OIL: Oil Rallies On Tough EU Comments, US Stock Build May Pressure Prices

Trading in recent months has been characterised by concerns over excess supply pushing prices lower and an expansion of sanctions on Russia driving them higher. Prices rose on Tuesday following comments from EU foreign minister Kallas that increased expectations of stricter restrictions on Russia. The announcement of new US/EU sanctions in October pressured Russia’s Urals benchmark and it is down further this week. Reports of another US oil inventory build may pressure prices on Wednesday.

- Kallas said that Russia’s actions against the EU constitute “state-sponsored terrorism” prompting expectations of further sanctions. There have been numerous incursions of airspace over recent weeks.

- WTI rose 1.3% to $60.69/bbl after a high of $60.93. It had traded below $60 through Tuesday’s APAC and early European sessions before breaking above. Initial resistance is at $62.59 with the bear trigger at $55.96.

- Brent is up 0.9% to $64.78/bbl off the intraday peak of $65.10, holding below resistance at $65.95. The bear trigger is at $59.97.

- Ukrainian attacks on Russian refineries and sanctions on Russian majors Rosneft and Lukoil, which are due to be imposed on Friday, have increased concerns over diesel supplies driving prices higher. ICE gasoil prices rose 6.4% yesterday. The restrictions already appear to be having an effect with some Asian purchases out on hold and ICE reporting that physical diesel deliveries will have to be from non-Russian crude.

- Bloomberg reported that there was a US crude inventory build of 4.4mn barrels last week after an increase the week before, according to those familiar with the API data. Product stocks were higher too with gasoline +1.5mn and distillate +600k. The official EIA data is out on Wednesday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: Q3 CPI Consistent With RBNZ Thinking

Q3 CPI printed very close to consensus and the RBNZ’s August projections with a couple of quarterly increases a bit higher. Thus, this outcomes is unlikely to derail any further easing in November. Headline rose 1.0% q/q to 3% y/y after 0.5% & 2.7% in Q2, the top of the target band, with tradeables up 0.8% q/q and domestically-driven non-tradeables +1.1%. See Statistics NZ release here. More details to follow.

AUSSIE 3-YEAR TECHS: (Z5) Strong Weekly Close

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.620 @ 16:28 BST Oct 17

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Aussie 3-yr futures surged on the resumption of trade after the weekend, returning focus higher despite the break of support last week. Short-term resistance at 96.615, the Sep 12 high, has been broken, with 96.780 is the next upside target. Clearance of this level puts markets at fresh multi-month highs. 96.280 marks next major support - but markets are some way off this mark now.

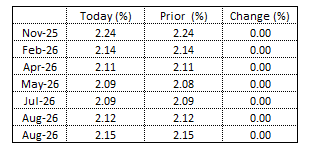

STIR: RBNZ-Dated OIS Pricing Little Changed Ahead Of Q3 CPI

Figure 1: RBNZ-Dated OIS: Today vs. Prior

Source: Bloomberg Finance LP / MNI