BONDS: NZGBS: Subdued Trading, Underperforms $-Bloc Markets

Feb-10 03:44

NZGBs closed slightly richer across benchmarks after a subdued data-light session.

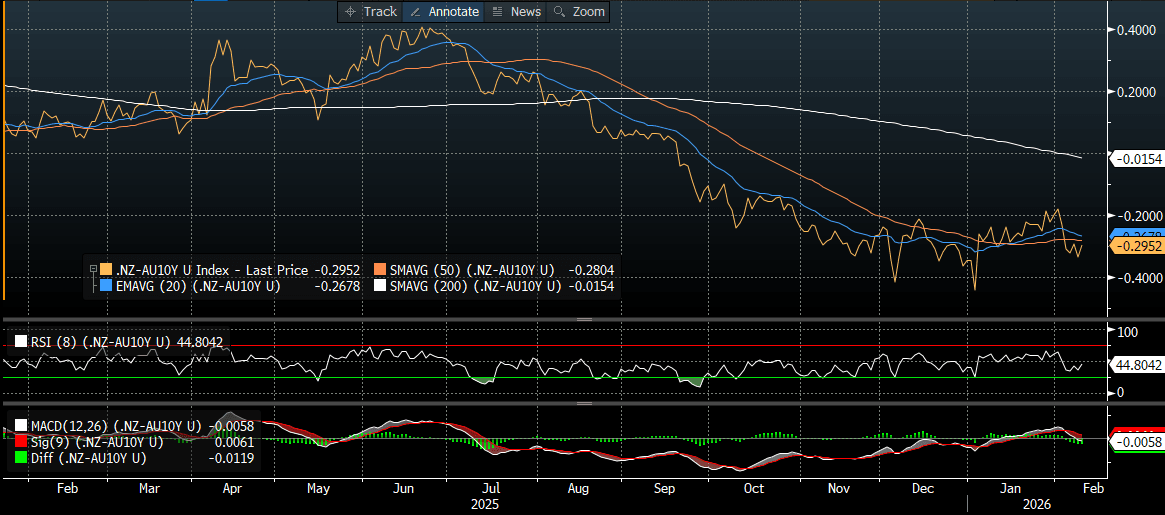

- NZGBs did, however, underperform their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 3-4bps wider.

- Cash US tsys are 1-2bps richer, with a flattening bias, in today's Asia-Pac session.

- (MT Newswires) NZ’s total new lending increased to NZ$20.1 billion in December 2025 from NZ$12.79 billion in November 2025, according to RBNZ data.

- Swap rates closed little changed.

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 44bps.

- Tomorrow, the local calendar will be empty. The local calendar will be light until Friday's release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.5% May-35 bond.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

Jan-10 22:45

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Jan-09 23:36

Test Test TEST

MNI: MNI Test, Please Ignore

Jan-09 23:30

Test, ignore