NOK: Outperforming G10 Basket, Bearish Theme In EURNOK Intact

NOK outperforms the G10 basket today, with EURNOK down 0.6% at 11.2075 having tested the Feb 19 low at 11.2019. A bearish theme remains intact, with this week’s modest gains prior to today’s session considered corrective. Next support is the December 2023 low at 11.1760, which shields the more important July 2023 low at 11.0965 and the psychological 11.0000 figure.

- NOKSEK is up 0.4% to 0.9515. The 0.9500 has provided decent resistance in recent sessions, helping the cross consolidate a strong year-to-date rally.

- There hasn’t been an obvious driver for the magnitude of today’s krone outperformance. Crude oil and natural gas futures have risen this morning amid the latest US/Iran concerns – but front benchmarks remain below yesterday’s highs.

- Meanwhile, Norges Bank’s monthly FX transactions pointed to another month of daily krone buying ahead – but this isn’t a surprise. While central bank flows are undoubtedly more supportive than last year (both from an actual flow and psychological standpoint), it’s worth remembering that they are the flipside of lower petroleum tax revenues relative to previous years.

- Finally, this morning’s retail sales and labour market data were resilient, but are no means gamechangers for the Norges Bank outlook (which has already significantly hawkishly repriced this month). Next week’s Norwegian calendar includes Q4 balance of payments data – our focus will be on net FDI flows and ex-GPFG portfolio flows.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD Recovers Marginally, Fed Tone Closely Watched

- The Dollar Index has recovered marginally across Asia and through the European morning, however the broader view on the USD remains lower. Prices are consolidating somewhat following the 3.9% losses seen over the last 2 weeks or so to yesterday's 95.55, the lowest print since February 2022.

- Against the backdrop of the Trump administration's aggressive trade threats, the likelihood of a Rieder-led Fed and the possibility of another gov't shutdown, focus turns to today's FOMC meeting. The main question here will be if Chair Powell makes any changes to his message from December that the FOMC is "well positioned to wait to see how the economy evolves". On USD valuations, Powell should keep his stance of that being a matter of the Treasury.

- CAD outperforms and is in focus as today's BoC meeting provides a potential catalyst on top. With the second consecutive hold firmly expected, there is uncertainty in which direction the next move be. While a break of 1.3540, key medium-term support, could extend bearish conditions, the trend has entered oversold territory, and a corrective bounce would allow this condition to unwind.

- USDCHF meanwhile has seen a 0.8% bounce this session after extending down to fresh decade lows of 0.7605 yesterday. 2015 lows sit at 0.7406 (Bloomberg data). Risk sentiment should be a key determinant on if the likes of AUD or NZD or rather the Swiss franc will book stronger gains should the current dollar weakness extend.

- Trump also mentioned yesterday the new Fed chair announcement will be "soon", today's FOMC meeting could be an event the administration is targeting the announcement around. Rieder has consolidated around 50% implied odds for the position over the past couple of sessions while Warsh is the runner-up at ~25%.

- In terms of data the calendar is light with just MBA Mortgage applications scheduled.

