ITALY AUCTION PREVIEW: On offer Tuesday

Oct-26 16:35

The MEF will look to sell the following next week (total E7.5bln BTP plus E1.25bln CCTeu):

- E1.0-1.5bln of the 2.20% Jun-27 BTP (ISIN: IT0005240830)

- E2.0-2.5bln of the on-the-run 5-year 4.10% Feb-29 BTP (ISIN: IT0005566408)

- E3.0-3.5bln of the on-the-run 10-year 4.20% Mar-34 BTP (ISIN: IT0005560948)

- E1.0-1.25bln of the 0.80% Oct-28 CCTeu (ISIN: IT0005534984)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

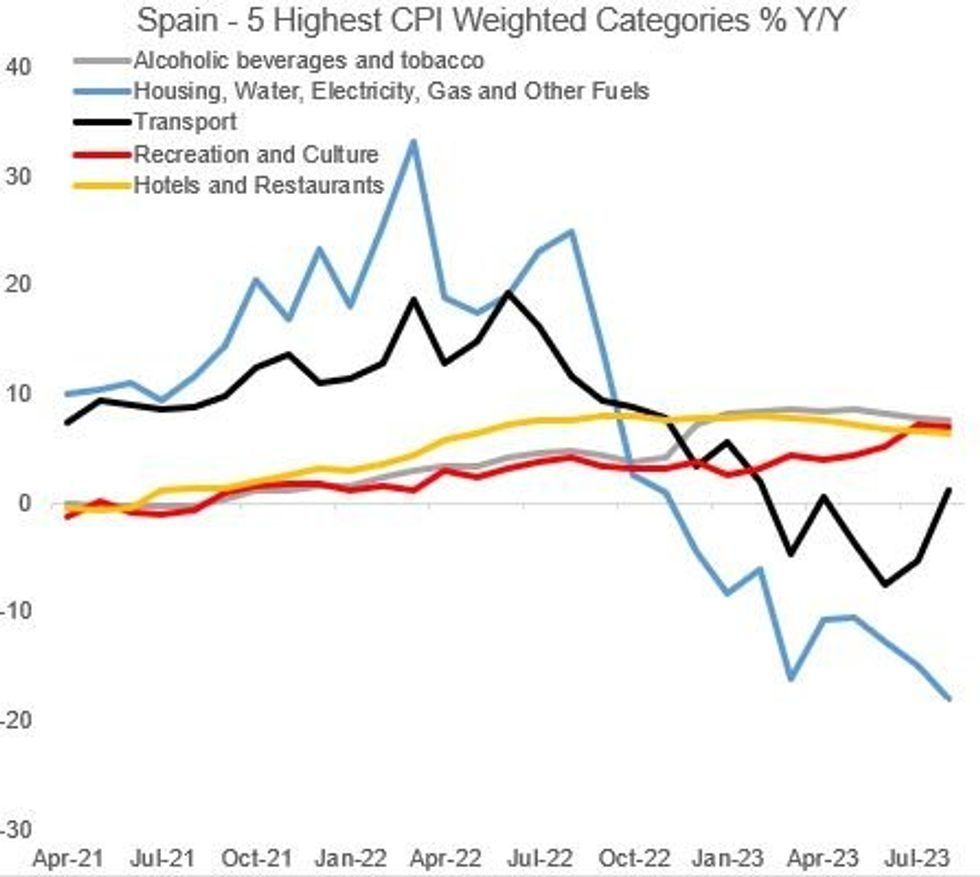

EUROZONE DATA: Spain Inflation Preview: Acceleration On Energy Prices

Sep-27 14:29

Spain (11% of EZ HICP) – 0800UK Thu 28 Sep

Consensus expectations:

- HICP: 3.3% Y/Y (vs 2.4% prior); 0.6% M/M (vs 0.5% prior).

- CPI: 3.5% Y/Y (vs 2.6% prior); 0.2% M/M (vs 0.5% prior).

- Core CPI: 6.0% Y/Y (vs 6.1% prior).

Energy prices are expected to be the main contributor to September inflation domestically (which will also push up the Euro-area headline rate). While energy still expected to fall Y/Y, a sequential monthly increase in electricity prices act as an offset.

- Some analysts note that the clothing component will not see sequential monthly increases as large as usual in September, owing to a weak summer sales period and a basket reweighting effect.

CANADA: OSFI Consulting On Negative Amortization Mortgages, Banks Addressing Risk

Sep-26 16:29

- Bloomberg reports the OSFI’s Routledge saying the economy is doing better than expected, with the regulatory body to wait for more information before deciding on bank capital levels in December.

- On mortgages, he says the body is still consulting with banks on negative-amortization mortgages and that they have a “precise” view into the negative-amortization problem.

- The OSFI has previously proposed tougher bank rules on extended mortgages back in July, at the time being open for comment until Sep 1 (see more here).

- He goes on to add that banks are beginning to address mortgage risk.

STIR: BoE Peak Pricing Ticks Up Tuesday, ECB Implied Eyes Inflation Catalyst

Sep-26 16:26

- ECB peak hike pricing was little changed by Tuesday's close, with a 4.05% depo rate seen in December 2023 (implying 5bp of hikes from current levels). With just 2bp priced for October's meeting. the next potential major catalyst for an uprating is the Eurozone September flash inflation data due Thu and Fri (MNI's preview is here).

- There was no change today in expectations for cuts expected in the year following the peak rate, at 61bp by end-2024.

- BoE terminal pricing ticked 3bp higher, with the 18bp in cumulative hikes priced by for Feb 2024 representing the highest implied Bank Rate (5.43%) since last Thursday's close. Near-term pricing didn't change much though with just 9bp of a hike seen in November (around 36% prob of a 25bp raise, unch from Monday's close).

- Around 79bp of cuts are seen in the year following the peak - 1bp greater than seen at Monday's close.