EM LATAM CREDIT: Paraguay Upgraded to 'BBB-' from 'BB+'

"S&P Lifts Paraguay Rating to Investment Grade, Joining Moody’s" - Bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Gov Generated Data Gradually Resuming, Chip Makers Under Pressure

- Treasuries look to finish modestly higher Monday - inside a relatively narrow session range after scaling back from pre-NY open highs, backlogged economic data gradually starting to flow.

- Currently, the Dec'25 10Y contract trades +4 at 112-21 (112-15.5 low / 112-24.5 high), Treasuries last week challenged resistance at the 113-02 level, an area of congestion since Nov 5. This hurdle remains intact, however, a clear move above it would be a bullish signal and shift focus on resistance at 113-18+, the Oct 28 high. A break would also cancel a short-term bearish theme. For bears, attention is on 112-10, the 100-DMA and 112-06, the Sep 25 low.

- August construction data - whose Oct. 1 release was delayed 6 weeks due to the federal government shutdown - showed a 0.2% M/M rise in spending (-0.1% expected, 0.2% prior rev from -0.1%). The NY Fed's Empire State Manufacturing Survey impressed in November, with the current General Business Conditions index rising 8 points to a 1-year high 18.7 (well above the 5.8 expected).

- Fed Vice Chair Jefferson said he's likely one of the 9 FOMC members who anticipated cutting rates in Sep, Oct and Dec (in his September Dot Plot) and if forced to guess we would think he is still marginally in favor of a December cut and here he again highlights "increased downside risks to employment compared to the upside risks to inflation, which have likely declined somewhat recently".

- Stocks hit hard Monday, Chip makers continue to lead late session declines followed by Financial names. Note, Nvidia is expected to release Q3 earnings this Wednesday.

- Tuesday data schedule is light, with markets gearing for the now much-delayed September NFP print due this Thursday. Fed speak: Fed's Barkin is due to comment on the economic outlook having not commented directly on policy since the last Fed decision. Barkin had previously seen less caution around the jobs market given the unlikely circumstance of broad layoffs given such a slow pace of hiring in recent years.

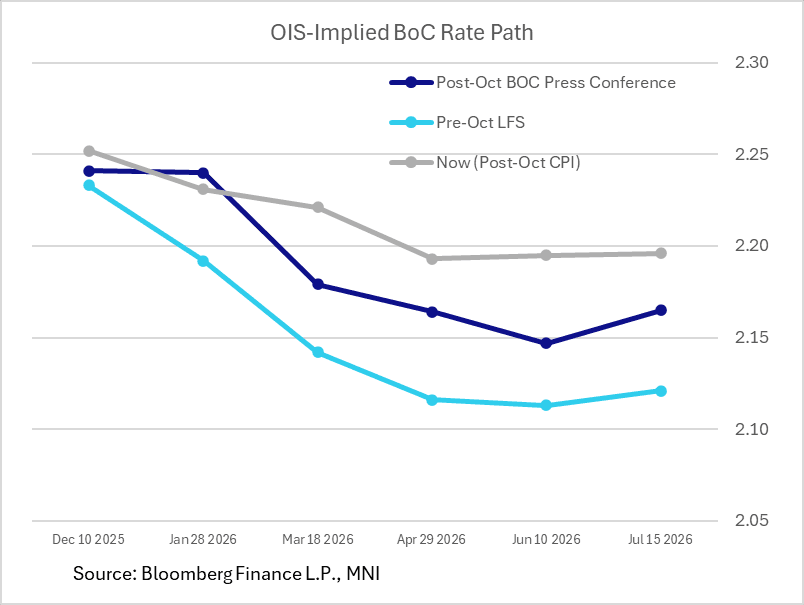

BOC: Latest Data Affirms Conviction On Prolonged BOC Hold

Firm core indicators in the October CPI report, in conjunction with the month's stronger-than-expected Labour Force Survey, have combined to pretty much eliminate expectations for a further Bank of Canada cut in this cycle let alone December, with the terminal rate now seen just ~5bp lower (vs 8bp pre-data, and 14bp pre-LFS).

- Coming into this week, BMO was the only Canadian bank that still sees another BOC cut in this cycle, though only in January - there's no mention of any change in its view post-CPI: "On the surface, this looks to be a mildly friendly report with headline and median inflation rates dipping. However, the sources of relief were well-known ahead of time, and the new news here is not great, driven by persistent strength in insurance costs and a snap higher in cell charges. Overall, this does little to change the BoC's view that underlying inflation remains close to 2-1/2%; but, if anything, most underlying metrics have been stuck a bit above that, or have just crept up there. In other words, this report is just another reason to believe the Bank is moving to the sidelines in December."

- Other analysts in alphabetical order:

- CIBC: "While headline inflation decelerated in October, the move was only broadly in line with expectations and it would take a longer period of easing price pressures, combined with indications of economic growth deteriorating again, to bring the Bank of Canada back off the sidelines. We continue to forecast no change in the overnight rate through to the end of next year."

- Desjardins: "With a broad group of inflation measures remaining in the top half the Bank of Canada’s 1% to 3% operating range and the economy still expected to just escape falling into recession in Q3 2025, there is little pressure on the BoC to continue cutting rates at this time. We maintain our view that the Bank of Canada will be on hold for the next year."

- National: "In its latest interest rate decision, the central bank stated that it considered it had done enough...October's employment data, which showed a decline in the unemployment rate and an acceleration in wages, combined with today’s inflation figures, will reinforce its conviction. We continue to view the Canadian economy and labour market as being in excess supply, and the outlook is not reassuring without a trade agreement with the United States, but inflationary pressures are persisting longer than normal. This limits the BoC's room for maneuvering to give the economy some relief."

- RBC: "Core price pressures remain sticky at rates above the BoC's inflation target, consumer demand has proven resilient to-date despite international trade uncertainty, and fiscal policy is set to provide support to growth in the year ahead. The BoC has indicated the overnight interest rate is "about the right level" provided inflation and economic activity continue following the October projections. Given that backdrop, we do not expect further interest rate reductions from the BoC."

- Scotiabank: "the BoC doesn’t seem to know which measure(s) of core inflation it’s primarily interested in and so markets also have difficulty determining how the BoC would view the readings. Regardless, the clear message from the BoC is that it is on a prolonged hold barring major shocks...These are not light readings on balance. The suite of them over recent months indicates that core inflation remains too persistently too warm to a) have eased of late, and b) for any further easing to be contemplated."

- TD: "The mixed performance across core inflation measures does not give the BoC much clarity on underlying price pressures, but we believe the gradual deceleration in CPI-trim/median and fading CPI breadth should allow the Bank to keep policy slightly accommodative through 2026."

AUDUSD TECHS: Shooting Star Candle Highlights A Reversal

- RES 4: 0.6648 2.0% 10-dma Envelope

- RES 3: 0.6644 76.4% retracement of the Sep-Oct bear leg

- RES 2: 0.6618 High Oct 29 and a key near-term resistance

- RES 1: 0.6580 High Nov 13

- PRICE: 0.6502 @ 16:16 GMT Nov 17

- SUP 1: 0.6459 Low Nov 5

- SUP 2: 0.6440 Low Oct 14 and key support

- SUP 3: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

AUDUSD continues to trade below last week's high. Recent gains undermine a bearish theme, however, note that last Thursday’s activity also highlights a potential bearish reversal signal - a shooting star (inverted hammer) candle. Key short-term pivot resistance has been defined at 0.6580, the Nov 13 high. A break of this level would cancel the candle pattern. A sell-off would instead expose 0.6440, the Oct 14 low.