IRAN: Optimistic Iran War Headlines Generate 0.4% Rise In Euro Equities

Apr-24 11:23

* Correction to the above: The key X post from Al Arabiya is here: "Al Arabiya correspondent: Paki...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

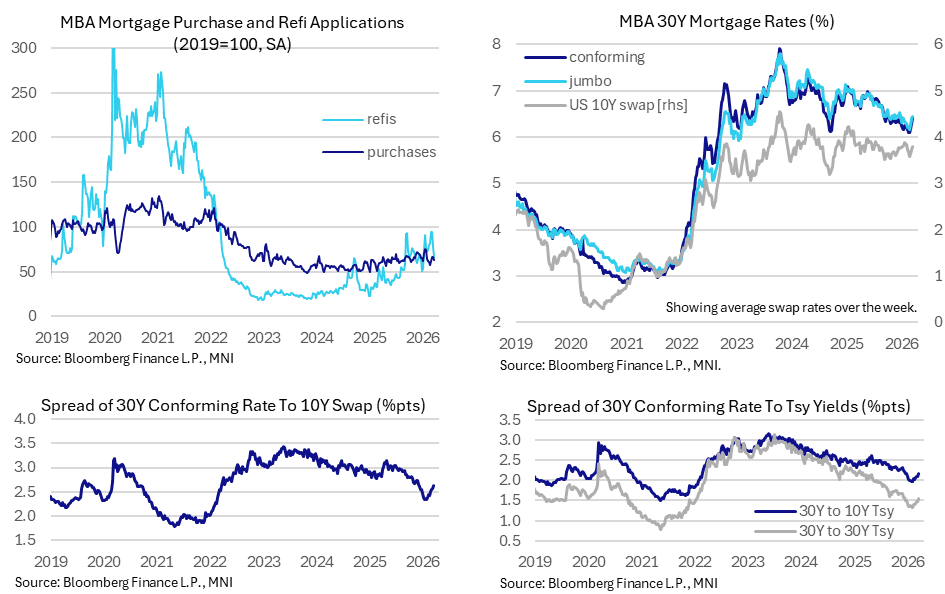

US DATA: Mortgage Applications Slip Further As Rates Climb Again, Spreads Wider

Mar-25 11:17

- MBA composite mortgage applications slipped another -10.5% (sa) last week after -10.9% the week prior, hitting their lowest level since the turn of the year.

- Refis again led this weakness (-14.6% after -18.5%) but new purchase applications also softened (-5.4% after 0.9%) with their largest weekly decline since end-Jan.

- The new purchase applications trend leaves at best flat momentum for housing market activity.

- Higher rates are clearly having an impact, with the 30Y conforming mortgage rate climbing another 13bp after 11bp and 10bp increases in the previous two weeks. It’s a 34bp increase from 6.09% in late Feb in what had been its lowest since Sep 2022.

- A widening in mortgage spreads has been fuelling this rate increase in recent weeks after a material tightening seen through 2H25 and into early 2026.

- The spread of 30Y mortgages to 10Y Tsy yields averaged 217bp last week (from 210bp the week prior) vs high 190s in mid-Jan to early Feb, whilst the spread to 10Y swap rates averaged 264bp (256bp the week prior) vs in the 230s in mid-Jan to early Feb.

EURIBOR: Today's ESTR vs Euribor Spread

Mar-25 11:16

- ESTR vs ERM6 has traded in ~24.2k Today. Some of the spreads are attributed at the time of the lower Fixing, selling the Spread.

- ESTR vs ERZ6 has traded in 15.2k total Today.

