outperforming.

- The 2-Yr is down -5.8bps at 3.734%

- The 5-Yr is down -4.7bps at 3.882%

- The 10-Yr is down -3.7bps at 4.26%

- The 30-Yr is down -1.5bps at 4.859%

Us bond futures are higher with the 10-Yr up +19+ to 111-15+. This sees TYM6 back above the 20-day EMA of 111-05+ for the first time since the beginning of March as the 'war premium' was built into markets. Above is the 50-day EMA at 111-20+.

What happens next is now the key debate and likely anyone's guess. More details will follow no doubt but for now bond markets may turn to the economy for its next steer.

STIR: RBNZ-Dated OIS: No Chance Of A Hike Priced Today

RBNZ-dated OIS pricing shows no tightening is priced for today, while December 2026 assigns 49bps.

- That said, December 2026 was showing 59bps earlier today but has since softened following news of an US-Iran ceasefire.

- President Trump has said the US will suspend bombing and attacks on Iran for two weeks following a Pakistan-linked request that includes a deadline extension. The US has received a 10-point proposal from Iran, with the two-week window intended to finalise a potential agreement, while any ceasefire remains conditional on the reopening of the Strait of Hormuz.

- Notably, market pricing remains flat to 15bps firmer than levels seen prior to February’s RBNZ decision.

Figure 1: RBNZ Dated OIS Current

Source: Bloomberg Finance LP / MNI

CHINA: Net Liquidity Unchanged Following Today's OMO

Repo rates remain stable and at the lower end of recent ranges and with a modest maturity schedule after today, it seems likely that this week could see muted injections for the remainder of the week.

- The PBOC issued CNY0.5bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY0.5bn of 7-day reverse repo

- Net liquidity unchanged

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.34%, from prior close of 1.32%.

- The China overnight interbank repo rate is at 1.21%, from the prior close of 1.20%.

- The China 7-day interbank repo rate is at 1.34%, from the prior close of 1.33%

.