OIL PRODUCTS: Oil Products End of Day Summary: Cracks Fall

Nov-06 19:25

Diesel and gasoline crack spreads have fallen today in reaction to an inventory build and a drop in implied demand in the week.

- US gasoline crack down 0.1$/bbl at 13.69$/bbl

- US ULSD crack down 1$/bbl at 23.59$/bbl

- Meanwhile, diesel spreads have eased back after reaching the highest since early August yesterday.

- Gasoline stocks rose despite a drop in imports to the lowest since April 2020 with stocks supported by the strong refinery runs. Weekly implied gasoline demand fell to take the four-week average back below the previous five-year average.

- EIA Weekly US Petroleum Summary - w/w change week ending Nov 01: Gasoline stocks +412 vs Exp -328, Implied mogas demand -33, Distillate stocks +2,947 vs Exp +113, Implied dist demand -475. EIA data showed US jet fuel stocks fell by 228k bbl last week, a 0.5% weekly decline.

- Sunoco Sees refined products demand over the next 6-12 months reflecting demand over the past year, company officials said on a Q3 earning call, cited by Bloomberg.

- The outlook for Europe’s gasoline exports improves with new arbitrage opportunities, according to Sparta Commodities.

- Turkeys Izmit refinery is operating normally following a fire at a compressor unit, Turpas said to Bloomberg.

- Total oil product stocks in Fujairah fell 5.4% during the week to Nov. 4 to 16.141m bbl, amid stable to healthy demand depleted light and heavy products, Platts reported.

- India's fuel demand increased by 11.71% m/m and 2.9% year-on-year to 20.04m metric tons in October, according to the oil ministry Petroleum Planning and Analysis Cell data.

- The price of producing SAF in Asia closed higher in October, driven by rising feedstock prices according to Platts.

- MNI COMMODITY WEEKLY: Sanctioned Barrels Face Potential Shake-Up: https://enews.marketnews.com/ct/x/pjJscVTZkuQI6a4zdxkgGQ~k1zZ8KXr-kA8x6mTC5OsptIPjO1OcQ

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: BLOCKs: Late SOFR Call Calendar Spreads

Oct-07 19:13

- 30,000 SFRF5/SFRH5 96.50 call spds, 4.75 ref 96.06 at 1500:36ET, total volume over 46,000

- 54,350 SFRF5/SFRH5 97.00 call spds, 2.5 ref 96.06 at 1458:14ET, total volume over 65,000

US STOCKS: Extending Late Session Lows, Dow Underperforming

Oct-07 19:03

- Stocks are extending late session lows at the moment, the Dow underperforming as Utility and Consumer Discretionary sectors continue to weigh. Currently, the DJIA is down 488.05 points (-1.15%) at 41865.32, S&P E-Minis down 59.25 points (-1.02%) at 5741.5, Nasdaq down 209.7 points (-1.2%) at 17929.35.

- There were no obvious headline drivers for the extension, likely program related as futures bounced slightly in late trade, focus on this week's CPI/PPI inflation measure, the September FOMC minutes and the start of the latest earnings cycle with Bank of NY Mellon, Wells Fargo, JP Morgan and Blackrock announcing Friday.

- Utilities and Consumer Discretionary sector shares continue to underperform in late trade, water and independent power providers weighing on the Energy sector early on: Vistra -6.54%, American Water Works -4.22%, NextEra Energy -3.53%. The Discretionary sector weighed by a mix of sporting goods, electronics and food related companies: Deckers Outdoor -5.76%, Garmin -4.53%, Ross Stores -4.12% and Dominos Pizza -4.01%.

- Energy and Information Technology sector shares continued to lead gainers in late trade, oil & gas stocks supporting the Energy sector as crude prices continued to surge (WTI +2.84 at 77.21) as Mideast tensions remain unresolved. Diamondback Energy +2.72%, EOG +1.21%, Valero +0.87%. Leading late session gainers in the IT sector: Super Micro Computers surged 15.55% on strong GPU sales, Nvidia gained 3.84%, while Fair Isaac Corp gained 2.10%.