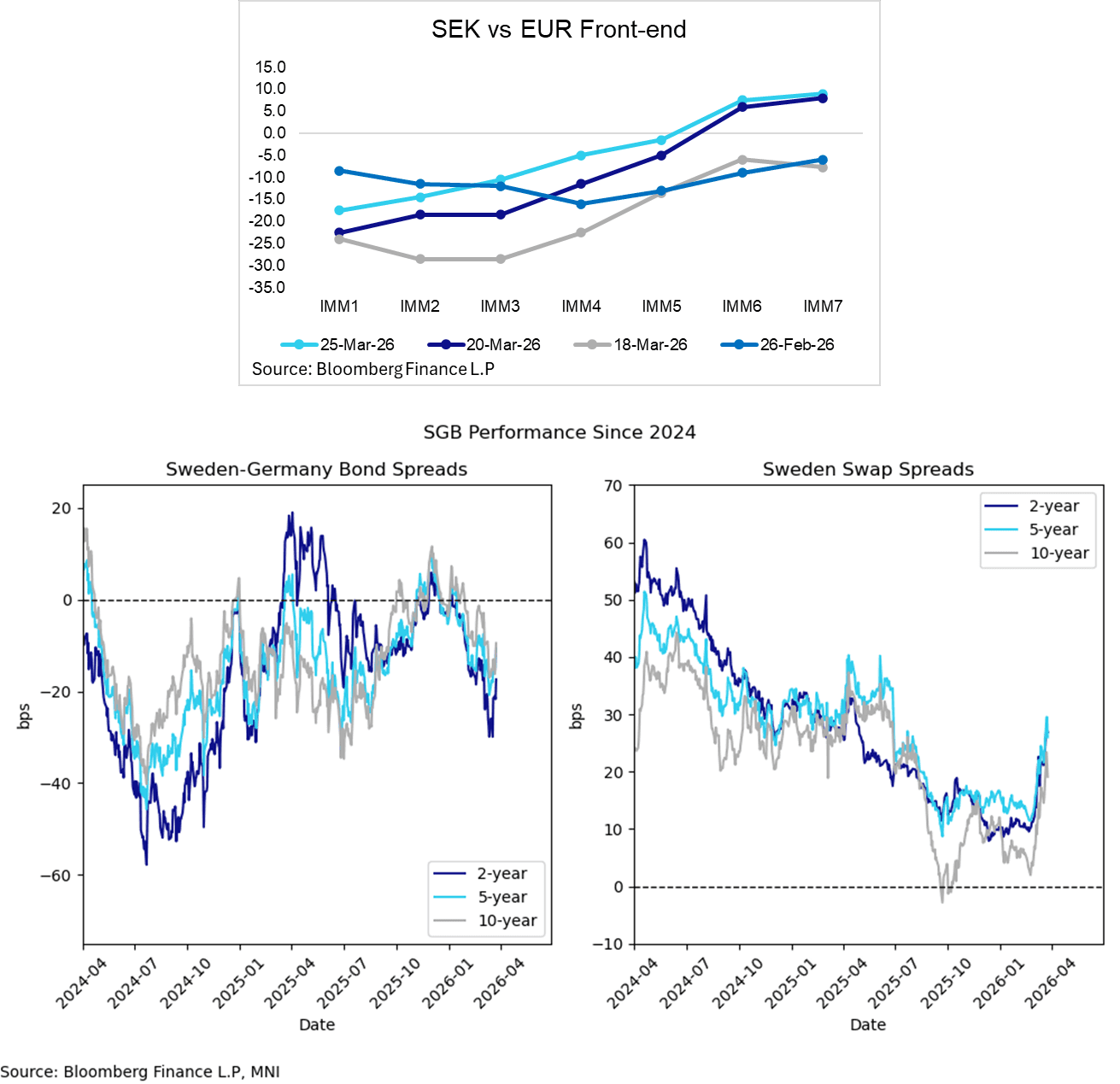

SWEDEN: Front-end SEK-EUR Curve Shifts Up Again, May Be Too Aggressive

Mar-25 11:13

We think this morning’s March Economic Tendency Indicator and March Riksbank minutes have somewhat reduced the likelihood of a Riksbank hike as early as May. Several Board members noted that economic conditions before the Iran war stared may allow for some patience before responding to the energy shock with rate hikes.

- However, there remains plenty of time before the May 7 decision to keep a May hike on the table. Board members are certainly cognizant of the risks from the “hawkish” scenario in the March MPR. Although the Jun26-Sep26 SEK FRA is down 2.5bps today at 2.365% (19.5bps above the 3M STIBOR rate), SEK-EUR front-end spreads still sit wider on the session.

- SEK-EUR spreads have risen notably since the Riksbank decision, with end-2027 spreads now in positive territory (U7 current at +8.5bps). That could be viewed as too aggressive, assuming the Riksbank will be more active in unwinding any hikes compared to the ECB, given Sweden’s rate sensitive economy and low underlying inflation conditions before the war started.

- Further out the curve, today’s 10-year 2.50% Oct-36 SGB auction saw a bid-to-cover of 1.47x for the SEK6bln issued – the lowest on record for that line (excluding the June 16th 2025 exchange auction). That has seen the 10-year SGB/Bund spread extend earlier widening, now +4.5bps on the session at -11bps.

- The 10-year SEK swap spread has narrowed 2.5bps today to ~19bps, down from a multi-month high of 23bps on Monday. Since the Iran war started, SGBs have been one of the few sovereign bonds to exhibit clear “safe haven” properties versus swaps. The 10-year SEK swap spread was around 4bps on Feb 26.