GILTS: Off Lows, Supply Passes Smoothly, Bears Fail To Force Clean Support Break

Gilt futures off lows, with smooth digestion of supply and bears failing to force a meaningful break of yesterday’s low in futures.

- Still, yields remain higher across the curve after this morning’s labour market readings.

- We maintain our base case for a BoE cut in August despite this morning’s data and yesterday’s domestic CPI prints, while continuing to lean towards quarterly cuts (August & November) through year-end.

- Gilt futures pierced initial support at yesterday’s low at 91.17, basing at 91.14 before a recovery to 91.35.

- Bears remain in technical control and a fresh extension lower would target Fibonacci support (90.97).

- Yields 1.5-3bp higher on the day, bear flattening. Benchmarks are 2-3bp off session highs.

- BoE-dated OIS continues to price over 80% odds of a cut for the August meeting, with such a move fully discounted come the end of the September MPC. Just under ~50bp of cuts showing through year-end vs. Monday’s dovish extremes of ~58bp. Market remains happy discounting 1x 25bp cut per quarter through year-end, with Bailey’s dovish commentary help limit hawkish adjustments in the wake of this week’s domestic data.

- Early SONIA option flow has been dominated by upside/dovish exposure in SFIZ5 & H6.

- Little of note on the UK calendar for the remainder of the day, which will leave focus on ongoing adjustment to the labour market data and broader macro inputs.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.004 | -21.3 |

Sep-25 | 3.965 | -25.2 |

Nov-25 | 3.805 | -41.2 |

Dec-25 | 3.727 | -49.0 |

Feb-26 | 3.600 | -61.7 |

Mar-26 | 3.568 | -64.9 |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Off Lows After Auction, Curve Holds Steeper

Gilts hold lower given cues from global peers and with crude oil off yesterday’s lows, although solid demand at the latest 5-Year auction has provided some support in recent trade.

- Futures stick within yesterday’s range, trading as low as 92.37 before recovering to ~92.50.

- Bullish technical conditions remain intact in the contract, initial support and resistance located at yesterday’s low (92.23) & the 50.0% retracement of the Jun 13-16 down leg (92.95), respectively.

- Yields 1-3bp higher, curve steeper.

- 2s10s and 5s30s stick within multi-week ranges, stabilising back above 60bp and 120bp, respectively.

- BoE-dated OIS is little changed on the day, showing ~48bp of cuts through year-end, with the next 25bp step almost fully discounted through the end of the September MPC (~24.5bp of easing showing through that horizon).

- SONIA futures flat to -3.0.

- Expect global cues to dominate for the remainder of the day, with ongoing focus on the next stages of the Israel-Iran conflict.

- Locally, CPI data will cross on Wednesday, ahead of the BoE’s Thursday decision.

- We see downside risks to the headline and services CPI reading (our full preview is available here).

- Still, the data shouldn’t have too much impact on the BoE decision, with no change expected by both the sell-side and markets, but a low print could impact the vote split.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.211 | -0.2 |

Aug-25 | 4.023 | -19.0 |

Sep-25 | 3.967 | -24.5 |

Nov-25 | 3.813 | -40.0 |

Dec-25 | 3.736 | -47.7 |

Feb-26 | 3.623 | -59.0 |

Mar-26 | 3.595 | -61.8 |

GERMAN AUCTION RESULTS: Green Bunds

| 2.10% Apr-29 Green Bobl | 2.30% Feb-33 Green Bund | |

| ISIN | DE000BU35025 | DE000BU3Z005 |

| Total sold | E1bln | E500mln |

| Allotted | E989mln | E495mln |

| Previous | E945mln | E908mln |

| Avg yield | 2.02% | 2.37% |

| Previous | 2.26% | 2.40% |

| Bid-to-offer | 3.18x | 3.49x |

| Previous | 2.43x | 2.04x |

| Bid-to-cover | 3.22x | 3.53x |

| Previous | 2.57x | 2.25x |

| Avg Price | 100.28 | 99.53 |

| Low Price | 100.28 | 99.52 |

| Pre-auction mid | 100.246 | 99.478 |

| Prev avg price | 99.37 | 99.27 |

| Prev low price | 99.36 | 99.25 |

| Prev mid-price | 99.329 | 99.234 |

| Previous date | 21-Jan-25 | 21-Jan-25 |

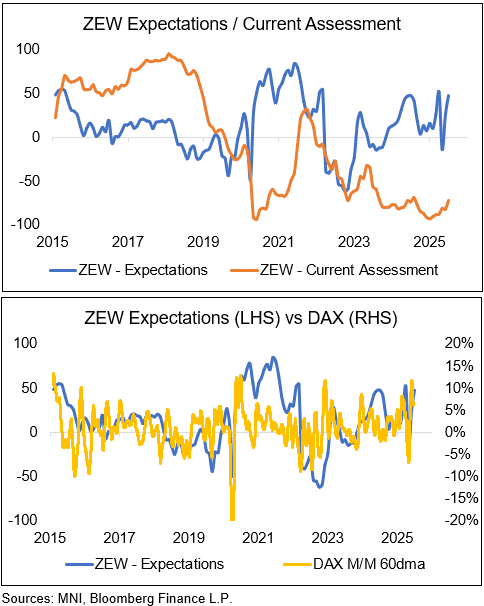

GERMAN DATA: June ZEW Mirrors Brightening German Outlook

The German ZEW expectations index outperformed in June, rising from 25.2 to 47.5 in June, higher than consensus of 35.0 but remaining below March's 3-year high of 51.6. The current conditions index meanwhile was also stronger than expected as it improved from -82.0 to -72.0 (consensus -75.0).

- Wider sentiment has ticked up in Germany recently although remains subdued. Recall that the IFO institute in its latest economic projections believes the economy has moved past its weakest levels: "The crisis in the German economy reached its low point in the winter". That forecast round included a 0.1pp upward revision to GDP growth of 0.3% in 2025 and a more notable +0.7pp to 1.5% in 2026.

- The ZEW survey of 200 analysts was conducted June 6-16.

- The ZEW index is based on a survey of "experts from banks, insurance companies and financial departments of selected corporations [which] have been interviewed about their assessments and forecasts for important international financial market data". It can exhibit elevated levels of correlation with German stock indices such as the DAX, as has been the case particularly strongly in recent months.