BONDS: NZGBs Trade Cheaper, Curve Steepens Tracking US tsys

NZGBs have closed cheaper today with curves steepening after concern over US debt supply and sticky inflation propelled a similar move in Treasuries. Earlier, Trade Balance data showed the deficit had narrowed, while the consumer confidence index rose 0.40% in December, after a 9.4% jump in November.

- New Zealand's total credit card spending dropped 0.8% m/m to NZ$4.67b in November, reversing October's 1% rise, according to RBNZ data. Domestic billings on New Zealand-issued cards fell 1.3% to NZ$3.97b. On an annual basis, credit card spending declined 3.2%, following a 0.3% increase in October. Separately, total advances outstanding decreased 0.8% m/m and 1.9% y/y to NZ$6.23b in November.

- New Zealand's trade deficit narrowed to NZ$437m in November from NZ$1.66b in October, driven by a 9.1% rise in exports to NZ$6.5b, led by dairy products and crude oil. Imports fell 3.9% to NZ$6.9b, primarily due to a 32% drop in petroleum imports. Annually, the trade deficit shrank to NZ$8.2b, down from NZ$13.5b a year earlier.

- US tsys have done very little during the Asian session today, with yields trading flat to 1.1bps lower, as the curve bull-steepens. The US 10yr remains above 4.50% at 4.558% after hitting 4.59% overnight.

- NZGBs curve has bear-steepened again today, the 2yr still hovers near yearly lows at 3.679%, +0.7bps for the session, while the 10yr is +6.7bps at 4.526% at session highs. The 5s10s is +0.50bps at 56.70 and now trades at its steepest levels for the year and almost 40bps steepening since August.

- RBNZ dated OIS is pricing in 54.2bps of cut for the Feb meeting, and 101bps of cumulative cuts are now priced in by May. There is a cumulative 123bps of cuts priced in through to October 2025.

- There is no further data out for New Zealand this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

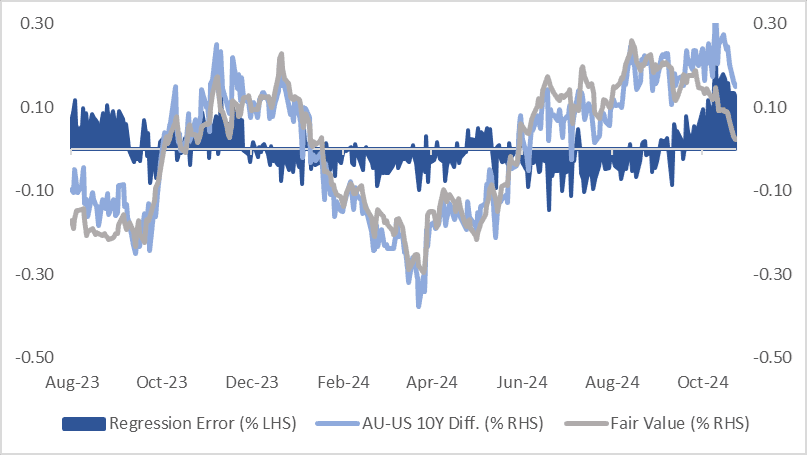

AUSSIE BONDS: AU-US 1Y3M Spread Drives 10Y Diff. Tighter

The AU-US 10-year cash yield differential is at +15bps today, roughly 15bps narrower than levels observed in the lead-up to the US presidential election. Prior to the election, the differential was near the upper end of the +/-30bps range that has largely prevailed since November 2022.

- A simple regression of the AU-US 10-year yield differential against the AU-US 1Y3M swap differential over the past year suggests that the current 10-year yield differential is close to fair value, estimated at +13bps.

- The 1Y3M differential serves as a proxy for the anticipated relative policy trajectory over the next 12 months.

- Since mid-September, the AU-US 1Y3M differential has narrowed by approximately 50bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI – Market News / Bloomberg

GOLD: Geopolitical Tensions Extend The Rebound

Gold is 0.3% higher in today’s Asia-Pac session, after closing 0.8% higher at $2632.08 on Tuesday, amid the escalation in geopolitical tensions between Russia and the West.

- Heightened geopolitical tensions lent support to haven trades after Ukraine launched US made long range missiles into Russia. Despite President Putin's move to revise Russia's nuclear doctrine, however, US State Department Spokesperson Matthew Miller told reporters that the US has seen no reason to adjust its own nuclear posture.

- Short end rates then pushed higher in the second half of the NY session, as projected rate cut pricing into early 2025 was tempered. Lower rates are typically positive for gold, which doesn’t pay interest.

- KC Fed Schmid said "now is the time to dial back restrictiveness of policy". Schmid repeated "While now is the time to begin dialing back the restrictiveness of monetary policy, it remains to be seen how much further interest rates will decline or where they might eventually settle."

- According to MNI’s technicals team, the technicals for gold remain bullish, with eyes on the 20-day EMA at $2,651.1. A clear break above this average would highlight a possible reversal and signal the end of the recent bearish corrective cycle. This would open $2,710.4, the Nov 11 high.

CHINA: US Treasury Holdings Continue to Decline.

- China reduced its holdings of US Treasuries for a third straight month in September data shows.

- China’s US Treasury holdings fell by USD2.6bn to USD772bn.

- Only April and May this year saw marginal increases in China’s US Treasury Holdings with each of the other months in 2024 seeing a decrease.

- Japan, the world’s largest holders of US Treasuries also reduced their holdings in September.