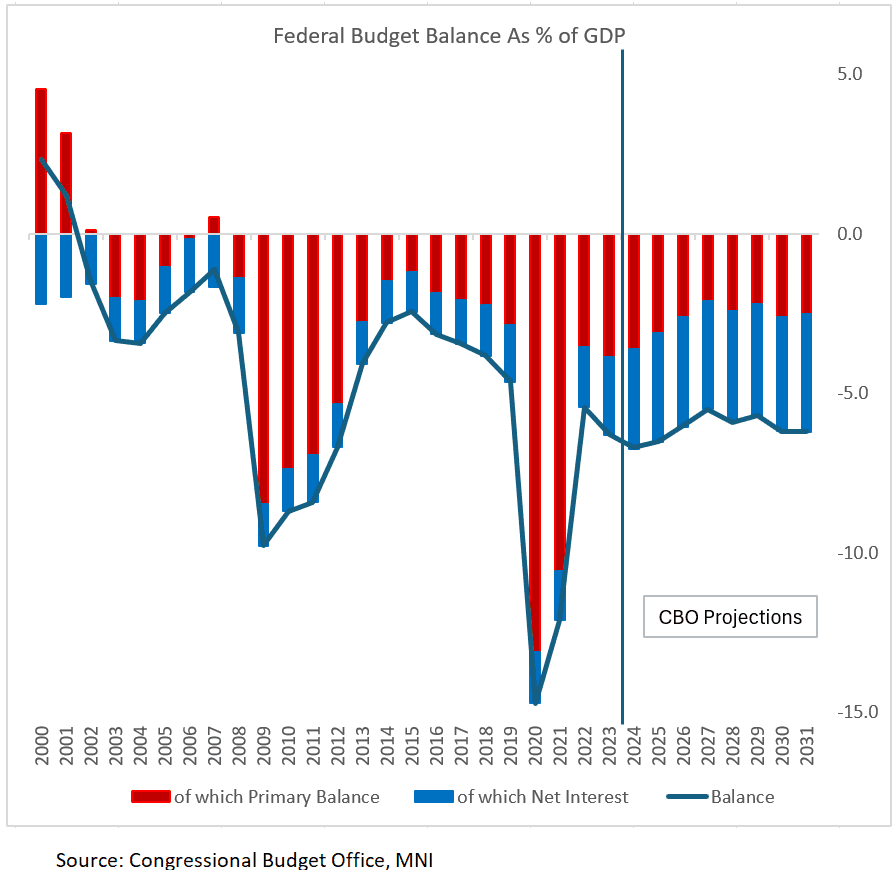

US FISCAL: Debt Pile Rising At $2T/Yr Pace, But Coupon Upsizings To Wait (2/2)

Oct-07 19:03

The bigger picture is that the deficit stopped narrowing vs pandemic wides at around 3.8% of GDP in 2022 on a 12-month rolling basis, rising back to 8.1% in June 2023 before receding again. The CBO estimates a slight improvement in 2025 and beyond, starting with 6.5% of GDP in 2025, but the longer-term outlook remains poor and the overall narrowing will stall in the mid-5% of GDP area.

- Much of that stalling is due to high interest payments, with the primary deficit projected to narrow over the next few years (see chart). The 97% of GDP debt pile (debt held by the public) at end-FY2023 will have grown to around 99% this month, jumping over 100% next year (per consensus and CBO).

- That's after trending down from the 2020 pandemic peak of just under 99%, and 79% in pre-pandemic 2019.

- In nominal terms, the debt pile rose by just under $2T in FY2024 and is set to rise by another $2T in FY2025.

- Attention will soon turn toward Treasury's guidance for future issuance, with coupon sizes expected by many to increase next year amid continued deficits.

- The Oct 30 quarterly Refunding announcement is likely to prove too early for any changes in guidance (at August's refunding, Treasury guided that it was not expecting to increase sizes for "at least the next several quarters").

- There are political sensitivities at play here as well - the fiscal trajectory could change under the next administration (though no major deficit reduction measures are expected from either presidential candidate), and there may well be a new Treasury Secretary in place for the February Refunding round. Additionally there is the end of the debt limit suspension on Jan 1 which throws up some uncertainties for cash management / bill issuance.

- On the latter, it's widely expected that bill issuance adjustments will sufficient to meet near-term deficits (particularly as TBAC has revised its guidance for bills to average 20% of outstanding debt, vs a lower-implied 15-20% before), with coupon auction sizes unchanged until well into 2025.

- Those signs point to any coupon size adjustment announcement to wait until mid-2025 at least - current consensus is for the August 2025 refunding round.