BONDS: NZGBS: Yields 3-5bps Lower, Back End Leads

New Zealand government bond yields have lost traction as the Thursday session unfolded. Benchmark yields sit close to 3-5bps lower across the curve, with back end yields seeing slightly largely losses. The 2yr NZGB yield was last at 2.95%, consolidating the recent break sub 3.00%, while the 10yr is back to 4.32%. We are tracking towards fresh lows since April of this year for this benchmark.

- NZGB yields have likely seen some negative spill over from the lower Aussie yield backdrop, although ACGBs are only down a little over 2bps so far today.

- NZ 2yr swap rates continue to make fresh lows, last at 2.72%, off 3bps today.

- Earlier we had a few data points. NZ filled jobs rose for the second straight month in July, which is a tentative sign of some stabilisation in the labour market but the increases remain slight.The ANZ business confidence for August rose to 49.7 from 47.8, the highest since March. However, the activity outlook deteriorated to 38.7 from 40.6, the weakest since May. ANZ noted that the August 20 rate cut drove some “isolated lifts in the data” but there was “no generalised confidence improvement”. The survey remains consistent with a gradual but lacklustre recovery.

- Tomorrow the ANZ consumer confidence index for August is out.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Sentiment Mostly Weaker Ahead Of Key Event Risks

Most regional Asia Pac markets are down in the first part of Tuesday trade. Losses aren't large, but outside of South Korea and Malaysia, trends are negative throughout the region. This follows and overnight session where US markets modestly outperformed EU weakness. So far today, US equity futures are modestly higher, with Nasdaq futures slightly outperforming. This comes ahead of month end late this week.

- Earlier remarks from US Commerce Secretary Lutnick stated that Trump is considering a few deals before the Aug 1 deadline, he will then decide on the unilateral tariff rate. Lutnick stated that an extension of trade truce was likely in terms of the current meetings under with China officials. Trump also pushed back on the idea he was pursuing a summit with China President Xi.

- The China CSI 300 is off a touch, but still close to recent highs. The HSI is down around 1%, but still above the 25300 level. Japan markets are also weaker, the Topix off close to 0.85%. Proximity to earnings outcomes and the Fed decision/data is being cited as a headwind for these markets.

- Taiwan's Taiex is down around 0.85% as well, after a strong run higher in recent weeks. The Kospi is bucking these trends, up nearly 0.60% and firmly above the 3200 level. Earlier we had headlines of corporate tax increases and changes to the capital gains tax, but these shifts have been flagged in the local media prior to today, which may be limiting the market impact.

- In South East Asia, most markets are down, except for Malaysia. Losses are modest though at this stage. Thailand markets have returned, unable to build on recent positive momentum. Thailand has accused Cambodia of violating the recent ceasefire agreement, while a meeting between the countries respective militaries has been postponed.

