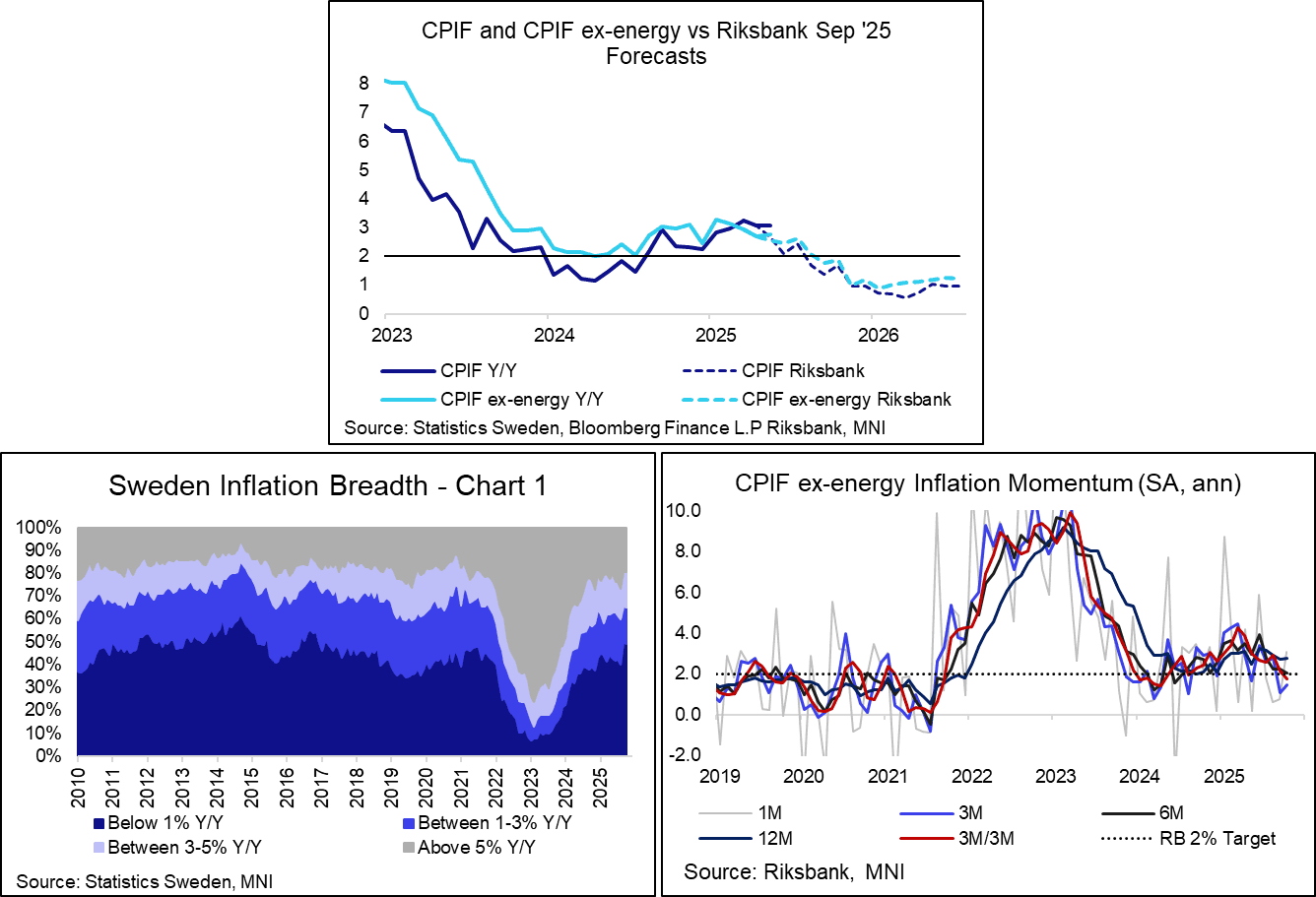

SWEDEN: October CPIF ex-energy Confirmed; Food and Services Pressures Noted

Swedish final October CPIF ex-energy confirmed flash estimates of 2.76% Y/Y. This was two tenths above the Riksbank’s September MPR projection. The Riksbank expects to hold the policy rate at 1.75% for “some time to come”, and one month of inflation data won’t be enough to shift them away from this path. Following last week’s flash release, Riksbank’s Thedeen and Jansson played down the strength of the print somewhat (albeit without knowledge of underlying details).

- On a seasonally adjusted basis using the X-13 methodology, we estimate CPIF ex-energy prices rose 0.25% M/M in October. While a sequential step up from July – September rates, it still allowed 3m/3m inflation momentum to ease to 1.77% (vs 2.15% prior), an 18-month low.