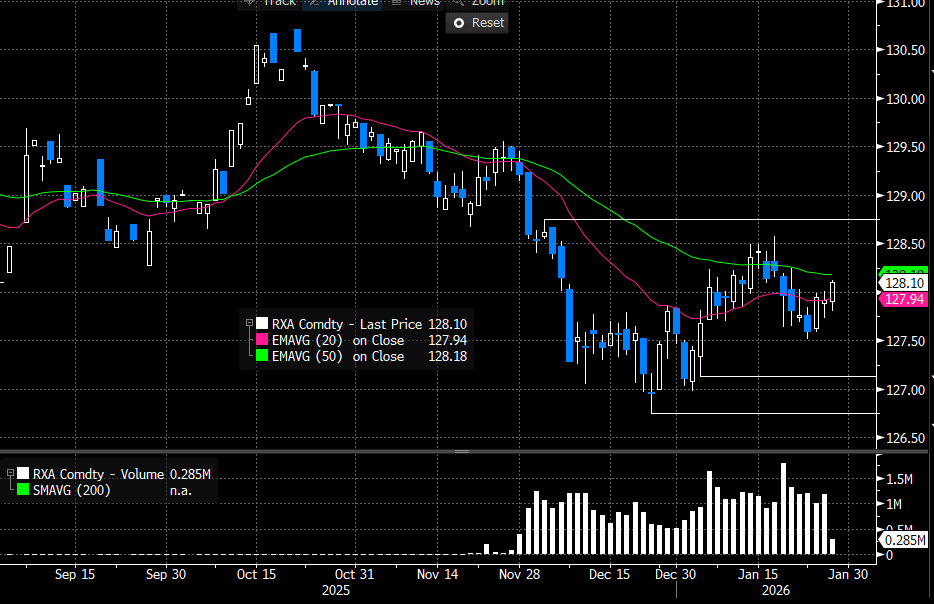

EGBS: German Curve Bull Steepens On Dovish ECB Signals

The German curve has bull steepened following somewhat dovish commentary from ECB’s Kocher and Villeroy this morning. Schatz and Bobl yields are down 3bps, after Kocher suggested to the FT that continued EUR appreciation could create “a certain necessity to react in terms of monetary policy”. Villeroy similarly noted that the exchange rate was one factor guiding policy.

- Note that in the same interview, Kocher stressed that recent EURUSD appreciation has been “modest” and does not necessitate a response for now – we think this aligns with the median Governing Council view.

- 10-year yields are down 2.3bps to 2.85%, though heavy impending supply (E6bln of the 2.90% Feb-36 Bund) is likely containing downside to an extent.

- German 5s30s is +2bps at 104.5bps. The spread has been relatively rangebound since mid-September, with a tighter implied distribution of ECB outcomes coming alongside a more muted-than-expected impact from Dutch pension fund transition flows.

- Bund futures are +17 ticks at 128.09. The trend outlook remains bearish and recent short-term gains are considered corrective. Initial resistance is the 50-day EMA at 128.19.

- 10-year EGB spreads to Bunds are little changed. Portugal will sell OTs at 1030GMT. French PM Lecornu survived two more censure votes yesterday – as expected.

- Broader global focus remains on today's BOC and Fed decisions.

Figure 1: Mar-26 Bund Futures (Source: Bloomberg Finance L.P)

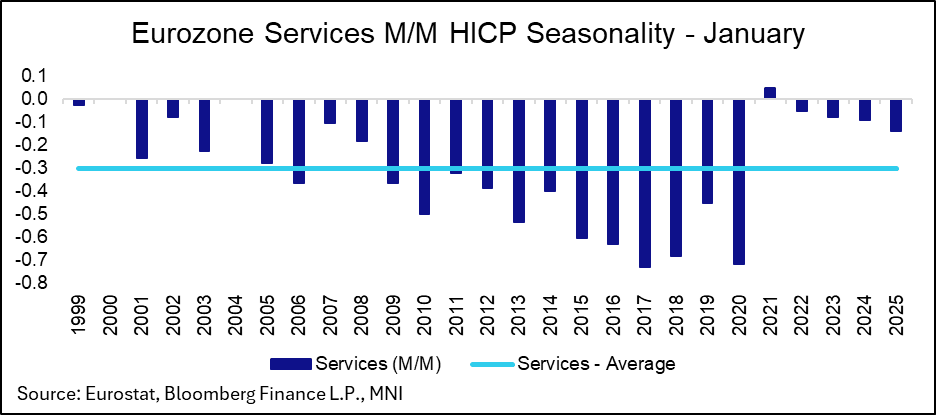

EUROPEAN INFLATION: MNI Eurozone Inflation Preview – January 2025

We've just published our preview of the January Eurozone inflation round - DOWNLOAD FULL REPORT HERE

Price Resets and Idiosyncratic Factors To Shape January Report

- The Eurozone January flash inflation round is split across two weeks. Germany and Spain are scheduled to release data on Friday January 30, with France due Tuesday February 3 and Italy, the Netherlands, and the Eurozone aggregate following on Wednesday February 4. The release will be an important input ahead of the ECB's February 5 decision. While the bar to a near-term rate change in either direction remains high, the data will inform assessments of the balance of risks for 2026.

- Headline inflation is expected to decelerate to 1.7% Y/Y (vs 1.9% prior). Across categories, analysts expect energy HICP to ease materially to around -4.5% Y/Y (from -1.9% in December). This will primarily be driven by base effects following January 2025's strong 3.0% M/M print, but some idiosyncratic factors are also at play.

- Core inflation is seen roughly stable to marginally lower at 2.2% Y/Y, with a small expected uptick in core goods not enough to offset a deceleration in services. Food, alcohol and tobacco is expected to see little changes around 2.5% Y/Y with no major seasonal effects beyond normal January patterns.

- There is more uncertainty than usual surrounding the January release due to several idiosyncratic factors.