SPAIN: Parliament To Convene With No Clear Path To New Speaker, Let Alone PM

The new parliamentary session in Spain gets underway on 17 August, with the 350-member Congress of Deputies meeting for the first time since the May general election. The first task for the new parliament will be to elect a new speaker as well as four deputies and four secretaries. The speaker's election could give a sign of how easy or difficult it will be to hold a successful investiture vote for a prime minister in the future.

- The parliamentary arithmetic could not be tighter.

- The right-wing bloc of the conservative Popular Party (PP), right-wing nationalist Vox, and regionalist Navarrese Popular Union (UPN) hold 171 seats.

- The leftist/regionalist bloc of PM Pedro Sanchez's Spanish Socialist Workers' Party (PSOE), far-left Sumar, centrist Basque Nationalist Party (PNV), Basque separatist EH Bildu, regionalist Republican Left of Catalonia (ERC) and leftist Galician Nationalist Bloc (BNG) hold 171 seats.

- This makes the decisions of the single member from the regional-interest Canarian Coalition (CC), and the hard-line pro-Catalan independence Together for Catalonia (Junts) with seven deputies crucial.

- In order to win, a speaker (or prime ministerial) candidate needs an absolute majority in the first round (176) or a simple majority in the second.

- Junts have stated they will not support the PP due to Vox's inclusion, but their demands on the PSOE (amnesty for exiled leader Carles Puigdemont to return, a legal referendum on self-determination) could prove too high a price for Sanchez to pay.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: ECB Pricing Little Changed On The Day

ECB-dated OIS is little changed to start the week, with the liquid contracts generally operating within 1bp of Friday’s closing levels at typing. Recent price action in wider core global FI markets has kept any pay-side flow in check.

- ECB speak has seen Governing Council member Vasle warn against the high and resilient nature of core inflation.

- Elsewhere, the Bundesbank flagged a risk of slower than expected German GDP growth vs. previous expectations, while also outlining expectations for core inflation to remain very high over the summer, even with a moderation in general inflation potentially in play over the coming months.

- All in all, ECB-dated OIS prices a 25bp hike at next week’s meeting with virtual certainty, while a little over 42bp of cumulative tightening is showing through September. Beyond there, a terminal deposit rate just above 4.00% is priced, with those measures all operating in familiar territory.

- The latest BBG survey of economists indicated a central expectation for a terminal deposit rate of 4.00% to be reached in September.

- This afternoon will see Executive Board member Elderson & Governing Council Member Vujcic appear on a panel.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jul-23 | 3.645 | +24.3 |

| Sep-23 | 3.823 | +42.1 |

| Oct-23 | 3.893 | +49.1 |

| Dec-23 | 3.926 | +52.4 |

| Jan-24 | 3.916 | +51.4 |

| Mar-24 | 3.888 | +48.6 |

| Apr-24 | 3.818 | +41.6 |

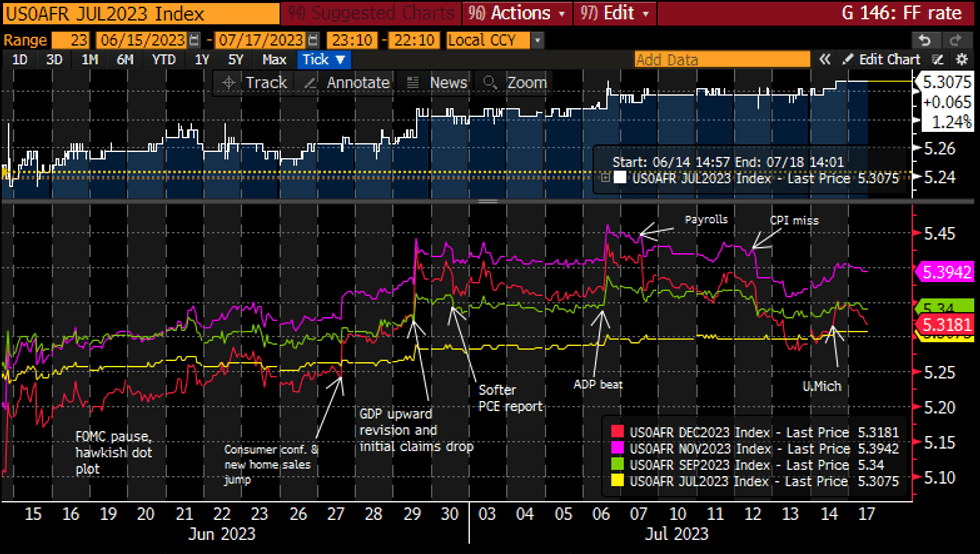

STIR: Fed Implied Rates Reverse U.Mich Pop On Softer China GDP

- Fed Funds implied rates are only marginally lower for the next couple meetings but with increasingly large declines further out, mirroring the belly led rally in Treasuries on softer than expected China GDP growth. The move helps reverse most of Friday’s push higher on the strong U.Mich survey.

- Cumulative change from 5.08% effective: +22.5bp Jul 26 (unch), +26bp Sep (-1bp), +31bp Nov (-1bp).

- Cuts from 5.39% Nov terminal: 8bp to Dec (from 6bp), 78bp to Jun’24 (from 73bp) and 153bp to Dec’24 (from 148bp).

- The Fed is now in media blackout. In the flip side to Jefferson’s skip narrative ahead of the June FOMC blackout, the final guiding message this time came from a hawkish Waller.

Source: Bloomberg

Source: Bloomberg

LOOK AHEAD: Monday/Tuesday Data Calendar: Retail Sales, IP/Cap-U, TIC Flows

Slow start for the week, data picks up Tuesday with Retail Sales for June, Industrial Production, Capacity Utilization and TIC flows. The Fed in policy blackout through July 27.

- US Data/Speaker Calendar (prior, estimate)

- Jul-17 0830 Empire Manufacturing (6.0, -3.5)

- Jul-17 1130 US Tsy $65B 13W, $58B 26W Bill auctions

- Jul-18 0830 Retail Sales Advance MoM (0.3%, 0.5%)

- Jul-18 0830 Retail Sales Ex Auto MoM (0.1%, 0.4%)

- Jul-18 0830 Retail Sales Ex Auto and Gas (0.4%, 0.4%)

- Jul-18 0830 Retail Sales Control Group (0.2%, 0.3%)

- Jul-18 0830 New York Fed Services Business Activity (-5.2, --)

- Jul-18 0915 Industrial Production MoM (-0.2%, 0.0%)

- Jul-18 0915 Capacity Utilization (79.6%, 79.5%)

- Jul-18 0915 Manufacturing (SIC) Production (-0.2%, 0.0%)

- Jul-18 1000 Business Inventories (0.2%, 0.2%)

- Jul-18 1000 NAHB Housing Market Index (55, 56)

- Jul-18 1000 Fed VC Barr, housing conference

- Jul-18 1130 US Tsy $50B 42D CMB auction

- Jul-18 1600 Net Long-term TIC Flows ($127.8B, --)

- Jul-18 1600 Total Net TIC Flows ($48.4B, --)