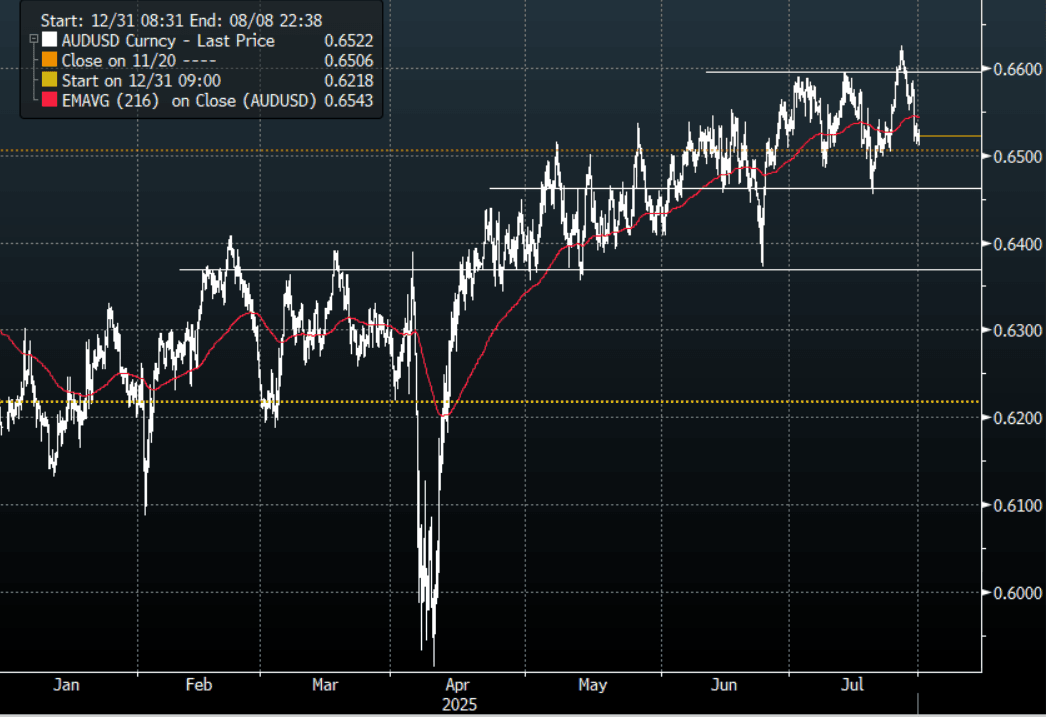

AUD: Asia Wrap - AUD/USD Trades Heavy, Looking Towards Q2 CPI Tomorrow

The AUD/USD has had a range of 0.6512 - 0.6530 in the Asia- Pac session, it is currently trading around 0.6520, -0.02%. The pair could not hold onto its early gains yesterday and slid lower as the USD bounced strongly across the board. The pair failed to gain any momentum above 0.6600 last week and now awaits a very busy calendar this week which could have meaningful implications for risk. Locally the Australian Q2 CPI tomorrow will be closely watched and could provide a catalyst for some movement. Worth keeping in mind it is corporate month-end today and this could see some further headwinds for USD shorts. First support around 0.6450 then the more important 0.6350 area.

- AUSTRALIA: Q2 Core Inflation Expected To Be 0.1pp Above RBA Forecast At 2.7%. Q2 CPI prints Wednesday and will be monitored closely given that the RBA relies on this series with the monthly version not yet complete (due to take place on November 26). Headline inflation continues to be distorted by federal & state government electricity rebates and so attention will remain on the underlying trimmed mean. The RBA’s May forecast was for 2.6% y/y and so a print close to this would likely result in an August cut but steady around Q1 may add doubt.

- CBA Warns Higher CPI Print Could Keep RBA Cautious. A 2.8% print could “be a somewhat awkward 0.2ppt above” the RBA’s latest forecast, but CBA would still expect a 25bp cut on August 12 but see the “decision as not as clear cut as current market pricing suggests”.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD968m), 0.6400(AUD323m). Upcoming Close Strikes : 0.6550(AUD1.01b July30), 0.6600(AUD1.38b July 31), 0.6465(AUD1.01b July31) - BBG

- CFTC Data shows Asset managers added a decent clip to their shorts -53959(Last -38267), the Leveraged community reduced their own shorts to -12010(Last -20048).

- AUD/JPY - Asia-Pac range 96.68 - 96.95, Asia is trading around 96.80. The pair could not hold above 97.00 yesterday. The support between 95.00 - 96.00 held very well last week and the pair is looking to regain its momentum for a move higher. The event-risk coming up this week could provide some short-term headwinds.

Fig 1: AUD/USD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Asia Wrap - Yields Drift Lower In A Quiet Session

The TYU5 range has been 110-25+ to 110-28+ during the Asia-Pacific session. It last changed hands at 110-27+, up 0-03 from the previous close.

- The US 2-year yield has shifted lower trading around 3.914%, down 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.402%, down 0.01 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, decent supply was seen around 4.30/35% first up. A decent bounce was seen off this support but the move has failed to follow through above 4.40% for now. The Data this week should hopefully provide more clarity going forward.

- Nick Timiraos on X: ”Fed officials expect they will need to resume lowering interest rates eventually—they just aren’t ready to do it this week. The questions dividing them center on what evidence they need to see first, and whether waiting for that clarity turns out to be a mistake.”

- “The Fed was united when officials paused cuts this year after tariffs raised fears of renewed inflation. But with tariff-related price hikes proving milder than feared and signs that hiring may be softening, officials are now fractured into three camps over whether to resume cuts.”

- “The focus will be whether Powell offers any hint of a September rate cut in his press conference Wednesday afternoon, and whether in the coming days and weeks his colleagues begin laying the groundwork for a cut at their next gathering.”

- Data/Events: Advanced Goods Trade Balance, FHFA House Price Index, S&P Corelogic, JOLTS, Conf. Board Consumer Confidence, Dallas Fed Services Activity.