- Food inflation was an important driver of the October uptick, printing at 3.25% Y/Y (vs 2.90% prior). However, food inflation remains well below the 4.00% average seen between January and August this year.

- Services CPIF fell a touch to 3.84% Y/Y (vs 3.93% prior). On a seasonally adjusted basis, we estimate a 0.27% M/M increase, below last month’s 0.54%.

- Disinflation in recreation and cultural services, telephone services, medical services, car rentals and (to a lesser extent) rents contributed here. However, there were elements of strength elsewhere, both in volatile components (package holidays, airfares) and more “underlying” components (restaurants/hotels, insurance, personal care).

- Goods inflation was -0.04% Y/Y (vs -0.19% prior), and we estimate a 0.18% M/M SA clip. Clothing and furniture inflation eased in October, but other household appliance components became less deflationary.

- The proportion of CPI sub-components with annual inflation rates between 1-3% ticked up to 16% (vs 15% prior).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Macro Takeaways from Bank Earnings So Far:

Markets Businesses:

- Wells Fargo: Markets revs up 6% Y/Y driven by higher revenue in equities, commodities, FX and Credit, offsetting weaker rates revenues

- BlackRock: Top growth sectors included iShares ETF business, which saw record demand.

- JPMorgan: Markets revenue up 25% Y/Y, with fixed income up 21%, equities up 33%

- Goldman Sachs: FICC sales & trading higher-than-expected, equities trading revenues lower than expected. Significantly revs in interest rate products and higher revs in mortgages and commodities, partially offset by significantly lower revs in FX and lower revs in credit. Equities reflected significantly lower revs in cash products.

Mortgages & Lending:

- Wells Fargo: Average loans higher by 2% Y/Y, with higher commercial loans, credit cards and auto loans offsetting declines for commercial RE and residential mortgages. Home lending revenues up 3% Y/Y, and up 6% from Q2, personal lending revs down 7% Y/Y

- JPM: Average loans up 7% Y/Y Firmwide

Charge-offs:

- Wells Fargo: Commercial loan charge-offs up $3mln to 18bps of average loans (CRE charge-offs 32bps of average loans)

- JPM: Net charge-offs were $2.0 billion, up $44 million. Reserve build driven by loan growth in Card Services and updates to certain macroeconomic variables in Card Services and Home Lending, partially offset by reduced borrower uncertainty.

- Goldman Sachs: Net charge-offs of $304 million for an annualized net charge-off rate of 0.6% (0.1% for wholesale loans, 5.6% for consumer loans)

Macro:

- JPM: Some signs of softening [in the US economy], particularly in jobs growth, but remains resilient. Continues to be heightened degree of uncertainty stemming from geopolitics, tariffs and trade uncertainty, elevated asset prices and the risk of sticky inflation.

FINLAND: Debt Brake To Be Introduced From 2026

"*FINLAND PARTIES AGREE TO INTRODUCE DEBT BRAKE FROM 2026" Bloomberg

NORWAY: Analyst Views On 2026 Budget Proposal

See below for a selection of sell-side views ahead of tomorrow's budget proposal:

SEB: “We expect the government to hold back spending to leave room to meet demands from support parties"....“We expect petroleum revenue spending around 2.7-2.8% of GPFG, implying a still expansionary budget although a smaller impulse than the 1.3ppt in 2025”...“We expect broadly stable gross NST issuance next year (NOK 95-105bn in 2025). Considering large drawdowns in recent years there is still a need to continue the built up of the cash reserve”

DNB: “We anticipate a broadly neutral fiscal stance, with a structural non-oil budget deficit of NOK 573bn, corresponding to a 2.8% withdrawal rate in 2026 (vs. 2.7%)”.

JP Morgan: “Our economists expect Norwegian fiscal policy to remain expansionary in 2026 with plentiful room for fiscal thrust of 0.6% for next year"....“Our economists expect the structural non-oil budget deficit to be 2.8% of the oil fund’s value, i.e. complying with the 3% fiscal rule. Based on the current market value of the fund (which varies a lot on a daily basis), this translates, in nominal terms, to a structural non-oil deficit of ~NOK 570bn, up NOK 28bn from 2025”.

Nomura: "The government is likely to propose NOK billions for defence funding, and a reduction in electricity tax, which should contribute to lower energy inflation in 2026"..."Fiscal policy is likely to have an expansionary effect on GDP in 2026".

Danske Bank: “Currently we estimate a funding need of NOK87bn”....“Given that in previous years (2023 and 2024), the government has used the account to lower the issuance and thus drawn on the account, it could increase the account in 2026, as it has done in 2025, when we estimate it will be increased by some NOK3bn to NOK13bn. Hence, we end up with an issuance target of NOK90bn-100bn”